Standard (AOP) deductible

$500 – $5,000

Paid out-of-pocket before insurance pays anything. Flat dollar amount on most policies.

Insurance claims feel overwhelming, but they follow a predictable process. This guide walks you through every step — from the first phone call to final settlement — so you get what your policy owes you. Bookmark this page and come back whenever you need it.

Your Claims Advocate

Insurance claims feel overwhelming, but they follow a predictable process. Understanding that process gives you leverage — you know what to expect, what to document, and when to push back.

Palm Build navigates claims daily and helps homeowners get full coverage. This page is your reference guide: bookmark it and return whenever you need clarity on documentation, adjuster coordination, or claim workflow.

Claims Handled Daily

Experienced claims coordination

200+ Photos Per Loss

Avg documentation standards

Xactimate Certified

Industry-standard estimating

FL & NC Licensed

State compliance in service areas

Interactive Claims Map

Click any step to see what you, your contractor, and your insurer do at each stage. Pin your current step to track where you are.

The sticker price of a restoration project is not what you pay. Between deductibles, non-covered scope, and depreciation holdback, the out-of-pocket cost to the homeowner can vary from a few hundred dollars to tens of thousands. For a deeper look at how deductibles stack with depreciation see homeowners insurance deductible explained.

| Scenario | Total claim | Deductible | Net to homeowner |

|---|---|---|---|

Category 1 burst pipe Single bathroom, ~200 sq ft, 4 days of drying, minimal demo. | $6,800 | $1,000 | $5,600 |

Category 3 sewage backup Basement, ~600 sq ft, full content loss, selective demolition, antimicrobial treatment. | $24,500 | $1,000 | $18,900 |

Named-storm wind + roof loss 2,200 sq ft home, 25% roof replacement, interior water damage, Florida coastal. | $48,000 | $8,000 | $34,300 |

Kitchen fire + smoke remediation 1,800 sq ft home, full kitchen replacement, smoke restoration throughout. | $72,000 | $2,500 | $62,700 |

Whole-home Category 2 water loss 3,000 sq ft, multi-room extraction, mold sublimit triggered, full rebuild scope. | $108,000 | $2,500 | $91,300 |

The components of homeowner exposure in a typical claim. Some you can plan for; others are recoverable if you follow through on the final paperwork.

Paid out-of-pocket before insurance pays anything. Flat dollar amount on most policies.

FL coastal policies commonly use 2-10% of Coverage A. A $400k home with a 5% hurricane deductible = $20,000 out-of-pocket.

Recoverable only after you complete repairs and submit the final invoice + proof of completion.

Cosmetic items, code upgrades beyond sublimit, landscaping, outbuildings above Coverage B limit, mold over sublimit.

If Coverage A is lower than the cost to rebuild, the shortfall comes from your pocket. Revisit dwelling limits every 2-3 years.

After this limit is exhausted, hotel/meal/laundromat costs are out-of-pocket even if you are still displaced.

Every policy type covers different perils in different ways. About 80 percent of U.S. homeowners carry HO-3, but HO-5, HO-6, HO-8, DP, and commercial CP 00 10 each have their own rules. Knowing which form you have is the first step in understanding what your claim will actually pay. For the coverage matrix that follows from this, see our homeowners insurance covers guide and water damage coverage guide.

Fire, lightning, windstorm, hail, explosion, riot, aircraft, vehicles, smoke, vandalism. No theft coverage. Rare today — some insurers no longer write it.

Best for

Lowest-cost option for minimal coverage. Rarely sold today.

HO-1 perils plus theft, falling objects, weight of snow/ice, accidental water discharge, freezing of plumbing, sudden tearing/cracking of heating systems, and short-circuit damage.

Best for

Budget-minded homeowners who want broader protection than HO-1 but do not need open-peril structure coverage.

Covers all perils on the dwelling except those specifically excluded (flood, earthquake, wear and tear, maintenance failure, etc.). Personal property is still named-peril — only the 16 HO-2 perils apply.

Best for

The default policy for most U.S. homeowners. About 80 percent of homeowner policies are HO-3.

Same open-peril structure coverage as HO-3, but also extends open-peril coverage to personal property. Fewer disputes over whether content damage fits a "named" peril. Typically higher premium but stronger coverage.

Best for

Higher-value homes and owners with substantial personal property. Claim disputes are less frequent than HO-3.

Covers interior "walls-in" property and personal contents. The building exterior and common areas are covered by the HOA master policy. Assessment coverage (your share of HOA deductible or shortfall) is an important optional endorsement.

Best for

Condo and co-op unit owners. Read the HOA master policy before setting HO-6 limits.

Designed for older homes where replacement cost exceeds market value. Payouts are typically based on actual cash value (ACV) or functional replacement cost rather than full replacement cost.

Best for

Historic or older homes where rebuild cost using modern materials would dwarf the market value.

DP-1 is named peril on structures not occupied by the owner (rentals, seasonal homes, vacant). DP-3 is the open-peril rental equivalent to HO-3. No personal property coverage unless endorsed.

Best for

Landlords, vacation home owners, and property held between owners or under renovation.

