Storm & Hurricane Damage Restoration in Hallandale Beach, FL

Hallandale Beach is Broward County's southernmost coastal city — 45,000 residents packed into 4.4 square miles flanked by the Atlantic Ocean and the Intracoastal Waterway. FEMA has documented repetitive-loss properties here, sea-level rise has increased tidal flooding 5–10× since the 1960s, and the April 2023 event dropped over 22 inches nearby. High-rise condominium towers and CBS single-family homes in Golden Isles and Three Islands face simultaneous wind and storm-surge exposure from every major hurricane. Palm Build responds from our Deerfield Beach hub — approximately 15 miles away — with emergency tarping, saltwater extraction, tile-roof repair, and full HVHZ-compliant reconstruction, with insurance coordination from the first call.

Deerfield Beach — approximately 15 miles from Hallandale Beach 30-40 min Response IICRC Certified

Why Hallandale Beach Is Uniquely Vulnerable to Hurricane Damage

Hallandale Beach occupies one of the most storm-exposed positions in all of South

Florida. The city's Atlantic Ocean coastline and Intracoastal Waterway corridor create

storm-surge pathways from two directions simultaneously. FEMA repetitive-loss

designations, documented tidal flooding that has increased 5–10 times since the 1960s,

and a housing stock dominated by high-rise condominiums and CBS concrete block homes

with barrel tile roofs make Hallandale Beach a uniquely challenging storm restoration

environment.

Palm Build responds to Hallandale Beach from our Deerfield Beach operations hub —

approximately 15 miles away. When a hurricane threatens South Broward, our crews are

pre-staged and ready to deploy across every Hallandale Beach neighborhood within minutes

of the all-clear.

~170 mph

HVHZ design wind

5–10×

Tidal flooding increase since 1960s

30-40 min

Response from Deerfield Beach hub

Zone A

Hallandale Beach's highest surge exposure

Hallandale Beach's Atlantic coastline and Intracoastal Waterway create dual

storm-surge pathways into its dense residential and high-rise condo corridor

Atlantic Ocean + Intracoastal Waterway Exposure

Hallandale Beach is Broward County's southernmost coastal city, flanked by the Atlantic Ocean to the east and the Intracoastal Waterway threading through its western residential corridor. During a hurricane, storm surge approaches from two directions simultaneously — ocean surge from the east and Intracoastal push from the west. Golden Isles waterfront homes and Three Islands condos face direct saltwater Category 3 exposure every time a major storm tracks across South Florida's coast.

HVHZ Design Wind ~170 mph

All of Broward County — including Hallandale Beach — sits within the High-Velocity Hurricane Zone (HVHZ). The Florida Building Code mandates design wind speeds of approximately 170 mph, impact-rated windows and doors, and Florida Product Approval or Miami-Dade NOA for all exterior products. Any storm restoration or reconstruction must be permitted through the City of Hallandale Beach Building Division and comply with Florida Building Code 8th Edition (2023), ASCE 7-22.

FEMA Repetitive-Loss Properties & Tidal Flooding

FEMA has documented repetitive-loss properties in Hallandale Beach — locations that flood repeatedly under the NFIP program. Sea-level rise has increased tidal flooding frequency 5–10 times since the 1960s along this stretch of South Florida coast (NOAA). The April 2023 extreme rainfall event dropped over 22 inches nearby, flooding streets across the city. Higher baseline water levels mean less drainage capacity when hurricanes arrive.

Dense High-Rise Condo Stock — Complex Restoration

With roughly 45,000 residents in just 4.4 square miles, Hallandale Beach is one of Broward County's most condo-dense cities. High-rise towers — like those in the Diplomat Resort Area and along Three Islands — face elevated wind speeds on upper floors, balcony door failure under hurricane pressure, and shared assembly water migration between units. HOA master-policy coordination and individual HO-6 coverage separation add insurance complexity that requires specialized documentation.

Neighborhood Storm Risk Profiles

Hallandale Beach's Most Storm-Vulnerable Neighborhoods

Storm damage in Hallandale Beach concentrates along predictable corridors. Golden Isles

and Three Islands carry Very High storm surge exposure in Evacuation Zone A. The

Diplomat Resort Area faces direct Atlantic wave action. Interior neighborhoods like

Gulfstream Park and Village on the Green see primarily wind and drainage flooding risks.

Understanding your neighborhood's specific risk profile determines your insurance needs,

evacuation planning, and the type of storm restoration your property will require.

Golden Isles

Very High

Evacuation Zone A — Very High Storm Surge

Golden Isles is Hallandale Beach's most storm-vulnerable neighborhood. This waterfront single-family enclave sits directly on finger canals connected to the Intracoastal Waterway, with Atlantic Ocean exposure just beyond. During hurricanes, storm surge pushes from both the Atlantic to the east and the Intracoastal to the west, surrounding properties with saltwater simultaneously. Saltwater Category 3 contamination is guaranteed during any significant surge event. CBS homes here carry high property values ($600K–$2M+), creating the city's largest single-loss exposure from a combination of wind, surge, and structural damage.

