Filing a restoration claim shouldn't be harder than the damage itself. Palm Build navigates the entire insurance process — documentation, adjuster coordination, supplement negotiation, and scope approval — so Charlotte homeowners get the coverage they've been paying for.

Local Office — Charlotte, NC Same day Response IICRC Certified

The Charlotte Insurance Landscape: What You're Paying For

Charlotte homeowners are paying more for insurance than ever — and many don't fully

understand what their policy covers until they need to file a claim. North Carolina's

homeowners insurance market has seen dramatic premium increases since 2020, driven by

severe weather events like Hurricane Helene, rising building material costs averaging

$180-$250 per square foot, and exploding reinsurance costs. The NC Rate Bureau secured

increases of 7.5% effective June 2025 and another 7.5% effective June 2026 — after

initially requesting 42.2% (which was rejected). Charlotte-specific rates increased even

faster at 9.3% in 2025 and 9.2% in 2026, reflecting the city's elevated severe weather

exposure and higher property values.

$2,037–$2,760

Average annual premium

Charlotte homeowners insurance cost range (2024-2026)

44.4%

Cumulative increase since 2020

NC Rate Bureau approved increases driving costs higher each year

40%

Consent-to-rate policies

Of NC policies allowing carriers to charge up to 250% of bureau rates for high-risk properties

Class 2

Charlotte CRS rating

FEMA Community Rating System — one of the highest in the Southeast, qualifying SFHA owners for up to 40% NFIP discount

The Claims Process

How the Insurance Restoration Process Works in Charlotte

From the first phone call through final claim closeout, here's exactly what happens

during a Charlotte insurance restoration claim — and how Palm Build manages each step so

you don't have to.

01

Report the Loss & Call Palm Build

Day 1

Call your insurance company to open a claim and call Palm Build simultaneously. Your policy requires you to mitigate further damage immediately — waiting for an adjuster before starting mitigation can result in secondary damage that complicates your claim. We begin emergency response and documentation while you file. Our team captures the initial damage condition with photos, video, and moisture readings before any cleanup begins — this pre-mitigation documentation is the foundation of your entire claim.

02

Initial Documentation & Emergency Mitigation

Days 1-3

Palm Build's IICRC-certified technicians document every affected area using thermal imaging, pin-type moisture meters, and comprehensive photography. We classify the damage by cause (critical for wind vs. flood distinction in storm claims), category, and class per IICRC standards. Simultaneously, emergency mitigation begins — water extraction, structural drying, board-up, soot stabilization, or mold containment depending on the loss type. Daily drying logs with data-logged moisture readings create the evidence trail your adjuster will reference.

03

Adjuster Inspection & Scope Development

Days 3-14

Your insurance company assigns a field adjuster — either a staff adjuster or an independent adjuster from a firm like Crawford, Sedgwick, or ESIS. We coordinate the inspection timing, walk the property with the adjuster, and provide our documentation package. Our Xactimate estimate is submitted alongside the adjuster's assessment. For Charlotte claims, we ensure the adjuster understands local factors like clay soil drainage affecting crawl space moisture, Charlotte's CRS Class 2 flood discount eligibility, and historic district reconstruction requirements.

04

Supplement Negotiation (If Needed)

Days 14-30

Initial adjuster estimates often miss hidden damage that's only discovered during demolition — water behind walls, mold in crawl spaces, fire damage in concealed spaces, structural issues revealed when finishes are removed. Palm Build documents supplemental damage as it's discovered and submits supplement requests with photographic evidence, moisture data, and updated Xactimate line items. Approximately 60-70% of Charlotte restoration projects require at least one supplement. Our documentation approach resolves most supplements within one revision cycle.

05

Reconstruction & Progress Documentation

Weeks 2-12

Once mitigation is complete and the reconstruction scope is approved, we begin rebuilding. Throughout reconstruction, we document progress at each major milestone — rough-in completion, inspection passage, material installation, and finish work. This ongoing documentation supports any remaining supplements and provides your carrier with evidence that the approved scope is being executed correctly. For Charlotte projects requiring Mecklenburg County LUESA permits, we include inspection records in the documentation package.

