Insurance Restoration Process in Coconut Creek, Florida

Coconut Creek homeowners face Broward County's punishing insurance market — average premiums of $5,164-$6,112, a strict 1-year filing deadline under Fla. Stat. 627.70132, AOB completely prohibited since January 2023, hurricane deductibles running 2-5% of dwelling value, and flood damage excluded from standard HO-3 policies. With 72% multi-unit housing, most claims also involve navigating the dual-policy maze of HOA master policies and individual HO-6 coverage. Palm Build handles the entire insurance restoration process from our Deerfield Beach office — just 5 miles away — delivering documentation, adjuster coordination, supplement negotiation, condo-specific claim separation, and Florida-specific deadline compliance.

5 miles — Coconut Creek, FL 15-25 min Response IICRC Certified

Why Insurance Claims in Coconut Creek Demand Expert Navigation

Coconut Creek sits in the heart of Broward County's punishing insurance market. Between

carrier volatility, the shortest filing deadlines in the nation, premiums exceeding

$5,164 annually, and the dual-policy complexity of condo living where mold can begin growing in 24-48 hours, filing a restoration claim without expert documentation means leaving money on the

table — or getting denied entirely.

Florida's property insurance market has seen more than a dozen carrier insolvencies since 2020. In Broward County, private carriers have exited or reduced their books, pushing homeowners toward Citizens Property Insurance — the state-backed insurer of last resort now holding 687,000+ policies statewide. Coverage restrictions have tightened: cosmetic hail damage exclusions, mandatory hurricane deductibles, and shrinking mold sublimits are now standard. Premium spikes of 25-40% per renewal cycle have become the norm.

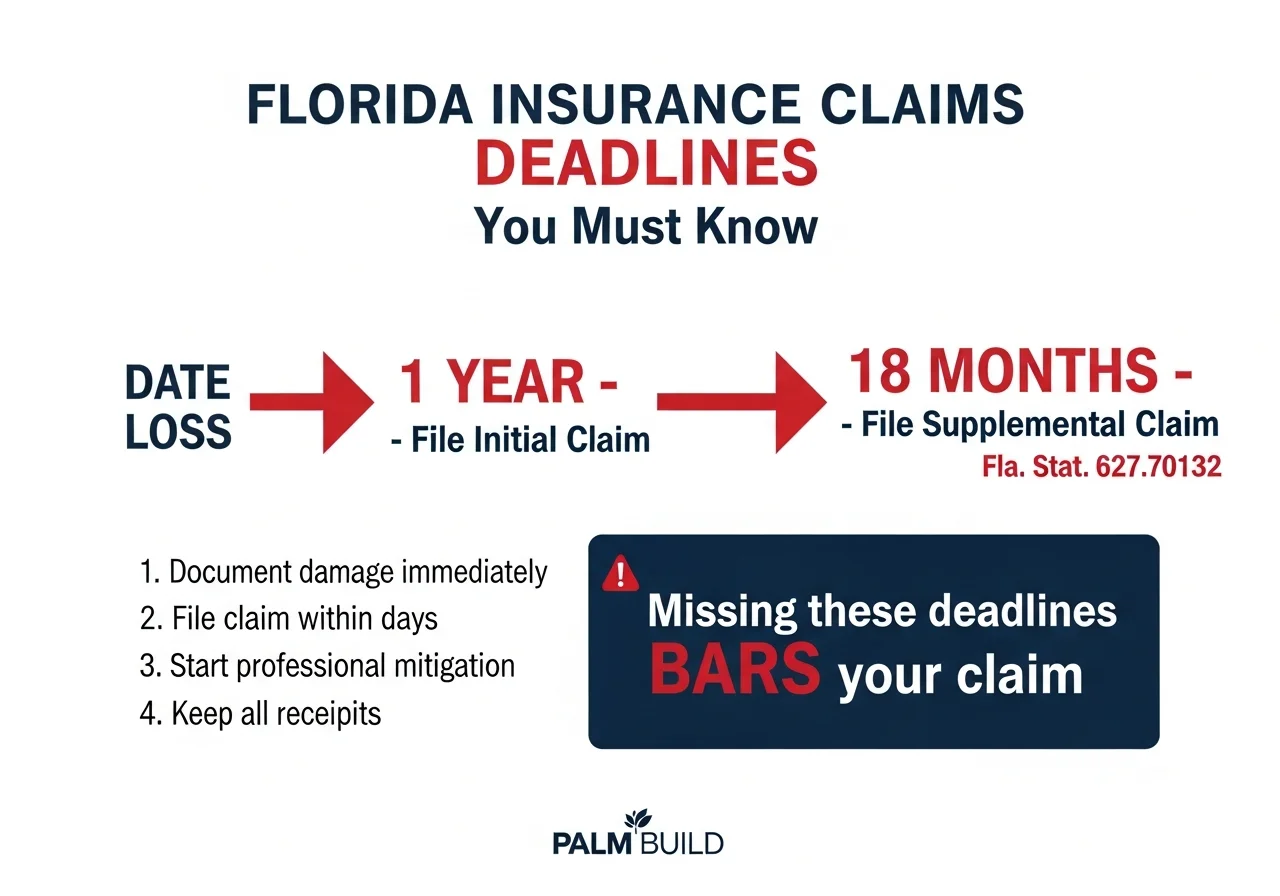

Florida compressed its claim filing deadline from two years to one year under Fla. Stat. 627.70132 (Senate Bill 2A). Supplemental claims for hidden damage discovered during restoration must be filed within 18 months of the original date of loss — not the date of discovery. For hurricane events, the clock starts from the NOAA verification date. Missing either deadline results in automatic claim denial regardless of damage severity or legitimacy.