The ISO commercial property form for buildings, business personal property, and tenant improvements. Pairs with the Causes of Loss form (Basic / Broad / Special) and typically a Business Income (CP 00 30) endorsement for lost revenue.

Best for

Commercial buildings, multi-tenant properties, warehouses, retail, offices. Business income coverage is critical for any operating business.

| Form | Structure | Contents | Perils covered |

|---|---|---|---|

| HO-1 | Named peril (10) | Named peril (10) | Fire, wind, hail, explosion, riot, vandalism, theft (limited) |

| HO-2 | Named peril (16) | Named peril (16) | HO-1 + theft, falling objects, freezing pipes, snow/ice load |

| HO-3 | Open peril | Named peril (16) | All perils except exclusions (flood, earthquake, wear) |

| HO-5 | Open peril | Open peril | All perils on structure AND contents except exclusions |

| HO-6 | Walls-in only | Named peril | Interior + contents; HOA master policy covers exterior |

| HO-8 | Named peril (limited) | Named peril (limited) | ACV or functional replacement — older homes |

| DP-3 | Open peril | Not included | Landlord / rental open-peril equivalent to HO-3 |

| CP 00 10 | Open peril (Special) | Open peril (Special) | Commercial — pairs with Business Income (CP 00 30) |

Eleven perils across HO-3, HO-5, NFIP flood, and commercial CP 00 10 — with the endorsements, sublimits, and exclusions that catch homeowners off guard. Read our understanding coverage guide for the full deep-dive.

| Trigger / peril | HO-3 | HO-5 | NFIP | CP 00 10 |

|---|---|---|---|---|

Sudden burst pipe (frozen / failure) Must be sudden and accidental. Long-term slow leaks are excluded. | Covered | Covered | Not applicable | Covered (Special) |

Long-term hidden leak (weeks / months) Classified as maintenance failure or gradual damage. Core exclusion across all policies. | Excluded | Excluded | Not applicable | Excluded |

Storm rising water / surge / flood Flood is always NFIP-only (or private flood). Standard homeowner and commercial policies do not cover rising water. | Excluded | Excluded | Covered | Excluded |

Wind damage (hurricane / tornado) Hurricane deductible typically applies. Coastal states may require separate wind/hail policy or NCIUA (NC) / Citizens (FL). | Covered | Covered | Not applicable | Covered |

Hail damage Separate wind/hail deductible may apply in hail-prone regions. | Covered | Covered | Not applicable | Covered |

Sewer backup Excluded by default on homeowner policies. Add a sewer backup endorsement (typically \$50-\$250/year) for up to \$5,000-\$25,000. | Endorsement only | Endorsement only | Sometimes covered | Endorsement only |

Fire and smoke damage Core covered peril. Wildfire coverage is typically included but may have separate deductibles in WUI zones. | Covered | Covered | Not applicable | Covered |

Mold damage Only covered when resulting from a covered water loss. Typical sublimit \$5,000-\$10,000. Mold from neglect or long-term leak is excluded. | Sublimit | Sublimit | Excluded | Sublimit |

Earthquake / earth movement Separate earthquake policy required. Applies to sinkholes in FL (separate coverage required under FL Statute 627.706). | Excluded | Excluded | Excluded | Excluded |

Ordinance / law (code upgrades) Covers the extra cost of rebuilding to current code. Often under-limited — consider an ordinance/law endorsement for older homes. | Usually 10% sublimit | Usually 10% sublimit | Sublimit | Endorsement (CP 04 05) |

Additional Living Expense / Loss of Use Homeowner ALE covers hotel, meals, laundromat during displacement. NFIP does not include ALE. Commercial uses Business Income coverage instead. | Typically 20-30% | Typically 20-30% | Not covered | Business Income (CP 00 30) |

Ten steps from the moment damage is discovered to the final depreciation recovery — with the exact phrases that work with adjusters. For water-specific guidance see how to file a water damage insurance claim. For Florida-specific timing see the 2026 Florida crisis guide.

Shut off water at the main, kill power to affected circuits, and evacuate if the structure is unsafe or air quality is compromised. For fire losses, do not re-enter until the fire department clears the property. Nothing else on this list matters if someone is injured — and insurers will never penalize you for prioritizing safety.

What to say to your adjuster

"The scene was unsafe until [time] on [date]. I have photos showing the hazards that delayed my access."

Take hundreds of photos from multiple angles — wide room shots, close-ups of the damage source, water lines on walls, content damage, the mechanical room, serial numbers on appliances. Narrated video walkthroughs are even stronger than stills. Photograph your mitigation progress as it happens. The documentation phase is the single highest-leverage step in the entire claim — thin documentation is the number-one reason claims are undervalued.

What to say to your adjuster

"I have 200-plus time-stamped photos and a narrated video walkthrough. I can share the full library on request."

The claim number on your insurance card routes you directly to the 24/7 catastrophe desk. Calling your agent first adds a day and forfeits valuable response time. Open the claim, get a number on the call, and note the examiner's name + direct line. State the loss type, the time of discovery, and that you are beginning your duty-to-mitigate obligations now. Prompt notice is typically required within 24 to 48 hours.