Three Islands

Very High

Evacuation Zone A — High Storm Surge Exposure

Three Islands is a dense condo community built on a series of islands surrounded by the Intracoastal Waterway. High-rise and mid-rise towers face simultaneous wind exposure on upper floors and storm-surge risk at ground and parking levels. When surge or tidal flooding reaches lobby entrances and parking garages, saltwater Category 3 water requires full demolition of all affected porous materials. FEMA flood zone designations here mandate flood insurance for federally-backed mortgages. HOA master-policy coordination adds layers to every hurricane claim.

Diplomat Resort Area

Very High

Coastal Zone — Wind & Surge Combined Exposure

The Diplomat Resort Area along Collins Avenue faces direct Atlantic Ocean exposure. Oceanfront and near-ocean condos and hotels sustain direct wave action during hurricane landfalls, with wind speeds amplified at elevation. Impact-rated glazing and HVHZ-compliant construction help, but failed balcony doors or aged sealants allow Category 3 saltwater to penetrate interior spaces. The area's hospitality infrastructure creates complex restoration scopes — commercial and residential units sharing the same building systems.

Gulfstream Park Area

High Risk

Interior Zone — Wind & Drainage Flooding

The Gulfstream Park area — centered on the mixed-use racetrack and casino complex — sits inland from the Intracoastal and away from direct surge exposure. Primary storm risks are wind damage to roofing, screen enclosures, and signage; heavy rainfall overwhelming drainage; and wind-driven rain intrusion through aging stucco facades. Lower flood insurance pressure here than coastal zones, but wind deductibles still apply. CBS construction common in surrounding residential blocks.

Village on the Green

High Risk

Interior Condo — Wind & Rainfall Flood Risk

Village on the Green is a mid-density residential condo community west of Federal Highway. Primary storm risks are wind damage to older roofing systems, screen enclosure destruction, and localized drainage flooding when stormwater systems are overwhelmed by hurricane rainfall. HOA insurance complexity adds layers to every claim — master policy versus unit-owner HO-6 coverage. Aging 1970s–80s construction in some buildings predates current wind-load engineering standards.

CBS Single-Family — West of US-1

Moderate

Zone B/C — Wind Primary, Canal Drainage Risk

Single-family CBS stucco homes west of Federal Highway face the city's primary hurricane threat: wind damage to barrel tile roofs and wind-driven rain intrusion through stucco and sealant failures. Not in the highest surge zones, but tidal flooding that has increased 5–10 times since the 1960s can back up through storm drains even in these inland blocks during extreme events. Flood insurance is strongly recommended even if not required by mortgage — over 25% of NFIP claims nationally come from properties outside special flood hazard areas.

Evacuation Zones & Storm Damage Claims

Zone A vs. Zone B: What Your Evacuation Zone Means for Storm Damage

Broward County divides Hallandale Beach into evacuation zones based on storm surge

vulnerability. Zone A covers properties east of the Intracoastal Waterway — including

Golden Isles, Three Islands, and oceanfront residences. Zone B covers properties east of

Federal Highway (US-1). Your zone determines not just when you evacuate, but what type

of storm damage your property will sustain, which insurance policies cover it, and how

aggressive the restoration protocol must be.

Zone A — East of Intracoastal

Evacuates for ANY hurricane

Areas: Golden Isles waterfront homes, Three Islands

condos, Diplomat Resort Area, barrier island, all oceanfront and Intracoastal-front properties

Primary threat: Direct saltwater storm surge from

the Atlantic Ocean and Intracoastal Waterway. Category 3 (grossly contaminated) water

requiring full demolition of all affected porous materials. Golden Isles finger canal

system amplifies surge penetration from multiple directions simultaneously.

Insurance impact: FEMA VE/AE zones require flood insurance

for federally-backed mortgages. NFIP premiums are highest in Zone A. Homeowners policy

covers wind; flood policy covers surge. Both claims filed separately with different deductibles.

Restoration Reality

Zone A properties hit by surge face the most expensive restoration: full Category 3

saltwater decontamination, demolition of all porous materials below the waterline,

anti-corrosion treatment of structural steel and fasteners, and complete interior

rebuild. Typical cost: $50,000–$200,000+ depending on surge height and property size.

Zone B — East of Federal Hwy

Evacuates for Category 3+ storms

Areas: Village on the Green portions, central Hallandale

Beach neighborhoods between Federal Highway and the Intracoastal

Primary threat: Wind damage to roofing and structure,

drainage system overflow from extreme hurricane rainfall, tidal flooding backup through

storm drains. Diminished but not eliminated surge risk from Intracoastal water pushed

through drainage connections.

Insurance impact: FEMA AE or AH zones in lower-lying

areas. Flood insurance strongly recommended even if not required by mortgage. Drainage

overflow damage is excluded from homeowners policies — only covered by separate flood

policy. Wind damage subject to 2–5% hurricane deductible.