06

Final Walkthrough & Claim Closeout

Project Completion

We conduct a final walkthrough with the homeowner to confirm every scope item has been completed satisfactorily. A completion certificate is provided to your insurance carrier along with final photos, inspection records, and a summary of all work performed. Your carrier releases final payment (typically held as a recoverable depreciation holdback until work is verified complete). The claim closes when both you and your carrier agree the work meets the approved scope.

Documentation That Wins Claims

The Six Types of Documentation Your Adjuster Needs

Insurance claims are won or lost on documentation. Your adjuster makes coverage

decisions based on the evidence provided — and the format matters as much as the

content. Here are the six documentation types that Palm Build produces on every

Charlotte restoration project, and why each one matters for your claim.

Pre-Mitigation Photography

Complete photo and video documentation of all damage before any cleanup begins. This establishes the baseline condition your adjuster will reference for the entire claim. Without it, disputes over pre-existing vs. loss-related damage become difficult to resolve in your favor.

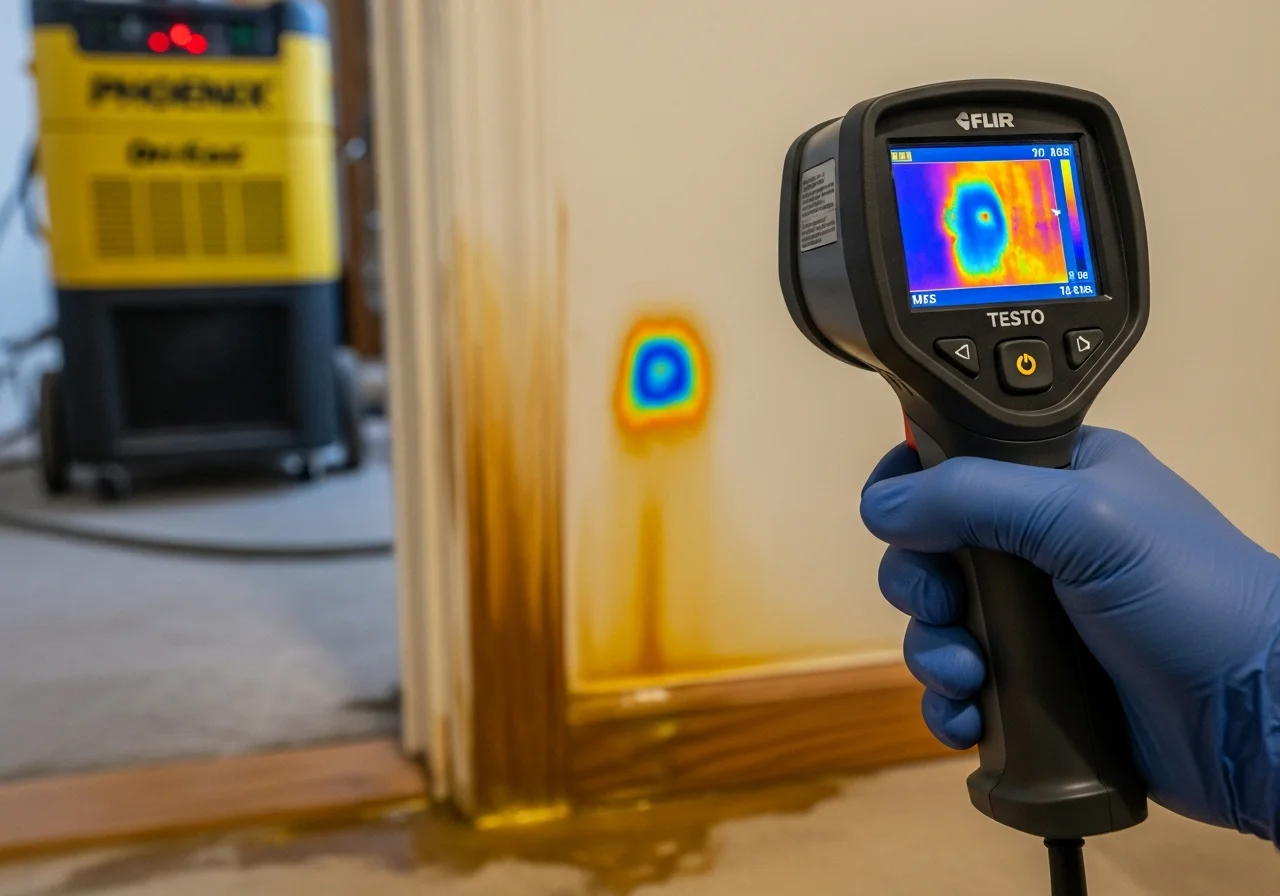

Moisture Mapping & Thermal Imaging

Infrared thermal cameras reveal moisture behind walls, under floors, and in ceilings that isn't visible to the naked eye. Pin-type and non-invasive moisture meters quantify the moisture content of every affected material. This data determines the drying scope — and proves to your adjuster exactly how far water traveled, preventing under-scoping of the claim.

Daily Drying Logs

Data-logged moisture readings taken every 24 hours during the drying process. These logs prove that professional drying was necessary, show progressive moisture reduction, and verify when materials reached their dry standard. Without daily logs, adjusters may question whether the drying timeline (and associated equipment charges) was justified.

Xactimate Scope & Estimate

Line-item estimates written in the same software and pricing database your insurance carrier uses. Every damaged item is measured, described, and priced per Xactimate's localized cost database for the Charlotte NC market. This format eliminates the back-and-forth that occurs when contractors submit estimates in different formats.