What to say to your adjuster

"Loss occurred at [time]. Source was [burst pipe / roof leak / kitchen fire]. I am authorizing emergency mitigation now under my duty-to-mitigate clause."

Your policy's duty-to-mitigate clause requires you to prevent further damage — you do not need adjuster approval to start drying, tarping, or boarding up. Waiting for an adjuster before starting mitigation is one of the most common reasons for partial denials. Choose a restoration company that documents with daily moisture logs, provides a written scope, and bills insurance direct. Emergency mitigation costs are typically reimbursable even if the broader claim is contested.

What to say to your adjuster

"I have authorized Palm Build to begin emergency mitigation under the duty-to-mitigate clause. Daily moisture logs and a written scope are forthcoming."

Save every receipt: temporary repairs, hotel stays, meals out, laundromat, rental equipment, debris disposal. Start a single notebook or spreadsheet as your claim diary — every phone call, every name, every conversation summary, every promised callback. Additional Living Expense (ALE) or Loss of Use coverage typically reimburses displacement costs, but only with receipts. The claim diary is your single source of truth if the claim escalates to appraisal or litigation.

What to say to your adjuster

"I am tracking all mitigation and displacement costs. Current total is [\$X]. I will submit itemized receipts with the final claim package."

Before the adjuster arrives, organize your documentation into a single binder or shared folder: photos, receipts, moisture logs, a written scope from your restoration company, serial numbers and values on damaged contents. Walk the adjuster through every affected room. Point out hidden damage (under flooring, behind walls, in cavities). Ask the adjuster what software they write estimates in (almost always Xactimate) and confirm the next step + timeline in writing after the visit.

What to say to your adjuster

"Here is the full documentation binder. Let me walk you through each affected area. Please note the hidden damage behind [wall / floor / cabinet]."

When the adjuster's Xactimate estimate arrives, compare it line-by-line with your restoration company's scope. Common omissions: dehumidifier day-count, antimicrobial treatment, content pack-out, code upgrades, like-kind flooring, paint primer, baseboards. Push back in writing on every missing or under-priced line item. Use the exact Xactimate codes — this is the language adjusters understand. Your restoration company should help prepare the line-by-line rebuttal.

What to say to your adjuster

"Your estimate is missing [line item X] per Xactimate code [Y]. The restoration scope shows [\$Z]. Please supplement the estimate to include it."

Never accept the first offer verbally. Request the settlement breakdown in writing, review each line item, and respond in writing — ideally by email for a documented trail. If the offer is adequate, acknowledge in writing and confirm payment timing. If it is under-scoped, itemize the disputed line items and request supplemental review. A written response protects you if the claim later needs to be reopened or escalated.

What to say to your adjuster

"I have reviewed the settlement breakdown dated [date]. I accept line items [A, B, C] and dispute [D, E, F] for the following reasons: [itemize]. Please confirm next steps in writing."

Hidden damage is the rule, not the exception. Once demolition begins, your restoration company will find rotted subfloor, mold behind walls, compromised framing, code-upgrade requirements, or concealed water migration. Each discovery triggers a supplement — a request for additional funds beyond the original estimate. Supplements are a normal and expected part of every significant claim. Document the hidden damage with photos and a supplemental Xactimate estimate, and submit it promptly.

What to say to your adjuster

"During demolition we discovered [hidden damage]. I am submitting a supplemental Xactimate estimate and photos. Please confirm receipt and expected review timeline."

Most policies pay Actual Cash Value (ACV) upfront and release Replacement Cost Value (RCV) — the depreciation holdback — only after repairs are complete and you submit proof of completion. Do not leave this money on the table. Once rebuild is finished, submit the final invoice, photos of completed work, and a sworn statement of loss. The RCV release often equals 20 to 40 percent of the total claim. Track the release against the policy's time limit for recovery (commonly 180 or 365 days).

What to say to your adjuster

"Rebuild is complete. I am submitting the final invoice, completion photos, and sworn statement to release the depreciation holdback of [\$X]."

| Time window | Action |

|---|---|

| Minutes 0–5 | Confirm safety. Shut off water / power as appropriate. Evacuate if needed. |

| Minutes 5–15 | Start photographing and video-recording before moving anything. |

| Minutes 15–30 | Call the carrier claims line. Open the claim. Get a claim number. |

| Minutes 30–45 | Call a restoration company. Authorize emergency mitigation. |

| Minutes 45–60 | Start the claim diary. Log every call, name, and commitment. |

Palm Build coordinates insurance claims daily — documentation, Xactimate scope, adjuster meetings, supplement filing, and depreciation recovery. Call the 24/7 claims line to walk through your situation with a coordinator.

Thin documentation is the number-one reason claims are undervalued. This is the full checklist — organized by category — that Palm Build's insurance coordinators use on every residential and commercial loss. For the deeper walkthrough see our documenting damage sub-guide and how to document water damage for insurance.

Damaged flooring, baseboards, cabinets, and contents are evidence. The carrier has the right to inspect physical damage before disposal. Photograph and video everything, then stage damaged items in a garage or storage area until after the inspection. Throwing things away early is one of the most common reasons for claim denial.

