Quick Answer

Tornadoes and hurricanes are both wind perils under standard homeowners insurance, but they pay out differently because of the deductible. A clear-day tornado usually triggers a flat $500 to $2,500 wind/hail deductible; the same tornado spawned by a named hurricane often triggers a percentage-based hurricane deductible of 1–10% of your dwelling coverage — potentially tens of thousands of dollars.

Key takeaways

- Both tornadoes and hurricanes are wind perils under standard homeowners insurance — but the deductible that applies decides whether your out-of-pocket is $1,000 or $20,000-plus.

- Hurricane (named-storm) deductibles are 1–10% of Coverage A dwelling. On a $400,000 home, that's $4,000–$40,000 in deductible. Standard wind and hail deductibles are flat dollar amounts of $500–$2,500.

- When a hurricane spawns a tornado, most policies trigger the hurricane deductible even though the damage looks like classic tornado damage. The trigger is the named-storm event window, not the damage signature.

- Helene in September 2024 spawned dozens of tornadoes well inland in NC and SC; Florence in 2018 spawned 30-plus confirmed tornadoes in NC alone. Hurricane-spawned tornadoes are now the regional baseline for Carolina homeowners, not an edge case.

- Florida gives 1 year to file (Fla. Stat. § 627.70132), NC and SC both expect mitigation plus documentation, and SC requires insurers to furnish proof-of-loss forms within 20 days — three rulebooks, one documentation discipline that satisfies all of them.

Tornado damage and hurricane damage are both wind perils under standard homeowners insurance, but they pay out very differently because of one mechanism — the deductible. A tornado that hits on a clear blue-sky day in Charlotte typically triggers a flat $500 to $2,500 wind/hail deductible. The same tornado, spawned by a named hurricane two states away, can trigger a percentage-based hurricane deductible of 1–10% of your dwelling coverage — $4,000 to $40,000 on a $400,000 home. The damage looks identical from the curb. The check from your insurer is not. This guide breaks down the physical differences, the insurance mechanics, and the documentation strategy that protects your claim across Florida, North Carolina, and South Carolina. For the broader pillar see storm and hurricane damage restoration, and if your home was just hit by a tornado, tornado-damage restoration is the same-day service page.

EF1 tornado peak winds

86–110 mph

NOAA Storm Prediction Center / National Weather Service Enhanced Fujita scale — the most common tornado strength in FL, NC, and SC

Cat 3 hurricane sustained winds

111–129 mph

NOAA Saffir-Simpson scale, sustained over a 1-minute average — but tropical winds cover hundreds of square miles, not a 200-yard track

Hurricane deductible range

1%–10%

Insurance Information Institute (III): percentage of Coverage A dwelling, varies by state, carrier, and proximity to coast

Tropical-system tornadoes per year

~10–60

NOAA SPC long-term average for the U.S.; Hurricane Helene in 2024 alone spawned dozens across the Carolinas

Tornado vs Hurricane: How the Damage Itself Differs

Physically, tornadoes and hurricanes deliver wind energy in fundamentally different ways. A tornado is a concentrated rotating column with peak winds inside a path that, per NOAA Storm Prediction Center climatology, is most often 50 yards to a quarter-mile wide and travels a few miles before lifting. The forces are rotational — twisting, uplift, and lateral displacement — and they leave a surgical signature: one home reduced to splintered framing while the immediately adjacent home stands largely intact. A hurricane is a continental-scale system with sustained directional winds, a much wider footprint (often 100+ miles in diameter), and a saltwater storm surge component along the coast. Hurricane damage is distributed: thousands of homes with peeled shingles, lifted ridge caps, downed fences, and saturated wall cavities, with relatively few showing total structural failure outside the surge zone.