High Premiums: Broward County Among Highest in FL

$5,164+

Avg annual premium

Coconut Creek homeowners pay $5,164-$6,112 annually in homeowners insurance premiums — among the highest in Florida and roughly three times the national average. Hurricane deductibles run 2-5% of dwelling value, meaning a $400,000 home carries an $8,000-$20,000 wind deductible before coverage begins. With premiums this high, every claim must be documented to maximize the return on what you are already paying.

Condo Complexity: Master Policy vs. HO-6 Coordination

72%

Multi-unit housing

With 72% of Coconut Creek housing stock in multi-unit buildings — Wynmoor (9,000+ units), The Township, Centura Parc, Hammocks, Coco Palms — most damage events trigger two separate insurance policies simultaneously. The HOA master policy covers building shell and common elements while individual HO-6 policies cover interior finishes. Shared claim coordination between carriers is the most common failure point in Coconut Creek claims.

Palm Build's claims consultation includes a complete review of your policy coverage,

deductible structure, and documentation requirements specific to your Broward County

carrier.

Flood Insurance Education

Flood Insurance in Coconut Creek: What Your HO-3 Does Not Cover

This is the single most dangerous coverage gap in Coconut Creek. If you do not carry

separate flood insurance, a canal overflow or overwhelmed storm drain can create

thousands in damage with zero coverage — regardless of how much you pay in homeowners

premiums.

Your HO-3 Does NOT Cover Flood

100%

Flood excluded from HO-3

Standard HO-3 homeowners policies do not cover flood damage from rising water — including overwhelmed storm drains, canal backup from the C-14 system, and storm surge during hurricanes. This is the single most dangerous coverage gap in Coconut Creek. Your HO-3 covers sudden water damage from burst pipes, appliance failures, and rain entering through storm-damaged roofing. Rising water requires a separate policy.

1 in 3 Flood Claims: Outside High-Risk Zones

50.7 in

Annual rainfall

Nationally, one in three NFIP flood claims comes from properties outside designated high-risk flood zones. Many Coconut Creek homeowners in Flood Zone X assume flood risk is negligible and decline separate flood coverage. During heavy rain events, the C-14 canal system and retention lakes can back up — flooding homes that have never flooded before. Coconut Creek averages 50.7 inches of annual rainfall.

Wind-Driven Rain vs. Rising Water

Dual

Peril classification required

During hurricanes, two perils frequently coexist in the same Coconut Creek home: wind-driven rain entering through damaged roofing (covered by homeowners under wind peril) and rising water from canal overflow or overwhelmed drainage (covered only by separate flood policy). Water staining at the ceiling suggests wind-driven rain entry. Water marks climbing walls from the floor suggest rising water. Both can be present simultaneously.

NFIP & Private Flood Insurance Quick Reference

NFIP Building Coverage Max

Residential

$250,000

NFIP Contents Coverage Max

Residential

$100,000

Waiting Period (NFIP)

Before coverage takes effect

30 Days

Private Flood Waiting Period

Varies by carrier

10-15 Days

Proof of Loss Deadline (NFIP)

After loss event — strict enforcement

60 Days

Palm Build Classifies Every Item by Cause

Our moisture mapping and thermal imaging show both the point of entry (roof

penetration vs. ground-level intrusion) and the direction of moisture migration. This

classification ensures the right policy covers the right damage — and prevents your

homeowners carrier from denying wind-rain damage by calling it flood.

Coconut Creek retention lakes and the C-14 canal system can overflow during sustained

heavy rainfall — flood damage from rising water is NOT covered by standard homeowners

insurance.

Florida Insurance Deadlines

Claims Deadline Timeline for Coconut Creek Homeowners

Florida's restructured insurance deadlines create a rigid timeline that every Coconut

Creek homeowner must understand. Missing any deadline results in automatic claim denial

— regardless of how legitimate the damage is.

What You Heard a Few Years Ago May Be Wrong

Before the 2022 reform, Florida property owners had 3 years to file wind-related claims and 2 years for other perils. Those windows were reduced to 1 year for all claims effective for policies issued or renewed after January 1, 2023. If your damage occurred

after your policy renewed in 2023 or later, the shortened deadlines apply. Do not rely on

outdated advice from neighbors or online forums — verify your specific deadline with your

carrier immediately.

1-Year Initial Filing Deadline

Fla. Stat. 627.70132

CRITICAL

You must report property damage to your insurer within 1 year of the date of loss. This deadline was reduced from 2 years by Senate Bill 2A. If you discover damage 13 months after a hurricane, your claim is barred — regardless of how legitimate the damage is. For Coconut Creek homes where moisture damage develops slowly behind CBS stucco walls, this shortened deadline makes immediate reporting essential.