Exception: items that pose a health or safety hazard (saturated carpet, Category 3 water, biohazard) may be removed for emergency mitigation. Document exhaustively before disposal and keep samples where possible.

Most homeowners assume they have one deductible. In hurricane states they often have three or four — and the percentage-based hurricane deductible is the one that surprises people most. A $400,000 home with a 5% hurricane deductible pays the first $20,000 out of pocket before the insurer pays a dollar. Dig into the specifics in our hurricane deductibles deep-dive guide.

Fire, theft, vandalism, non-hurricane water damage, lightning, and any non-wind covered peril.

Named storm systems when NWS issues a hurricane watch/warning for the area. Applies to all damage from that storm, not just wind. Florida coastal norm.

Wind or hail damage at any time (not just named storms). Common in inland states with hail exposure (NC, TX, OK, CO).

Loss during the time an NWS advisory, watch, or warning for a named storm is in effect for any part of NC. Set by NCIUA (Coastal Property Insurance Pool).

Applies only on NFIP flood claims — chosen separately for building and contents coverage. Completely separate from the homeowner deductible.

| Home coverage + % | Calculation | Out-of-pocket |

|---|---|---|

| $200,000 Coverage A, 2% hurricane deductible | $200,000 × 2% | $4,000 |

| $400,000 Coverage A, 2% hurricane deductible | $400,000 × 2% | $8,000 |

| $400,000 Coverage A, 5% hurricane deductible | $400,000 × 5% | $20,000 |

| $650,000 Coverage A, 5% hurricane deductible | $650,000 × 5% | $32,500 |

| $1M Coverage A, 10% hurricane deductible | $1,000,000 × 10% | $100,000 |

The single biggest confusion in storm claims: wind vs water, driven rain vs rising water, flood vs backup. Here are eight concrete scenarios and which policy actually pays. For a deeper read see wind damage vs flood damage insurance and our flood vs homeowners guide.

Wind, fire, theft, sudden water discharge, vandalism, hail, lightning, weight of snow

Flood, earthquake, gradual leaks, maintenance failure, intentional damage

Rising water from general surface condition affecting 2+ acres or 2+ properties, storm surge, mudflow, river overflow

Wind damage, non-rising water, ALE / loss of use, most finished basements (limited)

Wind and hail only — the wind peril that homeowner carriers excluded

Everything except wind / hail. Must pair with a homeowner policy that excludes wind.

| Scenario | Homeowner policy | NFIP flood | Verdict |

|---|---|---|---|

| Wind tears a hole in the roof; rain pours in through the opening | Covered (wind-driven rain through opening made by wind) | Not applicable — no rising water | Homeowners |

| Rainwater backs up through a clogged gutter and leaks into the ceiling | Excluded as maintenance failure unless policy specifies | Not applicable — no flooding | Often excluded |

| Storm surge from a hurricane pushes 3 feet of water into the ground floor | Excluded — this is flood | Covered if active NFIP or private flood policy | NFIP / flood |

| A nearby river overflows and water enters through the foundation | Excluded — this is flood | Covered if active NFIP or private flood policy | NFIP / flood |

| Hurricane wind blows over a tree that falls on the house | Covered — wind damage | Not applicable | Homeowners |

| Groundwater seeps up through the foundation during heavy rain | Excluded (seepage / groundwater) | Not covered unless meets NFIP definition of flood (general surface water condition affecting 2+ acres or 2+ properties) | Often no coverage |

| Burst pipe inside the home releases water | Covered — sudden and accidental water discharge | Not applicable — not flood | Homeowners |

| Mudflow from a hillside enters the home during a storm | Excluded (earth movement and flood) | Covered if meets NFIP mudflow definition | NFIP / flood |

The NFIP definition of flood matters. For NFIP to cover the loss, the water must be a "general and temporary condition of partial or complete inundation of normally dry land" affecting 2 or more acres or 2 or more properties. A single clogged gutter backup does not meet the definition. Neither does groundwater seepage. This is why so many storm claims fall between the two policies.

Property insurance is regulated state by state. Filing deadlines, hurricane deductibles, bad-faith remedies, and residual-market wind pools vary dramatically across our service area. Here are the statutes and regulators that actually affect your claim, with primary-source citations.

Florida is the most legislatively active insurance market in the country. Senate Bill 2A (effective December 16, 2022) fundamentally reshaped property claims law — shrinking deadlines, modifying bad-faith remedies, and eliminating one-way attorney fees that had driven litigation volume.

Under SB 2A, homeowners now have 1 year from the date of loss to report a new or reopened property claim (reduced from 2 years). Supplemental claims must be filed within 18 months (reduced from 3 years). This is the most important change in the entire reform package.

Fla. Stat. § 627.701 requires hurricane deductibles to be calculated as a percentage of dwelling coverage — typically 2%, 5%, or 10%. Deductibles apply per season, not per storm. Trigger is an NWS-named storm affecting any part of Florida.