Tornado damage characteristics

- Path is narrow — most often 50 yards to a quarter-mile wide, occasionally up to 2.6 miles for the largest events

- Duration on any single property is seconds to a minute

- Forces are rotational: twisting, uplift, and lateral displacement of structures

- Debris field fans out in concentric arcs; one home destroyed, the next largely intact

- Water role is limited to wind-driven rain through the breach — no storm surge

- Restoration is concentrated on a small number of severely damaged homes

Hurricane damage characteristics

- Footprint is wide — sustained tropical-storm-force winds can extend 100+ miles from the eye

- Duration on any single property is hours, sometimes longer than a full day

- Forces are directional and sustained: shearing, fatigue loading, and pressure-cycling

- Damage pattern is distributed — thousands of homes with similar moderate damage

- Water role is significant: storm surge, wind-driven rain, plus inland flooding

- Restoration capacity is regionally strained, queues stretch weeks to months

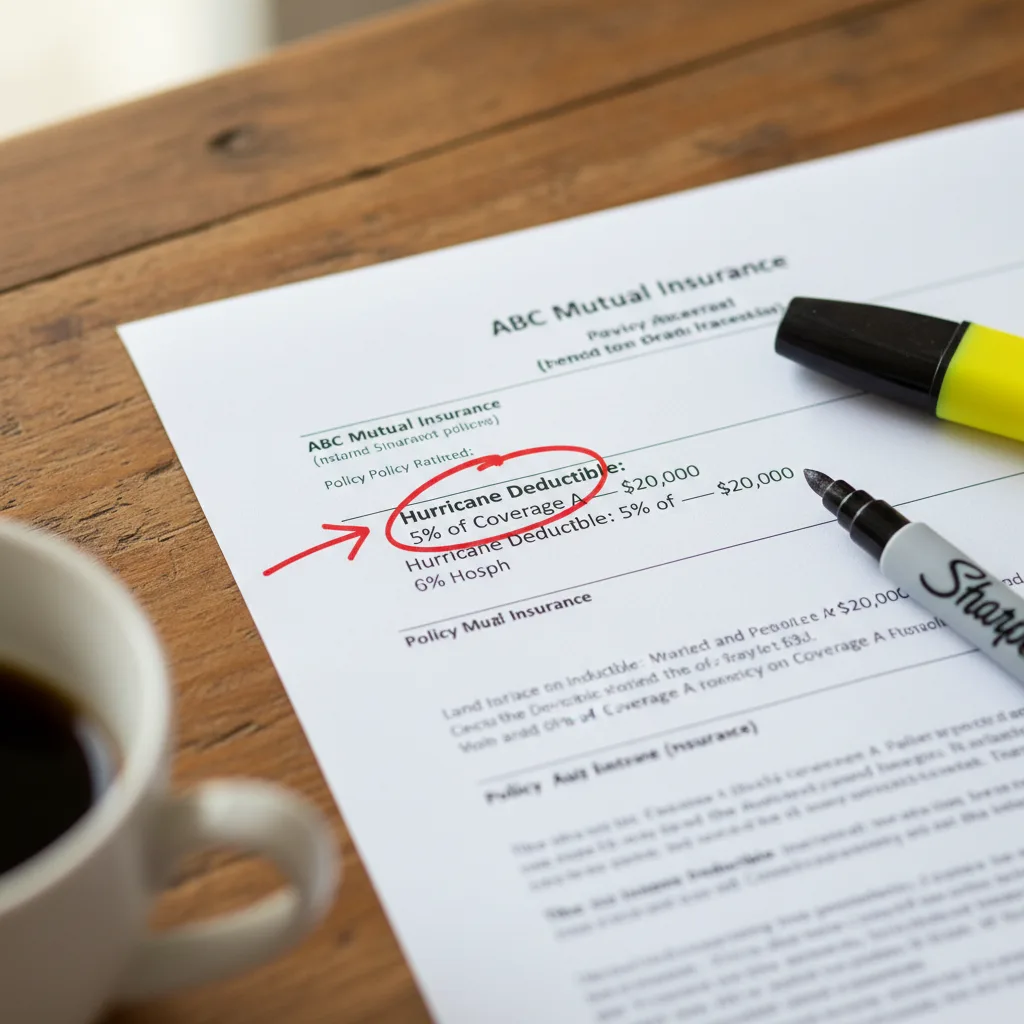

The Insurance Difference That Costs Homeowners Thousands: Hurricane Deductibles

Standard homeowners insurance treats wind and hail as a covered peril. On a clear-day tornado, you typically pay your standard deductible — a flat dollar amount of $500 to $2,500 — and the carrier covers the rest of a covered loss up to your coverage limits. On a hurricane, almost every coastal-state policy applies a separate, percentage-based deductible called a hurricane deductible or, more broadly, a named-storm deductible. The Insurance Information Institute (III) puts the typical range at 1% to 10% of Coverage A — your dwelling limit. On a $400,000 home, that's between $4,000 and $40,000 of out-of-pocket exposure on a single event. Florida codifies the rules in Fla. Stat. § 627.701, which sets allowable hurricane-deductible options at 2%, 5%, and 10% (with limited exceptions), and requires explicit homeowner sign-off for the higher tiers.