Restoration Reality

Zone B properties typically face combined wind and water damage: displaced barrel

tiles, wind-driven rain intrusion through stucco cracks, and potential drainage

flooding. Dual claims (wind to homeowners, flood to NFIP/private) are common. Typical

cost: $15,000–$75,000 depending on damage severity and whether flooding occurred.

West of Federal Hwy: Not in an Evacuation Zone, But Not Safe from Storm Damage

Properties west of Federal Highway — including Gulfstream Park area and inland CBS

subdivisions — are not in a mandatory evacuation zone. But tidal flooding that has

increased 5–10 times since the 1960s can back up through storm drains into streets even

during non-hurricane high-tide events. Hurricane-force winds affect every neighborhood in

the city equally. With FEMA repetitive-loss properties documented in Hallandale Beach and

sea level rise compressing storm-drain capacity every year, no neighborhood is truly

immune. Flood insurance is essential regardless of your evacuation zone.

How Hurricanes Damage Hallandale Beach Homes and Condos

Hurricane and storm damage in Hallandale Beach manifests in six distinct ways — and

major storms trigger multiple damage types simultaneously. The city's combination of

direct Atlantic and Intracoastal surge exposure, high-rise condo towers, aging CBS

construction with barrel tile roofs, and documented tidal flooding creates a restoration

landscape that demands specialized knowledge of each damage category, its insurance

coverage, and the correct remediation protocol.

Hallandale Beach CBS homes — many built from the 1960s through 1990s — have barrel tile roofs rated for hurricane wind loads. The tiles themselves rarely break. The failure point is the underlayment beneath: the waterproof membrane that prevents water intrusion. After 15–25 years of UV and salt-air exposure on the South Florida coast, underlayment dries out and cracks. Hurricane winds momentarily lift tiles, wind-driven rain penetrates the compromised membrane, and tiles reseat post-storm. The result is $15,000–$50,000+ in hidden interior water damage that goes undetected without a professional post-storm inspection. This is the #1 storm damage pattern in Hallandale Beach CBS single-family homes.

High

CBS Wall Wind-Driven Rain Intrusion

Hallandale Beach's dominant CBS (concrete block and stucco) construction is tested by every hurricane. Wind-driven rain at 80–130+ mph penetrates through hairline stucco cracks, mortar joint failures, and deteriorated window sealant joints. CBS walls trap moisture between the exterior stucco and interior drywall, and dry 20–40% slower than wood-frame construction. The majority of Hallandale Beach homes predate modern stucco attachment requirements. Post-storm moisture meter inspection of every exterior wall is essential — visible damage represents only a fraction of actual water intrusion.

Critical

Saltwater Storm Surge (Category 3 Contamination)

Properties in Golden Isles, Three Islands, and along the Intracoastal Waterway face direct saltwater storm surge. Under IICRC S500 standards, saltwater surge is Category 3 (grossly contaminated) water requiring complete demolition and removal of all affected porous materials. Salt crystals embedded in concrete slabs, wall framing, and subfloor systems continue absorbing atmospheric moisture indefinitely, creating perpetual dampness and accelerated corrosion of rebar, fasteners, and electrical components. This is the most destructive and expensive form of storm damage in Hallandale Beach.

High

Tidal Flooding & Intracoastal Overflow

Hallandale Beach's FEMA repetitive-loss properties and documented tidal flooding — which has increased 5–10 times since the 1960s — create a flooding baseline that compounds during hurricanes. Storm surge pushes Intracoastal water through drainage outlets and into streets, garages, and lobby levels even in neighborhoods not directly on the water. The April 2023 extreme event that dropped 22+ inches nearby demonstrated how quickly drainage systems saturate. Saltwater tidal flooding is Category 3 contamination requiring the same aggressive remediation as direct surge events.

High

High-Rise Balcony & Glazing Failure

Hallandale Beach's dense high-rise corridor introduces a storm damage pattern absent in single-family neighborhoods: upper-floor balcony door and impact glazing failure under hurricane pressure. Wind speeds increase significantly with elevation — upper floors of towers in the Diplomat Resort Area and Three Islands experience higher sustained loads than ground level. A failed balcony door or cracked impact panel creates interior pressurization that can damage ceilings, walls, and furnishings on multiple floors simultaneously. Post-storm glazing inspection is essential for every condo building.

Moderate

Window & Opening Failure (Pressurization)

Many Hallandale Beach homes, especially those built before the 2002 Florida Building Code update, still have non-impact windows or aging shutters. When a window fails — from flying debris, wind pressure, or corroded shutter tracks — the result is catastrophic interior pressurization. Wind entering through a failed opening creates uplift pressure that can lift the roof from inside. Salt-air corrosion of accordion shutter tracks and slider hardware is the most common failure point in coastal Hallandale Beach. Pre-season shutter inspection is critical.

Hurricane Restoration Process

How We Restore Hallandale Beach Homes After Hurricane Damage

Hurricane restoration in Hallandale Beach requires navigating saltwater decontamination

protocols, high-rise condo insurance layers, barrel tile roof repair, CBS wall drying,

and dual wind/flood claims simultaneously. Here is our proven six-step process from

first call through final Hallandale Beach Building Division inspection.