Standard Florida HO-3 policies cover "catastrophic ground cover collapse" but not general sinkhole activity. Sinkhole loss coverage is a separate endorsement under Fla. Stat. § 627.706.

SB 2A eliminated the statutory right to assign benefits for property claims. This ended most AOB litigation but also ended one-way attorney fees for first-party claims. Homeowners now bear their own legal costs in most disputes.

Florida Department of Financial Services offers free claim mediation for residential property disputes under Fla. Stat. § 627.7015. Either party may request mediation; the insurer must pay the cost.

North Carolina's insurance code is codified in Chapter 58 NCGS. The state combines mainland inland exposure with significant coastal hurricane risk, addressed through the NC Insurance Underwriting Association (NCIUA) — formerly the Beach Plan, now officially the Coastal Property Insurance Pool.

NCGS Chapter 58 is the consolidated insurance code. Article 3 covers general provisions; Article 36 covers rate-making; Article 45 covers the NCIUA Coastal Property Insurance Pool. Consumer protections include prompt claim handling and unfair claims practice rules.

Homeowners in the 18 coastal and beach counties may need a separate NCIUA wind/hail policy if their admitted carrier has excluded wind. NCIUA is the market of last resort — a pool of licensed NC insurers providing essential wind coverage.

NCIUA named-storm wind/hail deductible is a minimum of 1% of insured value. Trigger is an NWS advisory, watch, or warning for a named storm affecting any part of North Carolina. Higher optional deductibles are available through the NC Rate Bureau.

NCGS § 58-63-15 prohibits unfair claim settlement practices including failure to acknowledge claims promptly, failing to adopt reasonable investigation standards, and not attempting prompt, fair, and equitable settlement.

South Carolina insurance law is codified in SC Code Title 38. The state has a more consumer-friendly bad-faith framework than Florida, with a statutory attorney-fees remedy for unreasonable claim refusals and the SC Wind and Hail Underwriting Association (SCWHUA) for coastal wind coverage.

SC Code § 38-59-20 defines improper claim practices. When committed "without just cause and performed with such frequency as to indicate a general business practice," violations include knowingly misrepresenting coverage, failing to acknowledge claims promptly, failing to adopt reasonable investigation standards, and not attempting prompt fair settlement.

SC Code § 38-59-40 provides that if an insurer refuses to pay a covered claim within 90 days after demand, and the trial judge finds the refusal was without reasonable cause or in bad faith, the insurer is liable for reasonable attorney fees. This is a homeowner-friendly remedy unique to SC.

The South Carolina Wind and Hail Underwriting Association provides essential wind and hail coverage in the designated Beach Zone. SCWHUA is the market of last resort for coastal properties when admitted carriers exclude wind.

SC House Bill 4733 (2025-2026 session) proposes a statutory bad-faith presumption in insurance settlements — a further strengthening of consumer remedies. Not yet law as of 2026; track status via the SC Legislature bill tracker.

Legal disclaimer: Statutory citations are current as of Q1 2026 based on primary sources. Insurance law changes. Always verify current statutes at the state legislature website before relying on any citation for legal action, and consult a licensed attorney for specific claim disputes.

Every professional on an insurance claim represents someone. Understanding who works for whom — and what they cost — is the difference between a paid claim and a denied one. For a deeper look at public adjuster economics see is a public adjuster worth it and our public adjuster guide.

Assigned by the carrier to investigate, scope, and settle your claim. They write the Xactimate estimate the carrier uses to set the settlement.

Contracted by carriers during catastrophe events (hurricanes, hail storms) when in-house staff cannot cover volume. Scope and settle claims under the carrier's guidelines.

Hired by the homeowner to document, scope, and negotiate the claim. They write their own Xactimate estimate and argue for a higher settlement.

Escalates denied or bad-faith claims to litigation or pre-suit demand. Uses statutory bad-faith remedies (SC § 38-59-40, FL § 624.155 pre-SB 2A for older claims).

| Situation | Recommended | Why |

|---|---|---|

| Straightforward small claim under $10k | Staff adjuster + good restoration company | Documentation from the restoration company usually drives a fair settlement without added fees. |

| Large-loss or complex multi-peril claim | Staff adjuster + restoration company; consider PA if disputes arise | Start with the carrier process. Escalate to a public adjuster if scope disputes grow. |

| Significantly underpaid settlement | Public adjuster for supplement negotiation | A PA can rewrite the scope, document missed items, and argue the higher estimate. |

| Claim denied outright | Attorney consultation (often free); public adjuster secondary | Denial disputes benefit most from legal review of the policy language and denial basis. |

| Carrier acting in bad faith — ignoring calls, delaying | Attorney | Statutory bad-faith remedies are legal remedies. PAs cannot file suit. |

