With 67% of York residents living in owner-occupied homes and a median home value of $198,600, most property damage claims here are deeply personal — your own house, your own policy, your own savings on the line. Palm Build navigates the South Carolina insurance landscape for York homeowners, producing airtight documentation that separates flood damage from covered water loss, establishes mold as a direct consequence of the original event, and keeps your claim moving through the adjuster pipeline without unnecessary delays or denials.

Charlotte Office — ~35 minutes to York 45-75 min Response IICRC Certified

The York SC Insurance Landscape: What Homeowners Need to Know

York sits in the heart of York County, South Carolina — a competitive private insurance

market that operates very differently from Florida's state-run Citizens model. With a

67% owner-occupied housing rate and a median home value of $198,600, most York

homeowners carry standard HO-3 policies from national carriers like State Farm,

Allstate, or Erie. Premiums run below the South Carolina statewide average thanks to the

Piedmont location away from coastal hurricane exposure. But lower premiums don't mean

simpler claims. Properties near Langham Branch and Bullock Creek sit in FEMA flood zones

that require separate NFIP coverage, and York's older housing stock — many homes built

in the 1960s through 1990s — introduces age-related coverage complexities around

plumbing failures, outdated wiring, and building code compliance gaps. Palm Build

understands these York-specific dynamics and builds every claim file around them.

Standard SC Market

No Citizens-style state insurer

Unlike Florida, South Carolina uses a competitive private market — York homeowners choose from State Farm, Allstate, Erie, and regional carriers without a state-run insurer of last resort

67% owner-occupied

York homeownership rate

Two-thirds of York households own their home, meaning most residential claims are filed by homeowners navigating the process for the first time rather than experienced landlords

$198,600

Median home value

York median home values sit below the York County average, but restoration costs follow material and labor pricing — not home value — so claims can still exceed expectations

Flood Zones

Langham Branch & Bullock Creek

Properties near Langham Branch and Bullock Creek corridors require separate NFIP flood insurance — standard homeowners policies exclude rising water regardless of location

York's Older Housing Stock Challenge

Many York homes were built between the 1960s and 1990s — before modern building codes

required updated plumbing materials, electrical standards, and moisture barriers. When

water damage strikes these older homes, restoration often triggers code-upgrade

requirements that standard policies don't cover without an Ordinance or Law

endorsement. Adjusters unfamiliar with York's housing age profile may not anticipate

these costs.

Palm Build documents code-compliance gaps during the initial inspection so supplement

requests for code upgrades are filed proactively rather than discovered mid-project

when they cause delays and out-of-pocket surprises.

The Claims Process

8-Step Insurance Claims Process for York SC Homeowners

From documenting the damage through final walkthrough, here's exactly how the insurance

restoration process works in York — and how Palm Build manages every step so you can

focus on your family instead of your claim.

01

Document the Damage

Immediately

Before touching anything, photograph and video every affected area of your York home. Capture wide shots of each room, close-ups of visible damage, and any standing water or structural issues. Document the source of damage if identifiable — a burst pipe joint, a storm-damaged section of roof, or a failed appliance connection. This initial documentation establishes the pre-mitigation baseline that your insurance adjuster will reference throughout the entire claim. Palm Build supplements your photos with thermal imaging and moisture mapping on arrival.

02

File Your Insurance Claim

Day 1

Contact your insurance carrier to open a claim — or call Palm Build first and we can guide you through the filing process. Provide your policy number, the date of loss, and a brief description of the damage. Your carrier will assign a claim number and schedule an adjuster inspection. For York homeowners, most carriers operating in the SC Piedmont region assign field adjusters within 3-7 business days for non-catastrophe events. During CAT events like major storms, timelines extend significantly.

03

Emergency Mitigation

Days 1-3

Your policy requires you to mitigate further damage immediately — and in York's humid Piedmont climate, waiting even 24-48 hours before beginning water extraction and structural drying can result in secondary mold growth that complicates your claim. Palm Build's IICRC-certified technicians begin emergency response while documenting every step: water extraction volumes, equipment placement, daily moisture readings, and material classifications. This simultaneous mitigation-and-documentation approach satisfies your duty to mitigate while building the evidence your adjuster needs.

04

Adjuster Meeting

Days 3-14

Your carrier assigns a field adjuster — staff or independent — to inspect the property. Palm Build coordinates the inspection timing, walks the property alongside the adjuster, and presents our complete documentation package: pre-mitigation photos, thermal imaging results, moisture maps, daily drying logs, and a preliminary Xactimate estimate formatted in the same software and SC regional pricing database the adjuster uses. Having this documentation ready at the first inspection eliminates the back-and-forth that delays York claims by weeks.

05

Scope Agreement

Days 7-21

The adjuster submits their estimate to the carrier for approval. If Palm Build's documented scope exceeds the adjuster's initial assessment — common when hidden damage behind walls or under York's older hardwood floors is involved — we submit a detailed scope disagreement with supporting evidence. Most scope agreements in York are reached within one revision cycle because our documentation format matches the carrier's internal system, leaving little room for interpretation disputes.