Cause-of-Loss Classification

Each item of damage is classified by its cause — wind, flood, fire, water discharge, mold — because different causes are covered by different policies or have different sublimits. For Charlotte storm claims, this distinction between wind damage (homeowners policy) and flood damage (flood policy) can mean the difference between full coverage and denial.

Progress & Completion Photos

Photography at every major milestone — demolition, rough-in, inspection, material installation, and final completion. This ongoing documentation supports supplement requests for hidden damage discovered during demolition and provides your carrier with evidence that the approved scope was executed correctly.

Know Your Coverage

What's Covered by Peril Type in Charlotte

Different damage types have different coverage rules under NC homeowners policies.

Understanding these distinctions before filing helps you avoid surprises and ensures

your claim is filed correctly from the start.

Flood from rising water (requires separate flood policy)

Wind & Storm

Covered (Separate Deductible)

Roof, siding, window damage from wind

Rain water entering through wind-created openings

Fallen tree removal and structural damage

Flood from rising water, creek overflow, dam release

NC may have separate wind/hail deductible (1-5% of dwelling value)

Common Pitfalls

Common Insurance Denials Charlotte Homeowners Face

These are the four most common reasons Charlotte restoration claims are partially or

fully denied — and how proper documentation and policy awareness can prevent each one.

Gradual Damage Exclusion

Most NC policies exclude "seepage, leakage, or slow discharge" of water. This means long-term crawl space moisture, slow pipe leaks behind walls, and gradual foundation water infiltration are commonly denied — even when the damage is significant. The key for Charlotte homeowners: if you discover a slow leak, document when you first noticed it. If it can be tied to a specific failure event (pipe joint failure, condensate line crack), it may still qualify as "sudden and accidental." Palm Build's documentation establishes the cause-of-loss timeline clearly.

Prevention: Document when damage was first noticed. Tie damage to a specific failure event when possible.

