Quick Answer

Usually only when the mold is the direct result of a sudden, accidental covered peril — like a burst pipe or an overflowing appliance — and even then a separate 'fungi' or mold sublimit often caps what the policy pays. Mold from gradual leaks, humidity, neglect, or flooding is typically excluded.

Key takeaways

- Mold is rarely covered on its own. It is paid (if at all) as 'resulting damage' from a covered water loss like a burst pipe — not as a stand-alone mold problem.

- Even a covered claim is usually capped. Most policies apply a separate mold or 'limited fungi' sublimit, commonly $1,000 to $10,000, that can be far less than the actual remediation bill.

- Mold from gradual leaks, humidity, neglect, or flooding is typically excluded. Flood-caused mold needs separate flood coverage, and the NFIP excludes mold you could have prevented.

- Professional mold remediation averages about $2,368 for one area (most projects run $1,200 to $3,800); larger or whole-home jobs reach $3,500 to $9,000 or more.

- State rules change the decision: Florida licenses mold assessors and remediators and sets strict claim deadlines, while North Carolina and South Carolina currently license neither — making contractor vetting and fast documentation critical.

Does homeowners insurance cover mold? In most cases, only when the mold grows out of a sudden, accidental event your policy already covers — a burst supply line, a ruptured water heater, or water used to put out a fire. Even then, mold is treated as "resulting damage" from that water loss, and most policies cap it with a separate 'fungi' or mold sublimit that can be far smaller than the actual bill. Mold tied to slow leaks, high humidity, deferred maintenance, or flooding is usually excluded outright. Because colonies can take hold in 24 to 48 hours, how fast you dry and document the loss often decides both your health outcome and your claim. In Florida, North Carolina, and South Carolina, licensing rules and claim deadlines add another layer — and that is where most national guides stop.

Average professional mold remediation for one affected area (HomeAdvisor, 2025-26)

$2,368

What most single-area mold remediation projects cost, before any deductible

$1,200-$3,800

How fast mold can start growing on a damp surface (EPA, FEMA)

24-48 hrs

EPA threshold below which mold cleanup is often a safe DIY job

10 sq ft

When Homeowners Insurance Does Cover Mold

Insurers do not "cover mold" as a category. They look at the water event behind the mold and ask three questions: was the cause a covered peril, was it sudden and accidental (not gradual), and did you act reasonably fast to limit the damage? When the answer to all three is yes, mold is usually paid as resulting damage from that covered water loss — subject to your deductible and your mold limit.

The scenarios national publishers and adjusters most often approve share the same DNA: a clear, single "release event" followed by prompt cleanup. Common examples include a burst or frozen pipe, a sudden appliance failure (a washing machine hose or water heater), and mold that develops after water is used to extinguish a fire. That last one is why a fire claim and the mold scope are handled together — coordinate emergency water extraction and drying and fire and smoke cleanup before secondary mold sets in.

| Mold scenario | Typically covered? | What makes the difference |

|---|---|---|

| Mold after a burst or frozen pipe you found fast | Often yes — but capped by the mold sublimit | A sudden "release event" plus drying within 24-48 hours is the strongest pattern insurers approve |

| Mold after a sudden appliance leak (washer, water heater) | Usually yes, as resulting damage | Save the failed part, photos, and a plumber's note; the appliance repair itself is usually not covered |

| Mold after water used to put out a fire | Often yes | Tied to a covered fire loss; the mold and fire scopes are documented together |

| Mold after a storm-created roof opening | Sometimes — if the storm, not wear, made the opening | Document missing shingles or punctures and the storm date; worn-out roofs are excluded |

How adjusters typically treat common mold scenarios. This is not legal advice; policy language and limits vary by carrier and state.

When Mold Is Not Covered

The flip side is just as predictable. Insurers treat mold as the homeowner's responsibility when the moisture behind it was gradual, preventable, or the wrong type of water. The clause cited in the denial letter is rarely "mold" — it is maintenance, continuous seepage, humidity, or flood.

Mold insurers usually pay for

- Mold from a burst or ruptured supply line

- Mold after a sudden appliance failure

- Mold from water used to extinguish a fire

- Mold behind a storm-created roof opening you reported quickly

- Mold you mitigated and documented within 24-48 hours

Mold insurers usually deny

- Mold from a slow leak found weeks or months later

- Mold from humidity, condensation, or poor ventilation

- Mold from flooding or storm surge (needs a flood policy)

- Mold from a sewer or drain backup (needs water-backup coverage)

- Mold you knew about and left unaddressed

| Mold scenario | Typically covered? | Exclusion usually cited |

|---|---|---|

| Slow drip under a sink found months later | No | Gradual leak / lack of maintenance |

| Bathroom, attic, or HVAC mold from humidity | No | Humidity, condensation, and ventilation |

| Mold after flooding or storm surge | No — needs a flood policy | Flood excluded; NFIP excludes avoidable mold |

| Mold from a sewer or drain backup | No, unless you bought water-backup coverage | Water/sewer backup exclusion |

| Mold you knew about and left unaddressed | No | Neglect / failure to mitigate |

Denied mold scenarios and the policy clause usually behind the denial.