12 months from date of loss

18-Month Supplemental Deadline

Fla. Stat. 627.70132

CRITICAL

When hidden damage is discovered during restoration — moisture behind walls, mold in concealed cavities, structural issues under finished surfaces — a supplemental claim must be filed within 18 months of the original date of loss. Not 18 months from discovery. If a hurricane hit 16 months ago and your contractor just found concealed damage, you have only 2 months to file the supplement.

18 months from original date of loss

AOB Prohibition (Complete Ban)

HB 7065 (Jan 2023)

CRITICAL

Assignment of Benefits (AOB) is completely prohibited for all property insurance policies issued or renewed after January 1, 2023. No restoration company can take over your insurance benefits. You remain the policyholder, you authorize all work, and your carrier pays you directly. Any contractor asking you to sign an AOB is operating outside the law. Palm Build has never used AOB — we work for homeowners, not insurance assignments.

Effective for all policies issued/renewed after Jan 1, 2023

Hurricane Date of Loss Rule

NOAA Verification

For hurricane losses, the 'date of loss' is NOT when you personally discover the damage — it's the NOAA verification date for the hurricane event. Your 1-year filing deadline starts from the date NOAA confirms the hurricane, which may be before you even return to your Coconut Creek home to assess damage. Check your policy and NOAA records to confirm your specific deadline.

NOAA verification date = start of deadline clock

14-Day Investigation / 60-Day Determination

Fla. Stat. 627.70131

Once you file a claim, your insurer must begin investigation within 14 days and provide a coverage determination (approve, deny, or partially approve) within 60 days. Undisputed portions must be paid within 90 days. If your carrier misses these deadlines, they are in violation of Florida statute. Document every communication date with your carrier.

14 days to investigate, 60 days to determine, 90 days to pay

Reopened Claim Deadline

Fla. Stat. 627.70132

If a previously closed claim needs to be reopened due to new damage or additional issues related to the original loss, you must reopen it within 1 year of the original date of loss. This applies when restoration reveals problems that were not apparent during the original claim — common in Coconut Creek CBS homes where water intrusion patterns evolve behind stucco.

1 year to reopen a closed claim

Florida's compressed claim deadlines leave no room for delay. Palm Build calendars every

deadline from the moment you call.

Palm Build tracks every deadline for you. From the moment we take your call, we calendar your 1-year filing deadline, 18-month supplemental

deadline, carrier investigation timelines, and any reopened claim windows. You will never miss

a Florida deadline because we build compliance into our process from day one.

Coconut Creek Claims Process

Step-by-Step Insurance Claims Process for Coconut Creek Homeowners

Filing a successful restoration claim in Coconut Creek requires methodical execution

across a defined sequence. Each step builds on the previous one — skipping or rushing

any step creates gaps that carriers exploit to reduce or deny payment.

01

Document Everything

Before Any Cleanup

02

File Claim Immediately

Day of Loss

03

Emergency Mitigation

Hours 1-6

04

Adjuster Coordination

Days 1-14

05

Supplement if Needed

18-Month Window

06

Restoration & Close-Out

1-6 Weeks

01

Document Everything

Before Any Cleanup

Palm Build arrives within 15-25 minutes from our Deerfield Beach office. Before any cleanup begins, we photograph every inch of damage with high-resolution photography, video walkthrough, and initial moisture readings. This pre-mitigation documentation is the single most important evidence in your claim — it establishes damage scope before intervention and prevents carriers from arguing mitigation was unnecessary or damage was pre-existing.

02

File Claim Immediately

Day of Loss

Do not wait. Florida's 1-year filing deadline under Fla. Stat. 627.70132 starts at the date of loss — not when you decide to file. For hurricane events, the clock starts from the NOAA verification date. Report the loss to your carrier the same day, even before you have a damage estimate. Palm Build provides initial documentation within hours of arrival to support your filing.

03

Emergency Mitigation

Hours 1-6

Your policy requires you to mitigate further damage — it is a contractual duty. Failure to mitigate can reduce or void your claim. Palm Build begins emergency water extraction, board-up, or tarping immediately after pre-mitigation documentation is complete. Every mitigation action is documented with timestamped photos showing the necessity of each step.

04

Adjuster Coordination

Days 1-14

We schedule and attend the on-site adjuster inspection at your Coconut Creek property. Our project manager walks the adjuster through moisture maps, thermal images, and damage scope documentation. Adjusters processing 8-12 inspections daily during catastrophe events miss items without an on-site guide. We ensure every damaged area is included in their scope.

05

Supplement if Needed

18-Month Window

Hidden damage found during demolition — mold behind drywall, saturated subfloor beneath tile, moisture in CBS block cores — requires supplemental claim filing. Under Florida law, supplements must be filed within 18 months of the original date of loss. Palm Build files supplements with supporting moisture maps, thermal images, and before-and-after photography proving damage was concealed during initial inspection.

06

Restoration & Close-Out

1-6 Weeks

We document each restoration phase and provide completion documentation to your carrier. This final package — showing the property restored to pre-loss condition — triggers the final payment release. For mortgage-held properties, this documentation satisfies your lender's loss draft department. For Coconut Creek condos, we provide separate close-out packages for master policy and HO-6 carriers.