| Scenario | Deductible type that applies | Typical out-of-pocket on a $400k home | Why |

|---|---|---|---|

| Tornado on a clear day in Charlotte, NC | Standard wind/hail (flat dollar) | $500 – $2,500 | No named storm in the region; carrier applies the standard policy deductible |

| Tornado spawned by a named hurricane in NC inland counties | Hurricane / named-storm (percentage) | $4,000 – $40,000 | Damage occurs inside the carrier's named-storm trigger window |

| Direct hurricane wind damage on a Deerfield Beach, FL coastal home | Hurricane / named-storm (percentage) | $20,000 – $40,000 (5–10% common in FL) | FL hurricane deductible applies once a watch or warning is issued for the county |

| Wind-only damage from an unnamed tropical depression | Standard wind/hail (flat dollar) | $500 – $2,500 | Hurricane deductible only triggers for systems named by the National Hurricane Center |

Tornado vs hurricane deductible scenarios — same home, four different out-of-pocket outcomes

Tornado Damage Insurance: What Standard Homeowners Actually Covers

On a tornado outside any named-storm window, your standard homeowners policy treats the event as a wind/hail loss. Coverage A pays for structural damage to the dwelling — the roof, exterior walls, framing, decking, and any built-in fixtures. Coverage B picks up detached structures like fences and sheds. Coverage C reimburses damaged personal property at either replacement cost or actual cash value, depending on how the policy is written. Coverage D — additional living expenses (ALE) — covers hotels, restaurant meals above your normal grocery budget, and pet boarding while the home is unlivable. What standard homeowners does *not* cover is ground-up flooding from rising water, which is the same trap as hurricane coverage: an uncovered peril needs a separate NFIP or private flood policy. For the deeper split see our wind damage vs flood damage breakdown.

There's a counter-intuitive insight worth its own paragraph: when the same physical damage is treated as a tornado loss rather than a hurricane loss, your *net* payout is often higher even though gross damages are identical. The reason is the deductible delta. On a $80,000 covered loss, a flat $1,000 wind/hail deductible leaves you with $79,000. The same $80,000 loss with a 5% hurricane deductible on a $400,000 home leaves you with $60,000. That's a $19,000 swing on identical paperwork, identical contractors, identical scope of work. This is why the deductible question — which one applies — is the most consequential single conversation in any post-storm claim, and why the documentation step we cover below matters far more than most homeowners realize before their first claim.

When a Hurricane Spawns a Tornado: The NC and SC Reality

Tropical systems generate tornadoes in the right-front quadrant of the storm as the cyclone interacts with land friction and increased wind shear. NOAA Storm Prediction Center records show this is not a fringe event — it's a regular feature of late-season Atlantic landfalls, and the Carolinas absorb the largest share. Hurricane Florence in September 2018 spawned 30-plus confirmed tornadoes in North Carolina alone per NWS Wilmington and NWS Newport storm survey data, several of them well inland. Hurricane Helene in September 2024 produced a dense cluster of tornadoes across the Carolinas inland of the surge zone, hitting Piedmont and Upstate SC counties hundreds of miles from the coast. Hurricane Idalia in 2023 spawned tornadoes across northern Florida and southeast Georgia. The pattern matters because it makes the inland Carolina homeowner — far from any beach — a primary target for the hurricane-deductible-on-tornado-damage scenario.

How carriers decide which deductible applies

When damage occurs during a named-storm window, the default carrier position is that the hurricane deductible applies to all damage from the event, including any tornado damage. To shift away from that default — or to keep the carrier from misclassifying — homeowners need cause-of-loss documentation that ties the damage to a specific peril and timeline. The two artifacts that carry the most weight are NOAA / NWS storm survey reports (which assign EF ratings, document tornado tracks, and establish the time and date a funnel touched down) and a documented timeline of when damage at your address occurred relative to the named-storm window. State insurance departments — including the North Carolina Department of Insurance and the South Carolina Department of Insurance — provide consumer assistance for disputed multi-peril claims, and the insurance claim process is one of the situations where a public adjuster's involvement most often pays for itself.