01

Emergency Tarping & Board-Up

Hours 1-4

We secure your Hallandale Beach home or condo against further weather exposure. Displaced barrel tiles are tarped with reinforced polyethylene rated for South Florida wind loads, failed windows are boarded, and compromised doors are sealed. Palm Build responds from our Deerfield Beach operations hub approximately 15 miles away — typically arriving within 30 to 40 minutes. Emergency tarping is covered by your insurance policy as part of your duty to mitigate further damage.

02

Damage Assessment & Water Category Testing

Days 1-3

Full documentation of all storm damage classified by cause: wind damage (tiles, siding, windows), saltwater surge from the Atlantic or Intracoastal (Category 3), tidal flooding backup (Category 2-3), and freshwater rain intrusion (Category 1-2). In Hallandale Beach, where Golden Isles faces direct surge and inland streets face tidal backup, we test flooding contamination levels on-site to determine the correct IICRC remediation protocol. We photograph every affected area, map moisture with thermal cameras, and create separate scopes for wind claims (homeowners) and flood claims (NFIP or private flood).

03

Water Extraction & Decontamination

Days 1-10

Storm damage in Hallandale Beach almost always includes water intrusion — through displaced barrel tiles, failed balcony doors, storm surge, or tidal flooding. We extract standing water, classify contamination, and begin appropriate protocols. Saltwater surge from Golden Isles or Three Islands (Category 3) requires full demolition of affected porous materials. Tidal backup flooding (Category 2-3) requires contamination testing before any materials can be dried rather than removed. Commercial dehumidifiers and air movers bring humidity below 60% to prevent mold colonization in South Florida's year-round 70–75% humidity environment.

04

Structural Drying & Mold Prevention

Days 3-14

Hallandale Beach's year-round humidity makes structural drying more demanding than most of the country. Without power (common after hurricanes), air conditioning stops and mold colonization begins within 24–48 hours. We deploy industrial desiccant dehumidifiers, establish negative air pressure containment in affected zones, and monitor moisture levels twice daily. HEPA air scrubbing removes airborne mold spores. CBS concrete block walls retain moisture longer than wood-frame construction — drying times for Hallandale Beach's dominant building type run 20–40% longer than national averages.

05

Full Structural Reconstruction

Weeks 2-16

Once the property is dried, decontaminated, and cleared, we begin reconstruction meeting current Florida Building Code requirements. Hallandale Beach is in the HVHZ (High-Velocity Hurricane Zone), requiring enhanced roof-to-wall connections, impact-rated windows and doors, and Florida Product Approval or Miami-Dade NOA for all exterior products. All permits are pulled through the City of Hallandale Beach Building Division. Barrel tile roof repair, stucco restoration, interior drywall and flooring replacement, electrical and plumbing repairs — all coordinated by a single Palm Build project manager.

06

Final Inspection & Insurance Closeout

Week 16+

City of Hallandale Beach Building Division inspections verify all structural, electrical, mechanical, and plumbing work meets current Florida Building Code (8th Edition, 2023). We perform a final walk-through with the homeowner or condo association representative and provide complete documentation for insurance closeout — including all invoices, permits, inspection records, code compliance certificates, and warranty information. For hurricane claims involving both wind and flood policies, we coordinate dual-claim closeout to maximize recovery from both carriers.

Hallandale Beach Pricing

Storm Damage Restoration Costs in Hallandale Beach

Hurricane restoration costs in Hallandale Beach are driven by barrel tile roof systems,

CBS wall drying complexity, saltwater and tidal-flood exposure, and South Florida labor

costs. High-rise condo work adds elevator protection, common-area containment, and

building access coordination. After major hurricanes, contractor demand and material

shortages across Broward County increase costs 20–40% and extend timelines by months.

Understanding what you will pay out of pocket starts with understanding your hurricane

deductible.

Hallandale Beach CBS homes range from $350,000 to $600,000 for typical single-family

construction, with Golden Isles waterfront properties reaching $1M–$2M+. High-rise

condo units vary widely by building and floor. At a 2% hurricane deductible, a

$450,000 home means $9,000 out of pocket before your wind claim pays anything. At 5%,

it is $22,500. For a $1.5M Golden Isles property at 2%, the deductible alone is

$30,000. This deductible applies to each hurricane event — not annually. If two

hurricanes hit in one season (as Frances and Jeanne did in 2004), you pay the

deductible twice. Many Hallandale Beach homeowners are stunned by this number when

they file their first hurricane claim.