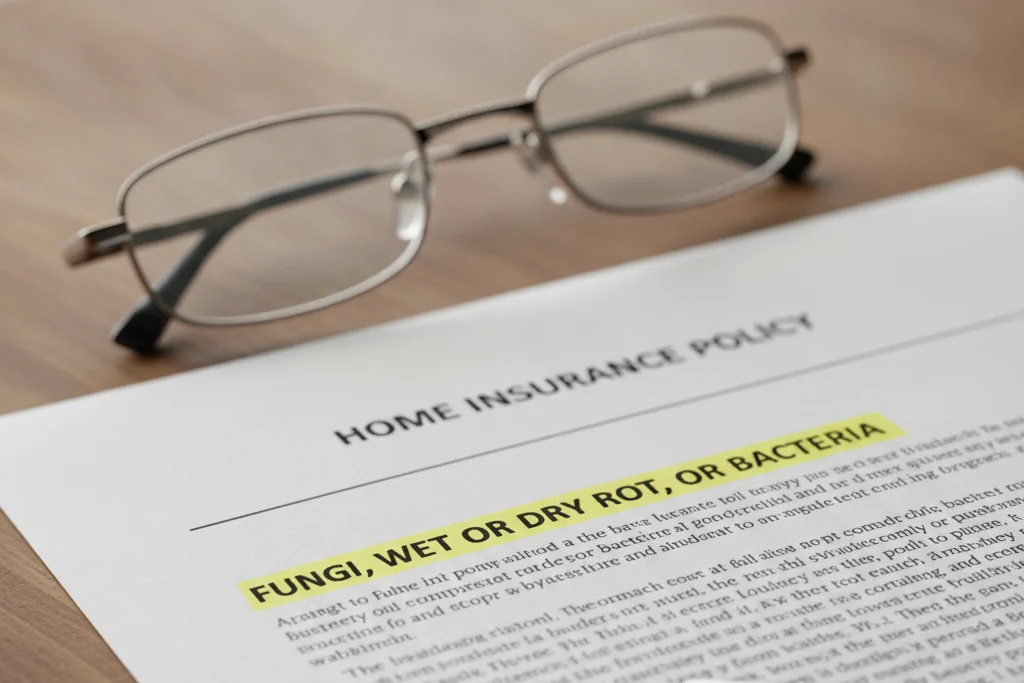

The Catch: Mold Sublimits and 'Limited Fungi' Coverage

Here is the part most homeowners miss until they get the check: even when mold is covered, it is usually covered to a point. Most policies apply a separate mold or "limited fungi" sublimit — a smaller cap that sits underneath your dwelling and contents limits and applies specifically to mold, fungi, wet or dry rot, and bacteria. Common sublimits run from about $1,000 to $10,000, and they exist precisely because carriers want to contain mold exposure.

That creates a frustrating mismatch. A covered burst pipe might pay generously to replace flooring and drywall, but if the mold cleanup runs $6,000 and your fungi sublimit is $2,500, you absorb the difference plus your deductible. The National Association of Insurance Commissioners notes that many standard policies offer limited or no mold coverage, and that you may be able to buy an endorsement to add or raise it — which only helps if you do it before the loss. Check your declarations page for a "fungi, wet or dry rot, or bacteria" limit, and ask your agent two questions: what is my mold cap, and can I raise it?

How Much Mold Remediation Costs (and Why Limits Matter)

Knowing the real cost of remediation tells you two things: whether filing a claim is even worth it against your deductible and sublimit, and whether a low mold cap leaves you exposed. The numbers below reflect current 2025-2026 consumer cost data; your project can land anywhere in the range depending on how much material is affected and whether your HVAC is involved.

| Cost item | Typical range | Notes |

|---|---|---|

| Mold inspection / testing | $300-$1,050 (avg ~$670) | A basic mold test runs about $250-$500; often separate from any covered claim |

| Professional remediation (one area) | $1,200-$3,800 (avg ~$2,368) | Rises fast when walls, HVAC, or multiple rooms are involved |

| Per square foot | $10-$25 / sq ft | Useful for quick estimates; not a guarantee |

| Larger or whole-home remediation | $3,500-$9,000+ | Major water damage, extensive demolition, or HVAC contamination |

Typical U.S. mold inspection and remediation costs (HomeAdvisor, Bob Vila, Fixr, 2025-2026). Coverage and any mold sublimit vary widely by policy and state.