Why Our Coconut Creek Claims Process Works

1

Pre-Mitigation Documentation

We photograph and moisture-map everything before any cleanup begins — the most critical evidence in any Florida claim

2

Xactimate-Native Estimates

Our estimates use the same software and localized Coconut Creek pricing your adjuster uses — no format conversion delays

3

Deadline Compliance

We calendar every Florida deadline from day one — 1-year filing, 18-month supplement, carrier response windows

4

Dual-Policy Condo Documentation

Separate documentation packages for master policy and HO-6 carriers — preventing finger-pointing denials

What Palm Build Documents for Every Coconut Creek Insurance Claim

Under Florida's post-AOB framework, the quality of your contractor's documentation

directly determines your claim outcome. Palm Build provides six categories of

insurance-grade documentation on every Coconut Creek project — formatted for every

carrier active in Broward County.

Moisture Mapping Reports

Pin-type penetrating and non-invasive capacitance meters create a comprehensive grid map of moisture levels across every affected surface — walls at base, mid-wall, and ceiling level; floors; and cabinetry. In Coconut Creek's CBS stucco homes, moisture routinely wicks into concrete block cores — damage that surface-level visual inspections completely miss. These maps show adjusters exactly where damage exists.

Proves the full extent of moisture intrusion to adjusters

Daily Drying Logs

Psychrometric readings — temperature, relative humidity, grain depression, dew point — recorded daily at each equipment placement location. These logs prove that professional dehumidifiers and air movers were necessary, properly deployed, and operated for the documented duration. In Coconut Creek's 70%+ ambient humidity, extended drying protocols are required compared to arid climates.

Justifies 3-5 day drying protocols in South Florida humidity

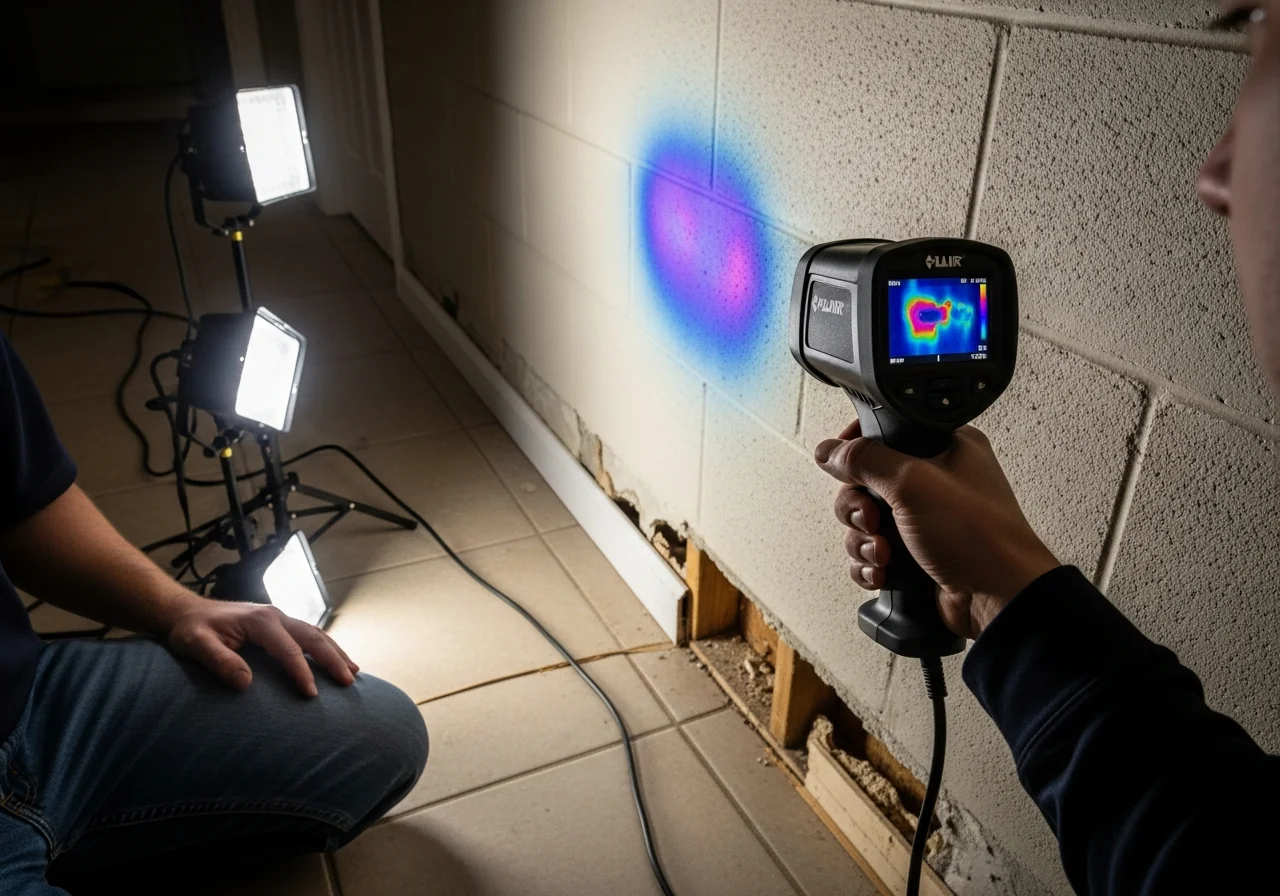

Thermal Imaging Scans

FLIR infrared cameras reveal moisture hidden behind CBS block walls, under tile flooring, and inside ceiling assemblies — damage invisible to the naked eye. In Coconut Creek's concrete block construction, thermal imaging is the only non-destructive way to map moisture migration through the porous block core. These images provide irrefutable evidence of concealed damage extent.