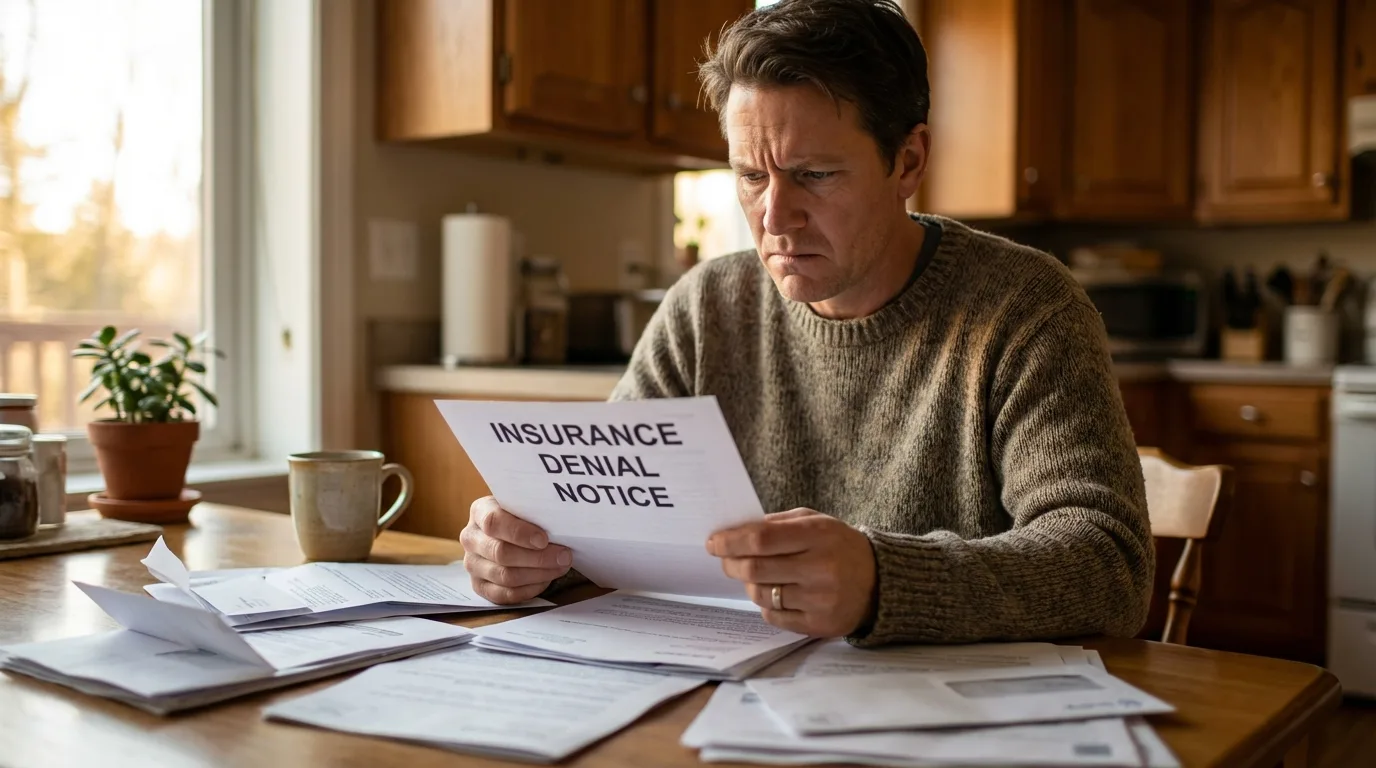

Most denials can be overturned with the right documentation and escalation path. Understanding the six most common denial reasons — and the seven-step appeal process — turns a denied claim into a paid one more often than homeowners expect. For specific tactics see denied water damage claim, carrier denial tactics, and our full denial guide.

Each has a distinct appeal strategy. Match your denial reason to the right approach.

The carrier classifies the loss as wear and tear, long-term leak, or deferred maintenance rather than a sudden and accidental event. Most common reason for water damage denials.

Submit a plumber or contractor report identifying the specific failure event. Temperature or pressure data can prove a sudden event. Photograph the failure point in detail.

The carrier argues the damage existed before policy inception or before the reported date of loss.

Produce prior inspection reports, home sale disclosures, real-estate photos, or prior homeowner records showing the undamaged condition before the loss.

The carrier argues the loss was caused by a peril specifically excluded: flood, earthquake, sewer backup (if no endorsement), mold (over sublimit), intentional damage.

Argue the proximate cause rule — if a covered peril (wind) caused an excluded peril (water), the loss may still be covered. Read the policy exclusion language exactly. In FL, anti-concurrent causation clauses complicate this.

The carrier denies for failure to provide prompt notice. FL now requires filing within 1 year of loss under SB 2A; most other states allow 2-3 years.

Demonstrate you provided notice as soon as reasonably possible after discovery. Document why notice was delayed (safety, access, discovery timing).

The carrier refuses payment for lack of photos, moisture readings, inventories, or specialist reports to support the claimed amount.

Supplement the file with the missing documentation. Public adjusters and restoration companies can often reconstruct documentation from moisture logs, drying reports, and Xactimate data.

Carrier argues the policy was not in force at the date of loss due to non-payment or cancellation.

Produce proof of premium payment. Review the cancellation notice for compliance with state notice requirements. Many lapse denials fall apart on close inspection of the notice sequence.

Start with step one. Escalate only if the prior step did not resolve the dispute. Each escalation adds leverage.