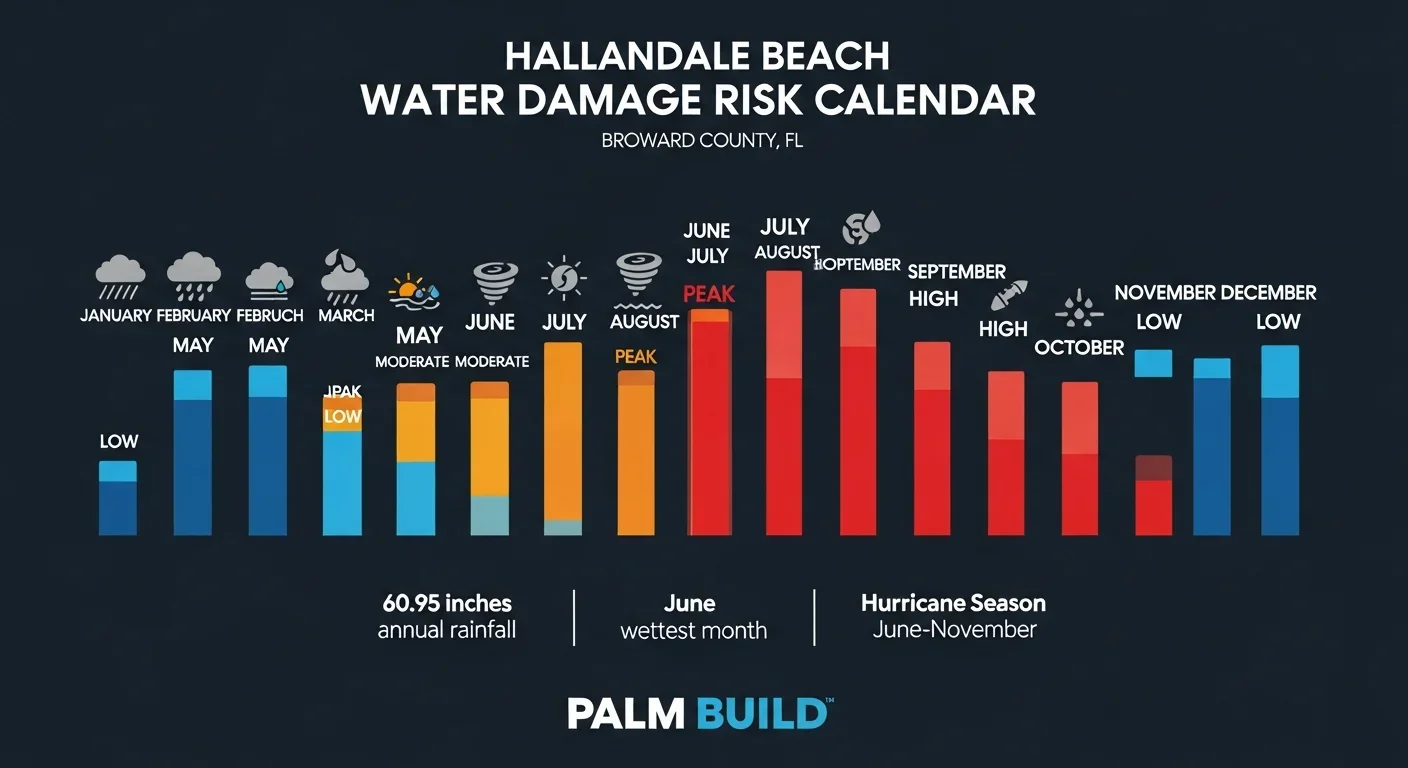

Hurricane Season Calendar

Hallandale Beach Hurricane Season: June Through November

Atlantic hurricane season runs June 1 through November 30, with peak activity

concentrated in September and October. For Hallandale Beach homeowners and condo

residents — with FEMA repetitive-loss properties, tidal flooding increasing 5–10 times

since the 1960s, and direct Atlantic and Intracoastal exposure — understanding the

seasonal risk curve determines when to complete preparations, when to stage emergency

supplies, and when to have your restoration company on speed dial.

June

Low-Moderate

Hurricane season begins June 1. Early-season storms are typically disorganized but can produce heavy rainfall and localized tidal flooding in Hallandale Beach's low-lying streets. This is your last window to complete roof inspections, verify insurance policies, and install shutter hardware before activity ramps up.

July

Moderate

Tropical development increases as Atlantic surface temperatures rise. Severe thunderstorm events become common in South Broward, capable of producing hail and damaging wind gusts. These non-hurricane events cause significant barrel tile, screen enclosure, and balcony railing damage across Hallandale Beach condos and single-family homes.

August

High

Peak development zone shifts toward South Florida. Cape Verde storms begin their Atlantic crossing. Sea surface temperatures peak, fueling rapid intensification. Preparation transitions from planning to execution — shutters should be accessible and tested, emergency supplies staged, and restoration company contact saved.

September

Peak

Statistically the most dangerous month for South Florida hurricanes. Hurricane Irma (2017) brought hurricane-force winds and storm surge to Broward County, including Hallandale Beach, as the storm tracked up the Florida Peninsula. Peak season demands full readiness: shutters installed, generator fueled, and your restoration company on speed dial.

October

Peak

October rivals September for hurricane frequency. Hurricane Wilma (2005) made Florida landfall on October 24, causing widespread damage across Broward County including Hallandale Beach. Late-season storms often approach from the southwest, catching east-coast communities off guard with unexpected surge angles from the Intracoastal corridor.