Mold Sublimit Exhaustion

NC standard policies typically cap mold coverage at $5,000 to $10,000. Charlotte crawl space mold remediation frequently costs $15,000 to $50,000+. When the sublimit is exhausted, remaining costs fall to the homeowner. However, when mold results from a covered sudden water event (burst pipe), the mold remediation may be covered as part of the water damage claim rather than under the mold sublimit. Palm Build's documentation connects mold to the original covered loss when applicable — potentially bypassing the sublimit entirely.

Prevention: Ask your agent about enhanced mold endorsements. Document the moisture source that caused mold growth.

Wind vs. Flood Misclassification

During storm events like Hurricane Helene, Charlotte homes often experience both wind damage (covered by homeowners) and flood damage (requires separate flood policy). Without cause-specific documentation, insurers may attribute water intrusion to flooding (excluded) rather than wind-driven rain entry (covered). This single classification decision can mean the difference between a $50,000 approved claim and a denial. Palm Build documents damage by entry point — water entering through a wind-damaged roof opening is wind damage, not flood damage.

Prevention: Ensure your restoration company documents damage by cause, not just by room or material.

Code Upgrade Denial

Charlotte requires reconstruction to meet current building code, not original code. For a 1960s brick ranch, this can mean $5,000-$15,000 in mandatory electrical, insulation, and safety upgrades. Without an ordinance-and-law endorsement on your policy, these costs are excluded. Many Charlotte homeowners discover this gap only after reconstruction begins and the code-required upgrades are already underway.

Prevention: Confirm you have an ordinance-and-law endorsement on your policy. Add it before you need it — the cost is minimal.

Industry-Standard Estimating

Why Xactimate Estimates Get Your Claim Approved Faster

Xactimate is the industry-standard estimating software used by virtually every

insurance carrier in North Carolina to price restoration work. When a restoration

company submits an estimate in a different format — a handwritten bid, a generic

spreadsheet, or a competing software — the adjuster must manually translate every line

item into Xactimate for comparison. This adds days to weeks of processing time and

creates opportunities for items to be missed, misinterpreted, or disputed.

Palm Build writes every estimate in Xactimate using the same pricing database,

line-item codes, and measurement standards that your Charlotte-area adjuster uses.

When our estimate arrives, the adjuster can approve it line-by-line without conversion

— dramatically reducing the time between scope submission and claim approval.

Benefits of Xactimate-Based Estimates

Eliminates format-based disputes — your estimate speaks the adjuster's language

Uses localized Charlotte NC pricing database reflecting actual local labor and material costs

Line-item detail matches the granularity adjusters use for approval decisions

Supplements are submitted in the same format — no conversion or re-entry needed

Reduces approval timeline from weeks to days for straightforward claims

Creates an auditable record that protects both you and the carrier

We Work With Every Carrier

Charlotte Insurance Carriers We Work With

Palm Build works with every major insurance carrier writing homeowners policies in the

Charlotte market. Our Xactimate-based documentation and estimating process is designed

to work with any carrier's claims workflow.

Allstate

Nationwide

Auto-Owners

State Farm

USAA

Liberty Mutual

Travelers

Progressive

SageSure

Safeco

Homeowners of America

Erie Insurance

Amica Mutual

NFIP (National Flood Insurance Program)

The Palm Build Difference

Why Charlotte Homeowners Choose Palm Build for Insurance Claims

Xactimate-Native Estimating

Every estimate, supplement, and change order is written in the same software and pricing database your carrier uses. No format translation, no re-entry errors, no weeks of back-and-forth over estimate structure. This single capability accelerates Charlotte claim approvals more than any other factor.

No Out-of-Pocket Insurance Coordination

Our insurance coordination, documentation, adjuster meetings, and supplement negotiation are included in the restoration scope and paid by your carrier — not out of your pocket. Your only direct cost is your policy deductible.

Direct Adjuster Communication

We meet with your adjuster on-site, walk the property together, and provide our documentation package directly. This face-to-face coordination resolves questions faster than email chains and phone tag. For Charlotte's high-volume adjusters managing dozens of claims simultaneously, a well-organized contractor who speaks their language gets priority attention.