The denial letter must state the specific basis: which policy language, which exclusion, which factual finding. Highlight each claim and address them individually in your response.

Most states give the insured a right to their own claim file. Request all adjuster notes, photos, estimates, and internal documents. This is your paper trail for any escalation.

Cite the specific policy language, attach supporting documentation, and request a supervisor-level re-review. Send by email with read receipts and certified mail.

If the denial is based on factual findings (scope, cause, extent), demand a physical re-inspection with a different adjuster present. This often surfaces missed damage.

If the dispute is about dollar amount (not coverage), invoke the appraisal clause in the policy. Each side picks an appraiser; the two appraisers pick an umpire. Binding on amount.

File a formal consumer complaint with the state Department of Insurance. Carriers must respond in writing. Complaints trigger regulator scrutiny, which often accelerates resolution.

For bad-faith conduct (unreasonable delay, denial without basis, misrepresentation), an attorney can pursue statutory remedies. SC Code § 38-59-40 is particularly strong.

Two of the highest-value concepts in insurance claims: supplements for hidden damage discovered mid-project, and recovering the depreciation holdback after rebuild is complete. Together they can add 20 to 50 percent to a final settlement. Learn the supplement workflow from our supplemental claims guide and what is a supplement in insurance.

Replacement Cost Value (RCV) pays what it costs to replace damaged property with equivalent new materials. Actual Cash Value (ACV) deducts depreciation based on age, wear, and useful life remaining. On a typical RCV policy, insurers pay ACV first, then release the depreciation holdback only after repairs are complete and you submit proof of completion.

Why it matters: depreciation holdback can equal 20 to 40 percent of the total claim. Homeowners who never submit the final paperwork forfeit this money. Track the recovery deadline (commonly 180 or 365 days from the initial ACV payment).

A supplement is a formal request for additional insurance funds beyond the original estimate, covering damage or costs that were not known when the original scope was written. Supplements are normal and expected on every significant restoration claim — typically one to three per project.

Supplements are submitted as a separate Xactimate estimate with photos, sketches, and a clear narrative describing why the new scope was not visible during the original inspection. A quality restoration company files supplements as a normal part of project management, not as an exception.

| Item | RCV (full) | Depreciation | ACV first pay | Holdback to recover |

|---|---|---|---|---|

10-year-old asphalt shingle roof Released after roof is replaced and final invoice submitted. | $22,000 | $11,000 | $11,000 | $11,000 |

8-year-old water heater Depreciation based on 40% of useful life remaining. | $1,800 | $720 | $1,080 | $720 |

5-year-old luxury vinyl plank flooring Shorter effective life → lower depreciation holdback. | $14,500 | $3,625 | $10,875 | $3,625 |

15-year-old kitchen cabinets Older materials → larger depreciation holdback to recover. | $28,000 | $16,800 | $11,200 | $16,800 |

These are the discoveries your restoration company will surface during demolition and repair. Each triggers a formal supplement request to the carrier.

Discovered during demolition. Requires mold assessment report, moisture readings, and supplemental Xactimate scope for remediation work.

Revealed when flooring is removed. Structural repair or subfloor replacement becomes a line-item supplement.

Local building code may require electrical, plumbing, or structural upgrades beyond the scope of what was originally estimated.

Thermal imaging or tear-out reveals water that migrated beyond the originally identified area. More drying, more demo, more rebuild.

Older homes may contain regulated materials discovered during demo. Abatement cost is typically covered as a supplement.

Items originally thought intact may show damage once cleaning begins (smoke, odor, structural deformation).

Most policies give you 180 to 365 days from the date of ACV payment to submit proof of completion and recover the depreciation holdback. Some carriers extend on request; others do not. File the final invoice, completion photos, and sworn statement of loss promptly after rebuild. This is the single most-forfeited category of claim money — do not leave it on the table.

Your Claims Advocate

We handle insurance claims every day. Our documentation, estimating, and adjuster coordination are designed to maximize your coverage and minimize your stress.

Our crews capture comprehensive photo and video documentation from the moment we arrive — before, during, and after every phase of work. This visual evidence is often the difference between a quick settlement and a prolonged dispute.

We record moisture levels throughout the drying process using calibrated meters and thermal imaging. These objective measurements prove the full scope of hidden water damage and justify every square foot of tear-out.

We prepare detailed Xactimate estimates using the same software and pricing databases your adjuster uses. When our estimate speaks their language, approvals come faster and disputes are minimized.

Our project manager meets the adjuster at your property to walk through every area of damage together. We point out damage that might be missed and provide professional opinions on repair vs. replacement decisions.

When we discover damage behind walls, under floors, or in other concealed areas during restoration, we document it immediately and file supplemental claims with photos and revised estimates. This is normal and expected.

We handle the billing paperwork with your insurance carrier so you typically only pay your deductible out of pocket. We coordinate payments, track depreciation holdbacks, and follow up on outstanding balances.

Deep-Dive Guides

Each guide below tackles a specific aspect of the insurance claims process in detail. Bookmark what applies to your situation and come back anytime.

Complete guide to photographing, inventorying, and documenting property damage for the strongest possible claim.