Identifies 30-50% more damage than visual inspection alone

Photo & Video Documentation

High-resolution, time-stamped photography and video walkthrough documenting all damage before any cleanup or mitigation work begins. Wide-angle room shots, close-up damage details, affected material identification, and equipment placement are captured. For Coconut Creek condos, we photograph the damage path across units and common areas to support multi-policy claims.

Establishes baseline damage scope before intervention

Xactimate Scope Documentation

Line-item estimates prepared in Xactimate using localized Coconut Creek pricing from the same database your adjuster uses. Every damaged item is individually priced using current Broward County labor and material rates. Code upgrade costs (impact windows, roof tie-downs, electrical upgrades) are itemized separately to trigger Ordinance or Law coverage.

Same software carriers use — eliminates format disputes

Third-Party Testing Results

When required, Palm Build coordinates independent third-party testing — mold air quality sampling, asbestos testing in pre-1980s materials, lead paint assessment, and water quality analysis. Third-party lab reports carry more weight with adjusters than contractor assessments and are required by some carriers for mold claims exceeding sublimits.

Thermal imaging reveals hidden moisture behind CBS block walls in Coconut Creek homes —

this documentation proves the full extent of damage to your insurance carrier's

adjuster.

Coverage Gaps & Exclusions

Common Coverage Gaps in Coconut Creek Homeowners Policies

Even with Broward County premiums exceeding $5,164 annually, most policies have

significant gaps that leave Coconut Creek homeowners exposed. Understanding what your

policy does NOT cover before you file a claim saves thousands in out-of-pocket costs.

Flood Damage NOT in Standard HO-3/HO-6

EXCLUDED

Standard homeowners policies do NOT cover flood damage from rising water — period. This is a critical distinction in Coconut Creek, where annual rainfall averages 50.7 inches, wet-season downpours overwhelm aging drainage infrastructure, and the C-14 canal system can back up during sustained rainfall events. One in three NFIP flood claims nationally comes from outside designated high-risk flood zones. If your home is in Flood Zone X and you skipped flood insurance, a canal overflow creates damage with zero coverage.

How Palm Build helps: Purchase NFIP or private flood insurance regardless of flood zone designation. Palm Build classifies every item of damage by cause and entry point — ensuring the right policy pays for the right damage.

Mold Sublimits ($10K-$50K Typical)

LIMITED

Most Florida homeowners policies cap mold remediation at $10,000-$50,000. Actual mold remediation in Coconut Creek's year-round 70-75% humidity routinely costs $20,000-$75,000+. Mold resulting directly from a covered sudden water event may bypass the sublimit with proper documentation establishing a causal chain — but mold from long-term humidity, HVAC condensation, or gradual moisture is excluded entirely.

How Palm Build helps: Palm Build's rapid 15-25 minute response minimizes mold colonization risk. Our documentation ties any mold growth directly to the covered loss event with photographic and scientific evidence to support bypassing the sublimit.

Windstorm Deductibles (2-5% of Dwelling Value)

LIMITED

Unlike your standard $1,000-$2,500 flat deductible, hurricane and windstorm deductibles in Broward County are percentage-based — typically 2-5% of your dwelling coverage amount. On a $400,000 Coconut Creek home, a 2% wind deductible means $8,000 out of pocket before coverage begins. A 5% deductible means $20,000. This deductible applies only to named storms and wind events; other perils use your standard flat deductible.

How Palm Build helps: Understand your specific hurricane deductible dollar amount before storm season. Buydown endorsements are available from some carriers to reduce the percentage. Consider a lower percentage if financially feasible.

Ordinance & Law Coverage for Code Upgrades

LIMITED

Florida Building Code requirements have evolved significantly since most Coconut Creek homes were built (1970s-1990s). When restoring damage, you may be required to bring affected areas up to current code — hurricane impact windows, updated electrical, enhanced roof-to-wall connections. Standard HO-3 policies provide only 25% of dwelling coverage for Ordinance or Law. For older Coconut Creek homes requiring significant HVHZ code upgrades, this may not be sufficient.

How Palm Build helps: Verify your Ordinance or Law coverage percentage and consider increasing if your home predates 1994 building code changes. Palm Build itemizes code upgrade costs separately in Xactimate to trigger this coverage.

ALE (Additional Living Expenses) for Displacement

LIMITED

If damage makes your Coconut Creek home uninhabitable, your policy's Coverage D (Additional Living Expenses) pays for temporary housing. But Coverage D limits vary widely — some carriers cap at 12 months, others at a specific dollar amount. Extended restoration timelines common for condo claims requiring HOA coordination can exhaust Coverage D before your home is repaired.

How Palm Build helps: Know your ALE limit and communicate displacement needs early with your carrier. Palm Build provides estimated restoration timelines to support requests for adequate temporary housing coverage.

Sewer Backup Exclusion

EXCLUDED

Sewer and drain backup is excluded from standard policies unless a specific endorsement is purchased. In older Coconut Creek communities like Emerald Lake Park (1969) and Hammocks (1980) with aging cast iron and clay drain lines, sewer backup is a legitimate risk. The endorsement typically costs $50-$100/year for $10,000-$25,000 coverage.