November

Low-Moderate

Season officially ends November 30 but late-season storms remain possible. Tropical cyclones have impacted South Florida in November within the historical record. Do not lower your guard until December — tidal flooding events can also intensify in late fall as sea levels are seasonally elevated.

Hallandale Beach's hurricane season spans June through November, with September and

October representing peak risk for major storm events affecting coastal South Broward

Sea Level Rise Compounds Every Season

Hallandale Beach faces documented tidal flooding that has increased 5–10 times since the

1960s. Sea level rise does not just affect surge events — it raises the baseline for

every king tide, every heavy rainfall event, and every drainage system throughout

hurricane season. Higher baseline water levels mean less drainage capacity when storms

arrive, faster street flooding, and more frequent saltwater intrusion into ground-floor

and parking-level spaces in the city's dense condo corridor.

FEMA Flood Zones in Hallandale Beach: VE, AE, and AH

Hallandale Beach contains three distinct FEMA flood zone designations, each carrying

different insurance requirements, construction standards, and restoration implications.

With FEMA-documented repetitive-loss properties and tidal flooding that has increased

5–10 times since the 1960s, the majority of Hallandale Beach properties fall within one

of these zones. Your FEMA zone determines whether flood insurance is mandatory, what

your premiums will cost, and what type of water contamination your property faces during

storm events.

The most dangerous FEMA designation. VE zones face direct wave action during storm events — not just rising water, but breaking waves that multiply structural damage force. Properties in VE zones must be elevated above Base Flood Elevation (BFE) and meet strict structural requirements. Flood insurance is mandatory for federally-backed mortgages. Storm surge in VE zones is always saltwater Category 3 contamination, requiring full demolition of all affected porous materials. Hallandale Beach's oceanfront and near-ocean properties in the Diplomat corridor fall within this designation.

Flood insurance mandatory. Highest NFIP premiums. VE construction requirements.

AE Zone — Special Flood Hazard Area

Golden Isles, Three Islands, Intracoastal-adjacent properties

AE zones face a 1% annual chance of flooding (100-year floodplain). In Hallandale Beach, AE zones follow the Intracoastal Waterway and the finger canal network throughout Golden Isles and Three Islands. Properties must be built to or above BFE. Storm surge pushes through the Intracoastal into Golden Isles canal system, while tidal flooding — which has increased 5–10 times since the 1960s — introduces saltwater into these zones even without a hurricane. Flood insurance is mandatory for federally-backed mortgages. Flooding in AE zones is typically saltwater (Category 3) from direct surge or tidal events.

Flood insurance mandatory. AE construction standards apply.

AH Zone — Shallow Flooding

Portions of central and western Hallandale Beach, low-lying interior areas

AH zones face shallow flooding (typically 1–3 feet) during extreme rainfall events or when drainage systems are overwhelmed. In Hallandale Beach, AH zones cover interior areas where infrastructure has limited capacity relative to South Florida rainfall intensity. The April 2023 extreme event that dropped over 22 inches nearby demonstrated how quickly interior neighborhoods can flood. Flood insurance may not be required by mortgage but is strongly recommended — FEMA has documented repetitive-loss properties in Hallandale Beach, and today's AH zone may qualify for reduced NFIP Preferred Risk rates.

Flood insurance recommended even if not required. Shallow flooding adds up fast.

X Zone: Not in a Flood Zone Does Not Mean Flood-Safe

Properties in FEMA Zone X (minimal flood hazard) are not required to carry flood

insurance. But with FEMA repetitive-loss properties documented in Hallandale Beach, tidal

flooding increasing 5–10 times since the 1960s, and sea level rise compressing storm-drain

capacity every year, even X-zone properties face real flood risk. Over 25% of NFIP flood

insurance claims nationally come from properties outside Special Flood Hazard Areas.

Today's X-zone property may be tomorrow's AE zone. Flood insurance for X-zone properties

is available at reduced Preferred Risk rates through the NFIP — a fraction of the cost of

uninsured flood damage.

Critical Insurance Distinction

Wind vs. Flood Insurance: Hallandale Beach's Most Expensive Misunderstanding

This is the single most important insurance concept for Hallandale Beach storm damage.

Wind damage and flood damage from the same hurricane are covered by different policies,

carry different deductibles, and are filed as separate claims. In a city where Golden

Isles faces direct Intracoastal surge, tidal flooding has increased 5–10 times since the

1960s, and high-rise condos sit on both flood and wind exposure simultaneously, most

hurricane events produce both wind and flood damage — making proper damage

classification the difference between full recovery and financial catastrophe.

Barrel tile displacement from wind uplift and flying debris

Balcony door, window, shutter, and impact-glazing damage from wind pressure

Rain water entering through wind-created openings in roofs or walls

Stucco and CBS structural damage from wind load or debris impact

Emergency tarping and board-up costs (duty to mitigate)

ALE (Additional Living Expenses) if home or unit is uninhabitable

FL Hurricane Deductible: 2–5% of insured value. On a $450K Hallandale Beach

home = $9,000–$22,500 out of pocket before coverage begins.