Do — multi-peril documentation that protects your claim

- Pull the NWS storm survey report for your zip code and save the EF rating, path, and times

- Photograph damage with timestamps and weather-app screen captures of the storm's named status

- Keep separate scope-of-work files for tornado damage vs. broader hurricane damage on the property

- Note the moment the National Hurricane Center named or downgraded the system

- File a single claim, but flag the multi-peril nature in writing on the first carrier contact

Don't — documentation gaps that get tornado-during-hurricane claims denied or shorted

- Don't rely on the carrier's adjuster to identify the peril split — they default to the higher deductible

- Don't sign a release without confirming which deductible was applied to your settlement

- Don't conflate tornado debris with hurricane debris in your photo set — keep them separated by location

- Don't toss the original NWS storm reports — they're the strongest cause-of-loss evidence available

- Don't accept verbal explanations for deductible decisions; ask for the policy language and trigger date in writing

State-by-State: Florida, North Carolina, South Carolina

Florida

Florida leads the U.S. in raw tornado count when normalized for area, but most Florida tornadoes are EF0–EF1 events with relatively narrow damage tracks. The hurricane deductible in Florida is statutory — Fla. Stat. § 627.701 sets the allowable percentages and consumer disclosure requirements — and once a hurricane watch or warning is issued for any part of the state, the named-storm deductible window typically opens. Florida also has the strictest claim-filing window in the region: Fla. Stat. § 627.70132 caps the time to give notice of a property insurance claim or reopened claim at 1 year from the date of loss, with supplemental claims barred after 18 months. For coastal Florida homeowners insured through Citizens Property Insurance Corporation, separate hurricane deductibles apply per occurrence per calendar year. For the deeper FL framework see our Florida 1-year claim deadline breakdown and Florida Citizens insurance claim guidance.

North Carolina

North Carolina sits at the eastern edge of what NOAA informally calls Dixie Alley — a tornado-prone zone running across the Deep South that peaks in spring (April–May) but reactivates during late-season Atlantic hurricane landfalls (August–October). The North Carolina Insurance Underwriting Association — also known as the Beach Plan or NCIUA — writes residential windstorm and hail policies for the state's beach-area zones; outside that windstorm coverage, standard homeowners covers wind/hail statewide. NC consumer guidance from the NC Department of Insurance asks homeowners to do three things in order after a loss: report the loss to the carrier, document damage with photos before any cleanup, and stop further damage with mitigation like roof tarping while keeping every receipt. NC also publishes specific consumer warnings about storm chaser scams, which spike after every multi-county event.

South Carolina

South Carolina inland zones — the Pee Dee, Midlands, and Upstate — see traditional spring tornado activity, while the coastal corridor absorbs both direct hurricane impacts and hurricane-spawned tornadoes that sometimes reach 100+ miles inland. The SC Wind and Hail Underwriting Association writes windstorm coverage for coastal counties; standard homeowners covers wind/hail elsewhere. SC procedural detail homeowners should track during a claim: state law requires insurers to furnish proof-of-loss forms within 20 days after notice of loss, and if those forms are not furnished within that timeframe, the claimant is treated as having complied with proof-of-loss requirements. That's a real protection — the calendar starts the day notice is given, not the day the carrier responds. For the broader SC framework see our South Carolina hurricane preparation checklist.

Restoration Timeline: Tornado vs Hurricane

T+0 to 24 hours

Safety and emergency mitigation

Tornado: utility lockout, debris triage, emergency tarping over roof breaches, board-up of broken windows. Hurricane: same scope but with regional capacity strain — emergency dispatch crews work across an entire metro at once. In both cases, the EPA and CDC put the wet-material drying window at 24 to 48 hours before mold growth begins.

Day 1–7

Documentation, claim notice, water mitigation

Photograph everything before cleanup, file claim notice (FL clock starts immediately), water mitigation crews extract standing water and set drying equipment. Tornado: contractors converge from outside the affected area within 48 hours. Hurricane: queues stretch as adjusters and contractors rotate across counties.