Put the cost against the cap. If your deductible is $2,500 and your mold sublimit is $2,500, a $3,800 remediation may net you almost nothing after the math — paying out of pocket can be simpler and keeps a claim off your record. Our mold remediation cost guide breaks pricing down by scope, and the insurance claim estimator helps you sanity-check coverage before you file.

When filing a mold claim makes sense — and when it doesn't

Filing usually makes sense

- The mold clearly traces to a sudden, covered water event

- Expected cost comfortably exceeds your deductible plus the mold sublimit

- You have photos, moisture readings, and a documented timeline

- Reconstruction (drywall, flooring, framing) is also needed

Paying out of pocket may be smarter

- The job is small and close to or under your deductible

- Your mold sublimit is low and the cause is borderline

- The moisture looks gradual and a denial is likely

- You want to avoid a claim on your loss history for a minor job

Insurance Claim Estimator

Estimate your likely coverage, deductible exposure, and out-of-pocket cost before you file.

Mold Growth Risk Calculator

Gauge how quickly your conditions can grow mold after a water event.

Florida, North Carolina & South Carolina: The Rules That Change Your Decision

The coverage logic above is national. What differs by state is who is allowed to do mold work, how fast you must report a claim, and what your carrier owes you in return. This is the layer national publishers skip — and it directly affects how you choose a contractor and protect a mold claim across the Southeast.

Florida: Licensed mold pros, a 12-month conflict rule, and strict claim deadlines

Florida is one of the few states that licenses mold professionals. Under Florida Statutes Chapter 468, Part XVI, the Department of Business and Professional Regulation licenses two roles — mold assessors and mold remediators — for any mold job larger than 10 square feet. The law also builds in a conflict-of-interest safeguard: the company that assesses your mold generally cannot also remediate the same structure within 12 months, and vice versa (with a narrow exception for certain licensed contractors who must disclose your right to competitive bids). On top of that, licensed assessors must carry at least $1 million in general and professional liability insurance, and remediators at least $1 million in general liability that covers mold claims. The takeaway for homeowners: in Florida, verify the license before you hire.

Florida also sets hard deadlines to report a property claim — one year from the date of loss for an initial claim and 18 months for a supplemental claim. That matters for mold specifically, because mold often surfaces weeks after the water event, and late reporting can sink an otherwise covered loss. We cover the timing in depth in Florida's 1-year water damage claim deadline.

North Carolina: No mold license, so vet for IICRC S520

North Carolina does not license or certify mold assessors or remediators — no state or federal certification is required to do the work. NC State Extension steers homeowners toward the industry benchmark instead: the ANSI/IICRC S520 Standard for Professional Mold Remediation. Because anyone can hang a shingle, the burden is on you to confirm IICRC training, references, and a written remediation protocol. Note that any associated repair or reconstruction over $40,000 does require a North Carolina general contractor license — a separate rule from mold work. On claims, the NC Department of Insurance expects insurers to acknowledge a claim within 30 days, but there is no fixed settlement deadline, which is one more reason not to wait on mitigation.

South Carolina: No licensing yet — and a 2026 bill that stalled

As of the 2026 legislative session (which adjourned in May 2026), South Carolina does not require a license or certification to perform mold assessment or remediation. A bill to change that — H. 5109, which would have created a mandatory certification program and a state Mold Assessment and Remediation Board — was introduced on February 5, 2026, but it stalled in House committee and did not become law. Similar bills have failed in prior years, so verify the current status before relying on it. Until then, vet your South Carolina mold remediation contractor the same way you would in North Carolina: IICRC credentials and S520 practices. On the claims side, South Carolina requires insurers to furnish a proof-of-loss form within 20 days if they require one, and a separate bad-faith statute can expose carriers that refuse to pay covered claims without reasonable cause.

| Florida | North Carolina | South Carolina | |

|---|---|---|---|

| Mold contractor licensing | Yes — state licenses Mold Assessors & Remediators (DBPR) | None — vet for IICRC S520 | None yet — 2026 bill (H. 5109) stalled |

| Notable rule | Assessor cannot remediate the same home within 12 months; $1M insurance required | GC license needed for repairs over $40,000 | Proof-of-loss form due within 20 days if required |

| Claim-notice timing | 1 year to report; 18 months for supplemental | Insurer acknowledges within 30 days | Adjuster contact typically within 48 hours |

| Climate driver | Humidity + June 1-Nov 30 hurricane season | Humid summers; post-storm wind-vs-flood disputes | Hot, humid subtropical summers |

Mold rules and claim timing at a glance across Palm Build's core states. Verify current statutes and licensing before you rely on them.