Supplement Resolution in One Cycle

Approximately 60-70% of Charlotte restoration projects require at least one supplement for hidden damage discovered during demolition. Our supplemental documentation includes photos, moisture data, and updated Xactimate line items submitted within 48 hours of discovery. Most Palm Build supplements resolve in one revision cycle.

Cause-Specific Documentation

We classify every item of damage by its cause — wind, flood, sudden water, fire, mold. This protects Charlotte homeowners from incorrect coverage determinations, especially during storm events where wind damage (covered) and flood damage (separate policy) may coexist. No other local restoration company documents at this level of cause-specificity.

Common Questions

Charlotte Insurance Claims FAQ

Does Palm Build work with my insurance company in Charlotte?

Yes — we work with every major carrier writing policies in the Charlotte market including Allstate, Nationwide, Auto-Owners, State Farm, USAA, Liberty Mutual, Travelers, Progressive, and SageSure. Our documentation and estimates use the same Xactimate software and pricing database that your carrier uses, which reduces disputes and speeds approval.

Should I call my insurance company or Palm Build first?

Call Palm Build first — or at least simultaneously. Your insurance policy requires you to mitigate further damage immediately, and documenting the initial damage condition before cleanup begins is critical for your claim. We can begin emergency mitigation and documentation while you open your claim with your carrier. Waiting for an adjuster before starting mitigation can result in secondary damage that complicates your claim.

How much does Palm Build charge for insurance coordination?

Nothing additional. Insurance coordination, documentation, adjuster meetings, and supplement negotiation are included as part of our restoration scope. Our fees are paid by your insurance carrier as part of the approved claim — not out of pocket. You are responsible for your policy deductible, which is the only out-of-pocket cost for a covered loss.

What if my insurance company denies part of my claim?

Partial denials are common, especially for items like mold remediation (sublimited coverage), code upgrades (requires ordinance-and-law endorsement), and gradual damage (excluded under most policies). Palm Build helps you understand which items are covered vs. excluded, documents covered items thoroughly to prevent incorrect denials, and files supplements with supporting evidence when legitimate claim items are initially denied.

What is Xactimate and why does it matter?

Xactimate is the industry-standard estimating software used by virtually all insurance carriers to price restoration work. When your restoration company submits estimates in a different format, the adjuster has to manually re-enter and cross-reference every line item — adding days to weeks of delay and creating opportunities for items to be missed or disputed. Palm Build writes every estimate in Xactimate, matching the exact format and pricing database your adjuster uses.

How long does the insurance claims process take in Charlotte?

For straightforward covered losses (burst pipe, kitchen fire), the claims process typically takes 1-3 weeks from initial filing to scope approval. Complex claims involving multiple damage types (storm with both wind and flood), disputed coverage, or large losses can take 4-12 weeks. Major catastrophe events like Hurricane Helene created claims backlogs that extended processing times significantly across all Charlotte-area carriers.

What documentation does my insurance company need?

Your carrier needs: initial damage photos and video (before any cleanup), cause-of-loss determination, moisture mapping and readings, a detailed scope of work with line-item pricing (Xactimate format), daily drying logs showing progress, photos at each stage of mitigation and reconstruction, and final completion documentation. Palm Build produces all of this as a standard part of every Charlotte project.

What about Charlotte's rising insurance rates?

Charlotte homeowners insurance rates increased 9.3% in 2025 and another 9.2% in 2026, with cumulative increases of 44.4% since 2020. Average annual premiums now range from $2,037 to $2,760. Despite rising costs, filing a legitimate claim for covered damage is exactly what your policy is for. Palm Build's thorough documentation helps ensure your claim is processed efficiently and completely — so you get full value from the premiums you're paying.

Need Help With a Restoration Insurance Claim in Charlotte?

Palm Build handles the entire insurance process — documentation, adjuster coordination, supplement negotiation — so you can focus on getting your home back. We work with every major carrier in the Charlotte market.