Week 1–4

Adjuster scope and structural assessment

Carrier adjuster inspects, scope-of-work is finalized. Engineers assess load-bearing damage on tornado losses — uplift signatures often require structural rebuild, not just envelope repair. Tornado timelines stay tight here. Hurricane timelines slow due to regional adjuster shortages after major declarations.

Month 1–6

Reconstruction phase

Permitting, framing, mechanical/electrical/plumbing rough-ins, drywall, finishes. Tornado: a tight cluster of total losses can rebuild in 3–6 months when materials are available. Hurricane: regional material shortages and labor competition can extend timelines to 9–12 months on similar damage.

Month 6–12+

Final completion and supplementals

Punch list, final inspections, supplemental claims for damage that surfaces after the original adjustment closes. In Florida, supplemental claims must be filed within 18 months of the date of loss per Fla. Stat. § 627.70132. For total-loss tornado situations, see large loss handling.

Documenting Tornado Damage for Your Claim

- 1

Wait for safety clearance, then start outside

Don't enter a tornado-damaged structure without a professional safety walk-down. Gas leaks, downed lines, and compromised load-bearing elements are the leading hazards. Document the exterior first.

- 2

Walk the perimeter with phone video on

Slow continuous video around all four sides establishes the relationship between the storm path and your property. Narrate as you go — date, time, and what you're seeing. Then return for stills.

- 3

Document the debris field as evidence

Tornado debris fans out in concentric arcs and the pattern itself is evidence of rotational forces. Photograph it before any cleanup. Insurance fraud investigators look at this pattern; so do your adjuster and any public adjuster you bring in.

- 4

Pull the NWS Storm Prediction Center event log

Search the SPC database for your zip code and date. The official EF rating, path coordinates, and times are the strongest cause-of-loss evidence in any multi-peril dispute. Save the report as a PDF.

- 5

Build a cause-of-loss narrative if a hurricane was active

If a named storm was in or near your state when the tornado touched down, write a one-page narrative with timestamps: when the system was named, when the funnel formed at your address, when you first observed damage. Attach to your claim file.

- 6

Get a professional damage assessment in writing

An IICRC-certified contractor produces a Xactimate-ready scope of work. The carrier's adjuster will produce theirs. Side-by-side scope comparison is the leverage point for any disputed line item.

- 7

File the claim with the multi-peril nature flagged

On your first contact with the carrier, state in writing that the loss involves potential tornado-versus-hurricane peril classification. That single line in the claim file forces a more careful initial scope — and protects against a default to the higher deductible.

Common Tornado-vs-Hurricane Claim Mistakes

Do — claim moves that hold up at every stage

- Document and mitigate inside the EPA's 24–48 hour wet-material drying window

- File claim notice within the first week regardless of adjuster availability

- Keep every receipt from tarp materials, debris removal, hotel, and pet boarding

- Pull and save the NWS storm survey report for your event

- Get a written contractor scope of work before signing any settlement

- Verify the deductible category your settlement actually applied

Don't — mistakes that cost homeowners thousands

- Don't sign a contract with a contractor who knocked on your door uninvited

- Don't pay any contractor in cash up front for storm work

- Don't accept a settlement that doesn't itemize the deductible category

- Don't toss debris before the carrier's adjuster has documented it

- Don't skip filing because you think it's "only $5,000 of damage" — small claims feed supplementals later

- Don't sign an Assignment of Benefits (AOB) without reading every line — see FL restrictions for post-2023 policies

Storm-chaser contractor fraud spikes after both tornado and hurricane events, and the post-Helene period in 2024 saw NC and SC consumer protection agencies issue specific warnings about door-to-door pitches and Assignment-of-Benefits abuse. The pattern is consistent: a contractor with no local address pressures a stressed homeowner into signing a contract or AOB the same day, then either disappears with a deposit or runs the claim up to maximize their cut. For the deep-dive on the warning signs and how to vet a crew, see storm chaser scams and the documentation discipline in filing a storm damage insurance claim.

When to Call a Public Adjuster

Public adjusters work for the homeowner — not the carrier — and they're licensed by each state's department of insurance. The four scenarios where their fee almost always pays for itself: a total or near-total loss, a denied claim, a settlement that's significantly below the contractor's written scope, and any multi-peril dispute. The tornado-during-hurricane deductible question is a textbook multi-peril dispute, and it's the single most common scenario where homeowners benefit from an adjuster who can argue cause-of-loss with NWS reports and policy language. License lookups by state are at the Florida Office of Insurance Regulation, the North Carolina Department of Insurance, and the South Carolina Department of Insurance.