Flood Damage (Separate NFIP or Private Flood Policy)

Storm surge from the Atlantic Ocean or Intracoastal Waterway (Category 3 saltwater)

Tidal flooding backup through storm drains and drainage infrastructure

Groundwater intrusion through slab or foundation

Sewer backup from overwhelmed municipal systems during hurricanes

NFIP max dwelling coverage: $250,000 (may be insufficient for Golden Isles properties)

NOT covered by standard homeowners — requires separate flood policy

NFIP 60-Day Rule: Proof of loss must be filed within 60 days of the flood

event. Missing this deadline can void your entire flood claim.

Claim Deadline Alert: File Both Claims Simultaneously

After a hurricane in Hallandale Beach, you may need to file two separate claims: wind

damage to your homeowners carrier and flood damage to your NFIP or private flood

carrier. Each has different deadlines, deductibles, and adjusters. The NFIP 60-day

proof of loss deadline is the most critical — miss it and your entire flood claim can

be denied. Palm Build documents all damage by cause from day one, creating separate

wind and flood scopes that align with each policy's requirements. For condo owners, we

also separate damage covered by the association master policy from damage falling

under your individual HO-6. This multi-policy documentation approach recovers

significantly more than generic damage reports that do not distinguish coverage

sources.

What Hurricane Damage Looks Like in Hallandale Beach

Golden Isles' finger canal system and Intracoastal exposure make it Hallandale Beach's most storm-vulnerable neighborhood — surge enters from multiple directions simultaneously

Barrel tile displacement exposes aging underlayment beneath — the #1 hidden storm damage pattern in Hallandale Beach CBS construction after every hurricane season

Post-storm tidal flooding overwhelms Hallandale Beach drainage — sea-level rise has increased tidal flooding frequency 5–10 times since the 1960s

Tidal flooding regularly reaches Hallandale Beach streets even without a storm — when hurricanes arrive, this baseline makes drainage capacity critical

The Palm Build Difference

Why Hallandale Beach Homeowners Choose Palm Build After Hurricanes

Deerfield Beach Hub — 30-40 Minute Response to Hallandale Beach

Palm Build's South Florida Operations Hub is located at 786 S Military Trail, Deerfield Beach, FL 33442 — approximately 15 miles from Hallandale Beach. We dispatch emergency crews 24/7 and reach most Hallandale Beach neighborhoods in 30 to 40 minutes. During major hurricane events, we activate catastrophe response with pre-positioned crews and equipment staged closer to South Broward. Pre-storm clients receive priority dispatch ahead of the general queue.

Every crew lead holds current IICRC Water Restoration Technician and Fire/Smoke Restoration Technician certifications. Our South Florida teams are additionally trained in Category 3 saltwater decontamination and tidal-flooding protocols — critical in Hallandale Beach, where Golden Isles faces direct Intracoastal surge and the entire coastal corridor sees tidal flooding events that have increased 5–10 times since the 1960s. We test contamination levels on-site before choosing the remediation protocol.

Dual-Claim Documentation (Wind + Flood + HOA Master)

Our damage assessment classifies every item by cause — wind vs. surge vs. tidal flooding vs. debris impact — ensuring each claim is filed with the correct policy. In Hallandale Beach, where wind damage goes through homeowners (with 2–5% hurricane deductible), flood damage requires separate NFIP or private flood claims, and condo associations have master policies that cover specific elements, this multi-policy documentation approach recovers significantly more than generic damage reports.

Barrel Tile & CBS Construction Expertise

Hallandale Beach's dominant building type — CBS concrete block with barrel tile roofing — requires specialized storm restoration knowledge. We understand underlayment failure patterns beneath barrel tiles, moisture dynamics inside CBS walls (which dry 20–40% slower than wood-frame), and stucco crack assessment to find hidden water intrusion. Our crews have restored hundreds of CBS homes and condo units across Broward County.

Florida Insurance Navigation + Condo HOA Expertise

We understand Florida's complex insurance landscape: Citizens depopulation, hurricane deductible percentages, NFIP proof-of-loss deadlines, SB 2-A AOB reform, and the critical distinction between unit-owner HO-6 and association master-policy coverage. Palm Build coordinates with your carrier, your adjuster, HOA property management, and if needed your public adjuster to maximize claim recovery while keeping restoration moving.

Full Reconstruction — Emergency Through HVHZ Final Punch

From emergency tarping through HVHZ-compliant final reconstruction, one company handles everything. We pull permits through the City of Hallandale Beach Building Division, supply Florida Product Approval materials, and coordinate all inspections. Tile roof repair, stucco restoration, impact window and door replacement, and full interior rebuild — all managed by a single project manager with deep Broward County permit expertise. High-rise condo coordination — elevator protection, floor-by-floor containment — is part of our standard scope.

Common Questions

Hallandale Beach Hurricane Damage FAQ

How quickly can Palm Build respond after a hurricane in Hallandale Beach?