Found Mold or Water? Do This to Protect Your Home and Your Claim

Whether your loss ends up covered or not, the first 48 hours decide most of it. The same actions that protect your health also build the "sudden and accidental" record adjusters look for. Move in this order.

- 1

Stop the water and stay safe

Shut off the source if you can reach it safely. Keep clear of standing water near electrical systems until power is off. Stopping the moisture is step one for both safety and coverage.

- 2

Document everything before you touch it

Photograph and video the water source, the standing water, every affected room, and any failed appliance serial numbers. This timeline is your strongest claim evidence, and it is gone the moment cleanup starts.

- 3

Report the loss promptly

Call your insurer, ask what documentation and proof-of-loss forms they need, and log every call. "Prompt notice" is a policy duty, and in Florida it is also a statutory deadline.

- 4

Start mitigation and dry within 24-48 hours

Your policy includes a duty to prevent further damage, so begin extraction and drying right away — do not wait for the adjuster. The EPA and CDC both stress drying water-damaged materials within 24 to 48 hours to keep a water loss from becoming a mold loss. Professional water damage restoration with moisture logs documents that you acted.

- 5

Bring in a pro for anything past a small patch

The EPA says mold under about 10 square feet is often a DIY job; beyond that — or with porous materials, HVAC involvement, or contaminated water — you need containment and HEPA filtration. That is the line where professional mold remediation protects both your lungs and your claim.

Hour 0-2

Stop the source and document

Shut off the water, photograph everything, and move valuables out. The clock on both mold and your claim starts now.

Hour 2-24

Extract and start structural drying

Standing water out, air movers and dehumidifiers in. Begin a moisture log so you can prove the surfaces are drying.

Hour 24-48

The mold window

Mold can begin colonizing damp materials in this window. Verified drying here is what keeps a water claim from becoming a mold claim — more in how fast mold grows after water damage.

After 48 hours

Colonization and coverage risk

Once mold is established, costs climb and insurers start asking whether delay caused the spread — the most common reason mold portions get reduced.

Key Mold-Insurance Terms

- Mold or 'limited fungi' sublimit

- A separate, lower dollar cap your policy applies to mold, fungi, wet or dry rot, and bacteria — often $1,000 to $10,000 — even when the underlying water loss is covered. It can be far less than the actual remediation bill.

- Limited fungi endorsement

- An optional add-on that adds or raises mold coverage. Because many standard policies offer limited or no mold coverage, an endorsement is often the only way to close the gap — and it has to be in place before the loss.

- Resulting damage

- Secondary damage that flows from a covered event. Mold is usually paid, if at all, as resulting damage from a covered water loss — not as a stand-alone problem.

- Covered peril

- A cause of loss your policy lists as covered — a sudden, accidental event like a burst pipe, not gradual wear or neglect. Mold coverage rides entirely on whether the water event was a covered peril.

- Mold assessor vs. remediator

- In licensed states like Florida, the assessor inspects and writes the protocol while the remediator does the removal. Florida bars the same company from doing both on one home within 12 months to prevent a conflict of interest.

- ANSI/IICRC S520

- The industry's consensus Standard for Professional Mold Remediation (4th edition, 2024). In states with no mold license, following S520 — containment, HEPA filtration, and verified drying — is the mark of a qualified contractor.

Related Guides & Next Steps

Professional Mold Remediation

IICRC S520 containment, HEPA filtration, and moisture control across FL, NC, and SC.

Insurance Restoration Process

How we coordinate adjusters, estimating, and the documentation that supports your coverage.

Does Homeowners Insurance Cover Water Damage?

The companion guide to the water losses that trigger most covered mold claims.

Mold Remediation Cost Guide 2026

Current pricing by scope so you can weigh a claim against your deductible and sublimit.

How Fast Does Mold Grow After Water Damage?

Why the 24-48 hour window decides both your health and your claim outcome.

Florida's 1-Year Water Damage Claim Deadline

The statutory deadlines that can bar a late mold claim in Florida.

Frequently Asked Questions

Does homeowners insurance cover mold removal? +

Does homeowners insurance cover black mold? +

Is mold from a roof leak covered? +

Does insurance cover mold testing or inspection? +

Does flood insurance cover mold? +

How fast does mold grow after water damage? +

What is a mold sublimit, and why does it matter? +

When should I call a professional instead of cleaning mold myself? +

Mold after a water loss? Protect your home and your claim.

Palm Build's IICRC-certified crews handle mold remediation, drying, and reconstruction across Florida, North Carolina, and South Carolina — with documentation built for your insurer and 24/7 emergency response. Start with a mold assessment or talk through your coverage.

Found this helpful? Send it to someone who needs it.