Choosing a Restoration Contractor After a Tornado or Hurricane

- Verify the contractor's state license through the official licensing board (FL CILB, NC Licensing Board for General Contractors, SC LLR)

- Confirm IICRC certification for water mitigation (S500), mold remediation (S520), or fire restoration (S700) as applicable

- Demand a verifiable local physical address — not a P.O. box, not a magnetic sign on a truck

- Request a current Certificate of Insurance directly from the contractor's insurer

- Get a written, itemized scope of work — never a flat-rate or verbal estimate

- Refuse any request for cash up front; a deposit on materials is normal, payment in full is not

- Pull two or three local references from the same county and call them

- Check the BBB profile, Google reviews, and any state attorney general complaint history

For the broader contractor-selection framework see how to avoid storm chaser scams after a hurricane and the documentation discipline in how to spot storm damage on your roof. When a tree was the cause, the tree fell on my house walkthrough covers the parallel claim path.

Frequently Asked Questions

Does my hurricane deductible apply if a tornado was spawned by a hurricane? +

Tornado vs hurricane damage — which costs me more out-of-pocket? +

What's the difference between a named-storm deductible and a standard wind/hail deductible? +

How long do I have to file a tornado damage claim in Florida, North Carolina, or South Carolina? +

If a hurricane caused both wind damage and a tornado, do I file one claim or two? +

Can my insurer call my tornado damage "just wind damage" to apply the hurricane deductible? +

Do I need a separate tornado insurance policy? +

Why are tornado damage payouts sometimes larger than hurricane damage payouts on similar homes? +

Three regional faces of the same insurance question — Florida coastal hurricane-spawned tornado damage, NC inland Dixie Alley spring tornado damage, and SC Pee Dee tornado aftermath. Same peril, three different policy structures.

Storm, Wind & Hurricane Damage

24/7 emergency response across Florida, North Carolina, and South Carolina — the central pillar for everything storm-related, including hurricane and tornado dispatch.

Tornado Damage Restoration

Same-day tornado-damage restoration service page — emergency tarping, debris removal, structural drying, and full reconstruction across FL, NC, and SC.

Wind Damage vs Flood Damage

The companion blog to this one — covers the wind/flood split that drives most coastal hurricane claims, with FL/NC/SC carrier and NFIP context.

Storm Damage Insurance Claim Guide

End-to-end claim filing playbook — notice timing, documentation discipline, adjuster coordination, and supplemental-claim strategy for FL, NC, and SC.

NOAA Storm Prediction Center

Authoritative source for tornado climatology, EF-scale ratings, storm survey reports, and the cause-of-loss documentation any tornado claim hinges on.

Insurance Information Institute (III)

Industry reference for hurricane-deductible mechanics, named-storm trigger language, and U.S. multi-peril claim averages by region.

NC Department of Insurance

North Carolina consumer assistance for homeowners insurance, storm-chaser scam reporting, and disputed multi-peril claim guidance.

SC Department of Insurance

South Carolina consumer assistance, including the 20-day proof-of-loss requirement and SC Wind & Hail Underwriting Association reference.

The single most consequential conversation after any storm is which deductible category the carrier applies to your claim. On a tornado spawned by a hurricane, that conversation can swing your out-of-pocket by tens of thousands of dollars. Palm Build's IICRC-certified crews handle tornado and hurricane damage 24 hours a day across Florida, North Carolina, and South Carolina, and we coordinate documentation, mitigation, and rebuild as a single chain of custody — including the cause-of-loss narrative your adjuster needs to see. For tornado-specific service, visit tornado-damage restoration. For the broader storm pillar, see storm and hurricane damage restoration.

Tornado or hurricane damage in FL, NC, or SC? Get a same-day expert assessment.

Palm Build's IICRC-certified crews respond 24/7 across Florida, North Carolina, and South Carolina with the documentation framework adjusters approve — and the cause-of-loss narrative that protects your deductible category from the moment we arrive on site.

Found this helpful? Send it to someone who needs it.