What homeowners, flood, and windstorm insurance actually cover — and the exclusions that catch people off guard.

Why claims are denied, how to appeal, and when to escalate with a public adjuster or attorney.

Hurricane deductibles, Citizens Insurance, AOB reforms, and FL-specific resources every Florida homeowner should know.

How to prepare for the adjuster visit, what to expect, and how to ensure nothing is missed during the inspection.

When to hire a public adjuster, what they cost, how they work, and the honest pros and cons.

The critical first-hour checklist: safety, documentation, mitigation, and insurer notification in the right order.

How percentage-based hurricane deductibles work in Florida and coastal states, and why they surprise so many homeowners.

When and why supplemental claims are filed, how they work, and why they are a normal part of every significant restoration project.

The critical difference between flood and homeowners insurance, why it matters after storms, and how to avoid coverage gaps.

NC-specific insurance guidance, DOI resources, coastal wind coverage, and what NC homeowners need to know.

How deductibles, ACV vs. RCV, direct billing, depreciation holdback, and payment flow work during a restoration claim.

Twelve hand-picked blog deep dives grouped by subtopic, from claim filing and coverage questions to hurricane deductibles, denial appeals, and public adjuster economics.

Trusted Resources

These government agencies and industry organizations provide free assistance, consumer protections, and standards that apply to your restoration claim.

Consumer helpline for insurance complaints, claim disputes, and hurricane claim mediation.

Consumer assistance, complaint filing, and post-disaster insurance help for NC homeowners.

Consumer protection, complaint resolution, and insurance market information.

Federal flood insurance claims, flood maps, and disaster assistance programs.

Sets the restoration industry standards (S500 for water, S520 for mold) that guide proper mitigation and help justify claim scope.

Disclaimer: This page provides educational information, not legal advice. For specific questions about your policy or claim, consult with your insurance agent, a licensed public adjuster, or an attorney.

Local Service Pages

Tier 4 · Local office

Tier 2 · Local office

Tier 1 · Local office

Tier 1 · Local office

Tier 1 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 1 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 4 · Local office

Tier 4 · Local office

Tier 2 · Local office

Tier 1 · Local office

Tier 1 · Local office

Tier 1 · Local office

Tier 1 · Local office

Tier 4 · Local office

Tier 4 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 4 · Local office

Tier 4 · Local office

Tier 3 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 3 · Local office

Tier 4 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 1 · Local office

Tier 4 · Local office

Tier 1 · Local office

Tier 2 · Local office

Tier 2 · Local office

Tier 3 · Local office

Tier 2 · Local office

Tier 1 · Local office

Tier 1 · Local office

Tier 3 · Local office

Tier 2 · Local office

Related Restoration Services

Insurance claims touch every part of property restoration — from initial mitigation through rebuild. Use these connected guides to align scope, documentation, and timelines.

Water damage claims require documented moisture readings, drying logs, and photo evidence from extraction through completion.

Fire loss claims involve structural damage, contents inventory, smoke remediation, and coordinated rebuild scope.

Mold coverage varies by policy and state. Understand triggers, documentation standards, and exclusion language.

Storm claims often involve wind-versus-water disputes, supplement requests, and multi-carrier coordination.

Rebuild scope aligns with insurance estimates. Coordinate Xactimate line items, permits, and completion timelines.

Commercial claims add business interruption, code upgrade requirements, and multi-stakeholder documentation.

Step-by-step storm damage claim guide for Florida, North Carolina, and South Carolina. Documentation checklists, adjuster scripts, deadlines, supplements.

14 min read

File your water damage insurance claim the right way. 7 steps to document, report, and protect your payout, plus FL/NC/SC filing deadlines you need to know.

13 min read

Palm Build Tools

These tools help you think through claim-worthiness, cost exposure, storm triage, and timeline expectations before the first adjuster or contractor conversation.

Estimate claim-worthiness, likely out-of-pocket exposure, and the next documents to gather before you call.

Pair coverage questions with a more grounded cost range so the deductible conversation is easier to judge.

Start with same-day hazard and scope triage before moving into claim-readiness planning.

Translate mitigation, approvals, permits, and rebuild sequencing into a timeline stakeholders can actually follow.

Answers about filing insurance claims after property damage, working with adjusters, documentation requirements, denial appeals, and how restoration companies coordinate with your insurance carrier.

Ensure safety first — evacuate if necessary, shut off water or power to affected areas. Then document everything with photos and video before touching anything. Call your insurance company within the first hour to report the claim and get a claim number. Begin emergency mitigation (water removal, tarping, board-up) immediately — your policy requires you to prevent further damage. Do not wait for the adjuster before starting mitigation. Start a claim diary noting every call, name, and conversation.

Still have questions about filing your claim?

Most homeowners file one or two insurance claims in their lifetime. We handle them every single day. Our team documents, coordinates with adjusters, and advocates for full claim recovery so you can focus on getting your life back to normal.

Daily insurance coordination

Photos, moisture logs, estimates

We speak their language

Emergency mitigation and filing

Need help right now? Call us.

24/7 live dispatch — average answer time under 30 seconds