Palm Build's South Florida Operations Hub is located in Deerfield Beach, approximately 15 miles from Hallandale Beach — roughly 30 to 40 minutes under normal traffic conditions. After major hurricane events, we activate catastrophe response protocols with pre-positioned crews and equipment staged closer to South Broward. Pre-storm clients receive priority dispatch. We operate 24/7/365, including during hurricane season.

What hurricane evacuation zones affect Hallandale Beach?

Hallandale Beach follows Broward County evacuation zones. Zone A covers properties east of the Intracoastal Waterway — including Golden Isles waterfront homes and oceanfront residences — which evacuate for any hurricane. Zone B covers properties east of US-1 (Federal Highway), including portions of Three Islands, which evacuate for Category 3+ storms. Properties west of Federal Highway are not in a mandatory evacuation zone but still face wind damage, tidal-flood intrusion, and overwhelmed drainage during major events.

Does my homeowners insurance cover hurricane damage in Hallandale Beach?

Wind damage is covered under your Florida homeowners policy, but with a separate hurricane deductible of 2–5% of insured value. On a Hallandale Beach condo or CBS home valued at $400,000, that means $8,000–$20,000 out of pocket before wind coverage begins. Flood damage from storm surge, Intracoastal overflow, or tidal flooding requires a separate NFIP or private flood policy — standard homeowners policies exclude flood entirely. After a hurricane, you often need to file two separate claims with different carriers.

What makes Hallandale Beach high-rise condos especially vulnerable to hurricane damage?

High-rise condos in Hallandale Beach face compounded risk: upper floors experience higher wind speeds, balcony doors and sliding glass doors are common failure points under hurricane pressure, and a single failed opening can pressurize interior common areas or individual units. Storm surge reaching lower parking levels or lobby entries introduces Category 3 saltwater — the most destructive water type under IICRC standards — requiring full demolition of all affected porous materials. HOA master-policy coordination and individual unit HO-6 claim separation add insurance complexity unique to condo buildings.

What is the difference between saltwater storm surge and tidal flooding in Hallandale Beach?

Both carry saltwater, but the mechanism differs. Storm surge is wind-driven: a hurricane pushes a wall of Atlantic Ocean or Intracoastal water onto land, inundating Golden Isles waterfront homes and ground-level condo units with Category 3 contaminated water. Tidal flooding happens even during clear weather: sea-level rise now causes high tides to push water up through storm drains onto streets and into ground-floor spaces 5–10 times more often than in the 1960s. Both introduce saltwater, but surge events are higher-volume and require more extensive demolition and decontamination.

Why are barrel tile roofs vulnerable to storm damage in Hallandale Beach?

Hallandale Beach's CBS homes — many built in the 1960s through 1990s — commonly have barrel tile roofs rated for hurricane wind loads. The tiles themselves rarely break. The failure point is the underlayment beneath: the waterproof membrane that actually prevents water intrusion. After 15–25 years of UV and salt-air exposure, underlayment deteriorates. Hurricane winds momentarily lift tiles, rain penetrates the compromised membrane, and tiles reseat post-storm. This creates $15,000–$50,000+ in hidden interior water damage that goes undetected without a professional post-storm inspection.

Does the HVHZ (High-Velocity Hurricane Zone) requirement apply to Hallandale Beach?

Yes. All of Broward County — including Hallandale Beach — is within the High-Velocity Hurricane Zone. This means design wind speeds of approximately 170 mph, mandatory large- and small-missile impact testing (TAS 201/202/203) for exterior products, and Florida Product Approval or Miami-Dade NOA required for all windows, doors, and roofing materials. Any reconstruction must be permitted through the City of Hallandale Beach Building Division and comply with Florida Building Code 8th Edition (2023). Palm Build's reconstruction scopes meet all HVHZ requirements.

How long does hurricane damage restoration take in Hallandale Beach?

Emergency tarping and water extraction: 1–2 days. Saltwater decontamination and structural drying: 5–10 days (longer for Category 3 protocols in high-rise condos). Barrel tile roof repair: 3–8 weeks depending on material availability and Hallandale Beach Building Division permit processing. Full reconstruction: 8–20 weeks. After major hurricanes, timelines extend due to contractor demand, material shortages, and permitting backlogs across Broward County.

Trusted Vendors

Trusted local pros in Hallandale Beach

Outside our restoration scope, these are the vetted, licensed contractors we trust

alongside our work. Personally evaluated, reference-checked, and recommended by Palm

Build.

Hurricane Damage in Hallandale Beach? We Respond 24/7.

Palm Build dispatches from our Deerfield Beach hub — approximately 15 miles away — to every Hallandale Beach neighborhood. With FEMA repetitive-loss properties, tidal flooding increasing 5–10× since the 1960s, and high-rise condos facing storm surge from the Atlantic and Intracoastal simultaneously, storm damage spreads fast. Our crew provides emergency tarping, saltwater extraction, and full HVHZ-compliant reconstruction with insurance documentation from the first call.