How Palm Build helps: Add the sewer/drain backup endorsement at your next renewal — inexpensive coverage for a common older-home risk in Coconut Creek.

Condo Insurance Guide

Condo Insurance Claims Guide for Coconut Creek

With 72% of Coconut Creek housing in multi-unit buildings, most insurance claims involve

the complex interplay between HOA master policies and unit-owner HO-6 policies.

Misunderstanding who pays for what can leave thousands in reconstruction costs unfunded.

Here's what every Coconut Creek condo owner needs to know.

Master Policy vs. HO-6: Who Pays for What?

"Bare walls" master policies (common in Wynmoor, The Township) cover only the building shell — exterior walls, roof, common areas, and shared plumbing risers. Everything inside your unit walls is YOUR HO-6 responsibility: drywall, flooring, cabinets, fixtures, appliances, and personal property.

"All-in" master policies cover the building shell PLUS original unit finishes (as built). Your HO-6 covers upgrades, improvements, and personal property. The critical question is what constitutes "original" in a 1980s community where many units have been renovated.

When water originates from a neighbor's unit (common in Coconut Creek's dense condo stock), the source unit's HO-6 liability coverage and your HO-6 dwelling coverage must coordinate — Palm Build documents the origin point and damage path for both carriers.

Loss assessment coverage on your HO-6 protects you if the HOA levies a special assessment for a large common-area claim that exceeds the master policy deductible.

Post-AOB Reform (HB 7065, January 2023)

Florida eliminated Assignment of Benefits (AOB) on policies issued or renewed after January 1, 2023. Previously, condo owners could assign their insurance benefits directly to restoration companies who would bill carriers and pursue litigation if underpaid.

Under the new law, condo owners must navigate claims personally — file the claim, receive payments, and pay contractors directly. This is a significant change for Coconut Creek's large 55+ community population.

However, owners CAN still authorize contractors as their representatives for documentation, adjuster meetings, scope preparation, and estimate review. This authorization does NOT constitute an AOB.

Palm Build handles all Xactimate documentation, meets adjusters on-site, and prepares supplement requests — you stay in control of your claim while we provide the technical expertise your carrier requires.

Coordinating Between Master & HO-6 Policies

In multi-policy claims (common for fire, major water events, and hurricane damage), Palm Build prepares separate Xactimate scopes for master policy and HO-6 elements — clearly delineating who pays for what.

Master policy deductibles can be substantial ($10,000-$50,000+) and are often passed through to unit owners as special assessments — your HO-6 loss assessment coverage applies here.

When the HOA's master policy carrier and your HO-6 carrier disagree on responsibility, having professional documentation that clearly identifies the damage origin and affected elements prevents coverage gaps.

Palm Build communicates directly with both carriers and the HOA property management company to ensure nothing falls between policies.

Live in a Coconut Creek condo? Call (754) 600-3369 — we understand the master policy vs. HO-6 coordination your claim requires and work with

property management companies daily.

Coconut Creek Insurance Claim Documentation Gallery

Professional documentation is the difference between a denied claim and a fully covered

restoration. These Coconut Creek projects demonstrate how Palm Build's documentation

approach changes claim outcomes.

DAMAGE

DOCUMENTED & RESTORED

CBS Stucco Water Intrusion — Regency Lakes

Moisture behind CBS stucco was invisible until paint began bubbling months after a heavy rain event. Thermal imaging revealed water wicking through the block core extending 14 feet beyond the visible staining. The carrier initially approved only the visible 3-foot section — our moisture mapping documentation secured full-scope coverage for the entire affected wall system.

Supplement approved for concealed CBS block core damage — full restoration covered

DAMAGE

DOCUMENTED & RESTORED

Multi-Unit Water Migration — Wynmoor

A polybutylene pipe failure in an upstairs unit at Wynmoor sent water through three units across two floors. The master policy carrier and two separate HO-6 carriers each initially denied portions of the claim, pointing at the other policies. Our dual-documentation approach — separate Xactimate scopes for each policy with damage mapped by responsibility zone — resolved all three claims.

Triple-policy coordination — all three carriers paid their respective scope

DAMAGE

DOCUMENTED & RESTORED

HVAC Condensate Overflow — Centura Parc

An HVAC condensate line clog caused water to overflow through the air handler, damaging ceiling, walls, and flooring. The carrier initially classified it as a maintenance failure and denied the claim. Our documentation of the specific mechanical component failure — a cracked condensate pan, not a clogged drain line — reclassified it as a covered sudden event under the HO-3 policy.

Reclassified from maintenance denial to covered sudden event — full claim paid

The Local Advantage

Why Coconut Creek Homeowners Choose Palm Build for Insurance Claims

The insurance restoration process in Florida is more complex than in any other state.

Between AOB reform, compressed deadlines, volatile carrier markets, and the dual-policy

reality of condo living, Coconut Creek homeowners need a restoration partner whose

documentation expertise matches the complexity of the market.

5 Miles From Coconut Creek

Palm Build operates from 786 S Military Trail in Deerfield Beach — just 5 miles from Coconut Creek. We are not a franchise dispatching from Miami or a national company routing calls through a call center. Our entire South Florida operation runs from this office, and our crews know every Coconut Creek neighborhood by name.

15-25 Minute Emergency Response

Because our headquarters is 5 miles away, emergency response to anywhere in Coconut Creek — from Wynmoor to Regency Lakes to Centura Parc — is 15-25 minutes. Pre-mitigation documentation begins immediately upon arrival, before any cleanup starts. This rapid response is critical under Florida's compressed claim deadlines.

CBS Block Construction Specialists

Virtually every Coconut Creek home is CBS (concrete block structure) with stucco exterior. When moisture penetrates stucco, it wicks into the block core and cannot be dried from the surface. Our injection drying systems and thermal imaging are engineered specifically for this construction type — the dominant building method in Broward County.

Condo & HOA Dual-Policy Experts

With 72% multi-unit housing, most Coconut Creek claims involve master policy and HO-6 coordination. We prepare separate documentation packages for each carrier, map damage by responsibility zone, attend adjuster meetings for both policies, and communicate directly with HOA property management companies. This dual-documentation capability prevents the most common condo claim failure.

IICRC Certified, FL Licensed

Every technician is IICRC-certified in water damage restoration. Palm Build holds Florida DBPR mold remediation and assessment licenses — the dual licensing Florida law requires. All Xactimate estimates use localized Coconut Creek pricing from industry-standard databases, formatted for every carrier writing policies in Broward County.

Insurance Documentation from Hour One

Florida's 1-year claim deadline means documentation cannot wait. We photograph, moisture-map, thermal-image, and scope every detail your adjuster needs — formatted for your specific carrier — from the moment we arrive. Under the post-AOB framework, the quality of your contractor's documentation directly determines your claim outcome.

Palm Build's Deerfield Beach team is 5 miles from Coconut Creek — 15-25 minute response

to every neighborhood in the city.

Broward County Carrier Guide

Insurance Carriers in Coconut Creek & Broward County

Palm Build works with every carrier writing homeowners policies in Coconut Creek and

Broward County. Each carrier has different documentation standards, supplement

processes, and common pitfalls. Here are the carriers in the market with specific filing

guidance for each.

#1

Citizens Property Insurance

State (Last Resort)687K+ statewide (~15% share)

Filing Tip

Submit Xactimate-formatted estimates only. Citizens has a $700K dwelling coverage cap, excludes cosmetic hail damage, and enforces rigid documentation requirements including mandatory thermal imaging and moisture mapping for water claims. During depopulation events, your policy may transfer to a private carrier mid-claim.

Established claims process with dedicated South FL adjusters. During CAT events, out-of-state adjusters may not understand CBS construction or barrel tile replacement costs. Lead with Xactimate estimates using localized Coconut Creek pricing to prevent under-scoping.

Out-of-state adjusters during hurricanes, localized pricing gaps

#3

Universal Property & Casualty

FL-DomesticMajor FL carrier

Filing Tip

Absorbed large volume of Citizens depopulated policies. Familiar with Broward County CBS construction. Requires detailed cause-of-loss documentation and line-item Xactimate estimates. Requires thermal imaging for water damage claims.

Citizens depopulation carrier with growing Broward portfolio. Technology-forward claims process with digital documentation accepted. Coverage terms may differ from predecessor Citizens policy — review carefully after transfer.

Newer carrier processes, coverage term changes from Citizens

#5

Tower Hill Insurance

FL-DomesticEstablished FL carrier

Filing Tip

Longstanding Florida carrier with deep South Florida presence. Consistent claim handling with standard documentation requirements. Responsive to supplement filings when supported by professional evidence.

Active in Broward County with local market knowledge. Standard claim timelines with straightforward process. Requires Xactimate estimates and precise cause-of-loss classification.

Cause-of-loss classification scrutiny during hurricane events

Filing Strategy by Carrier Type

National Carriers

State Farm, Progressive/ASI, USAA

National carriers have established claims processes but often deploy out-of-state adjusters during CAT events who may not understand CBS concrete block construction, barrel tile replacement costs, or HVHZ code requirements. Xactimate documentation with localized Coconut Creek pricing prevents under-scoping.

FL-Domestic Carriers

Universal, Slide, Tower Hill, Frontline, American Integrity

Florida-domestic carriers understand local construction but often have tighter claims budgets. Detailed cause-of-loss documentation — especially wind vs. flood classification during hurricane events — is critical for full approval. These carriers scrutinize supplement requests aggressively.

Citizens & Wind Mitigation

State-backed insurer of last resort

Citizens has specific documentation requirements, a $700K dwelling cap, and unique processing timelines. Wind mitigation discounts of 15-45% are available for homes with hurricane-rated features (impact windows, hip roof, secondary water barrier). Palm Build documents wind mitigation features during restoration to support your renewal premium.

Carrier documentation requirements and claim processes vary significantly across the

Broward County market. Palm Build formats every claim for your specific carrier.

Common Questions

Coconut Creek Insurance Claims FAQ

Answers to the most common insurance restoration questions from Coconut Creek homeowners

— covering Florida deadlines, AOB reform, condo policy coordination, coverage gaps, and

the claims process.

What are the Florida filing deadlines for Coconut Creek insurance claims?

Under Florida Statute 627.70132 (amended by SB 2A), you must report property damage to your insurer within 1 year of the date of loss. Supplemental claims — for additional damage discovered after the initial claim — must be filed within 18 months of the original loss date. For hurricane losses, the 'date of loss' is the NOAA verification date, not your personal discovery date. Reopened claims must be filed within 1 year. Your insurer must begin investigation within 14 days and provide a coverage determination within 60 days. These deadlines are strictly enforced — missing them results in claim denial regardless of the damage's legitimacy.

What documentation does Palm Build provide for my Coconut Creek insurance claim?

We provide the comprehensive documentation package that Florida carriers require: moisture mapping of all affected areas using penetrating and non-penetrating meters, thermal imaging showing moisture behind walls and under flooring, photographic documentation of all damage before any mitigation work begins, daily drying logs showing dehumidifier placement and psychrometric readings, material inventories of all affected building materials, and Xactimate-formatted estimates that align with industry-standard pricing databases. For Coconut Creek's CBS stucco homes, we also document moisture wicking into concrete block cores — damage that surface-level inspections routinely miss.

How does the AOB reform affect my Coconut Creek claim?

House Bill 7065 (effective January 2023) completely banned Assignment of Benefits (AOB) for all property insurance policies issued or renewed after January 1, 2023. This means you can no longer assign your insurance benefits to a restoration company — you remain the policyholder and direct the claim. Palm Build operates exclusively under this post-reform framework: we work for you, you authorize the work, and your carrier pays you. Never sign documents that attempt to assign your insurance benefits to any contractor — any company still requesting AOB assignments after January 2023 is operating outside the law.

How does condo insurance work in Coconut Creek — master policy vs. HO-6?

In Coconut Creek's 72% multi-unit housing stock, most damage events involve two separate insurance policies. The HOA's master policy covers common elements — roofs, exterior walls, hallways, shared plumbing risers, and common area finishes. Individual unit owners carry HO-6 policies covering interior improvements, personal property, and fixtures from the drywall in. When a roof leak at Wynmoor damages a unit, the master policy covers the source repair and common element damage, while the HO-6 covers interior unit damage. When a polybutylene pipe fails inside a shared wall at Hammocks, determining which policy responds first depends on pipe ownership. Palm Build documents damage by responsibility zone from day one, creating separate documentation packages for each carrier.

Does my homeowners insurance cover flood damage in Coconut Creek?

No — standard HO-3 homeowners policies do NOT cover flood damage from rising water. This is a critical distinction in Coconut Creek, where wet-season downpours delivering 50.7 inches of annual rainfall can overwhelm drainage systems and the C-14 canal infrastructure. Your HO-3 covers sudden water damage from burst pipes, appliance failures, and rain entering through storm-damaged roofing. Rising water from overwhelmed drainage, canal overflow, or storm surge requires separate NFIP or private flood insurance. Nationally, 1 in 3 flood claims come from outside designated high-risk zones. During hurricanes, wind-driven rain (homeowners policy) and canal flooding (flood policy) often coexist in the same home. Palm Build classifies every item of damage by cause to ensure the right policy covers the right damage.

What if my Coconut Creek insurance claim is denied?

Claim denials in Coconut Creek often stem from documentation gaps — the carrier argues the damage is pre-existing, maintenance-related, or outside the covered peril. Palm Build's documentation protocol is specifically designed to prevent these denial scenarios by establishing clear cause-of-loss evidence from day one. If a denial occurs, our documentation package supports your appeal with moisture maps, thermal images, and timeline evidence that demonstrates the damage is sudden and accidental. We also identify when legitimate denials occur — for example, gradual moisture from HVAC condensation or long-term plumbing leaks that fall under maintenance exclusions — so you understand your options before investing in a dispute.

How does Palm Build help with my Coconut Creek insurance claim?

We manage the entire insurance restoration process: immediate emergency response with documentation before any cleanup begins, Xactimate-based estimates that match industry-standard pricing databases used by adjusters, direct communication with your adjuster including on-site meetings at your Coconut Creek property, supplement filing for hidden damage discovered during restoration (common in CBS stucco where moisture wicks into block cores), coordination between master policy and HO-6 carriers for condo claims, and deadline tracking to ensure your claim never expires under Florida's strict filing requirements. We do not practice law or act as public adjusters — we are restoration experts who produce the documentation your claim requires.

What is the cost of not filing an insurance claim for damage in Coconut Creek?

In Coconut Creek's subtropical climate with year-round humidity above 70%, unaddressed water damage escalates rapidly. A $3,000 pipe burst becomes a $15,000 mold remediation within two weeks. A $5,000 roof leak becomes a $40,000 structural repair when moisture saturates CBS block cores over months. Beyond repair cost escalation, Florida's 1-year filing deadline means waiting too long eliminates your ability to file entirely. Additionally, undisclosed prior damage can void coverage on future claims if your carrier discovers unreported losses during a subsequent inspection. The cost of not filing almost always exceeds the deductible you are trying to avoid.

Trusted Vendors

Trusted local pros in Coconut Creek

Outside our restoration scope, these are the vetted, licensed contractors we trust

alongside our work. Personally evaluated, reference-checked, and recommended by Palm

Build.

Insurance Claim in Coconut Creek? We Handle the Paperwork.

Palm Build handles the entire insurance process — documentation, adjuster coordination, supplement negotiation, condo master policy vs. HO-6 separation, and Florida-specific deadline compliance — so you can focus on getting your home back. We work with every carrier in the Coconut Creek and Broward County market.