06

Restoration Work

Weeks 2-10

Once the scope is approved, reconstruction begins. Palm Build manages the entire process — demolition of damaged materials, structural repairs, drywall installation, flooring replacement, painting, and finish work. For older York homes, we ensure all work meets current York County building code requirements, documenting any code-upgrade items that were included in the approved scope. Progress photos at every milestone give your carrier evidence that the approved work is being executed as agreed.

07

Supplemental Claims

As Discovered

Hidden damage frequently appears once demolition begins — moisture behind baseboards, mold in wall cavities, deteriorated subfloor beneath tile, or compromised insulation in attic spaces. Palm Build documents supplemental damage the moment it's discovered with photographs, updated moisture data, and revised Xactimate line items. For York properties built before the 1990s, supplemental discoveries are especially common due to older construction materials and methods. Our documentation approach resolves most supplements in a single revision cycle.

08

Final Walkthrough

Project Completion

A final walkthrough confirms every approved scope item has been completed to your satisfaction. Palm Build provides a completion certificate, final photographs, and a comprehensive summary of all work performed — triggering release of any held recoverable depreciation from your carrier. The claim closes when both you and your insurance company agree the restoration meets the approved scope. Your York home is restored to pre-loss condition or better.

Coverage Gaps

5 Insurance Coverage Gaps Every York SC Homeowner Should Know

York homeowners benefit from South Carolina's competitive private insurance market with

premiums well below coastal rates — but those savings come with coverage gaps that

surface at the worst possible time. Understanding these limitations before you file a

claim helps Palm Build build a strategy that maximizes your payout.

Flood Exclusion (Separate NFIP Required)

Full cost out of pocket without NFIP

Standard homeowners insurance does NOT cover flood damage from rising water. Most York homes sit outside FEMA mandatory flood zones, but properties near Langham Branch, Bullock Creek, and Turkey Creek corridors do flood during heavy rain events. When it happens, homeowners without separate NFIP flood insurance face the entire restoration cost out of pocket. Even York properties outside designated flood zones can purchase NFIP Preferred Risk Policies at significantly reduced rates.

Typically Covered

Burst pipe water damage

Appliance line failures

Sudden roof leaks from storms

Typically Not Covered

Rising floodwater

Creek overflow

Surface water runoff

Storm surge

Gradual Damage Exclusion

Complete denial if classified as gradual

Insurance covers sudden and accidental events — not gradual deterioration. Slow pipe leaks, long-term crawl-space moisture, and seepage through foundation walls are excluded. In York's older housing stock with original plumbing from the 1960s-1980s, the line between "sudden" and "gradual" is exactly where claims get denied. Palm Build's documentation establishes clear causation timelines with moisture data that proves sudden origin, preventing carriers from reclassifying a covered loss as gradual deterioration.

Typically Covered

Sudden pipe burst

Appliance failure

Storm-caused roof leak

Typically Not Covered

Slow leak over weeks/months

Long-term condensation damage

Foundation seepage

Normal wear and tear

Maintenance-Related Damage

Claim denied as maintenance issue

Insurance policies exclude damage that results from lack of maintenance. In York, this frequently applies to aging roof systems, deteriorated caulking around windows and doors, and crawl-space moisture barriers that have degraded over decades. When a storm causes water intrusion through a maintenance-deferred area, the carrier may deny the claim as a maintenance issue rather than storm damage. Palm Build documents the specific storm-caused entry point separately from any pre-existing maintenance conditions — establishing that the covered peril caused the loss, not deferred maintenance.

Typically Covered

Wind damage to properly maintained roof

Storm-driven rain through sudden breach

Typically Not Covered

Leaks through worn-out roofing

Water entry from deteriorated caulking

Degraded moisture barriers in crawl spaces

Mold Coverage Sublimits

$5K-$10K cap vs. $8K-$30K+ actual cost

Standard York County policies cap mold coverage at $5,000-$10,000. York crawl-space mold remediation routinely costs $8,000-$30,000+. The sublimit is exhausted before the project is half complete. The key to maximizing mold coverage is connecting the mold directly to a covered water damage event — with documented causation timelines showing the mold developed within the covered loss window. Palm Build establishes this chain of causation with timestamped moisture data and environmental testing results.

Typically Covered

Mold from sudden pipe burst (up to sublimit)

Mold testing after covered water loss

Typically Not Covered

Mold from long-term humidity

Pre-existing mold conditions

Mold exceeding sublimit without supplement

Sewer Backup (Optional Rider Required)

Zero coverage without endorsement

Sewer and drain backup is NOT covered under standard SC homeowners policies — it requires a separate endorsement that most York homeowners don't realize they need until it's too late. York's older municipal sewer infrastructure and tree root intrusion from established neighborhoods cause backups that send Category 3 contaminated water into finished living spaces. The endorsement typically costs $40-$75/year but provides $5,000-$25,000 in coverage. Without it, the entire cleanup and restoration falls on the homeowner.

Typically Covered

Sewer backup (with endorsement only)

Drain overflow from sudden blockage (with endorsement)

Typically Not Covered

Sewer backup without endorsement

Septic system failures

Gradual drain deterioration

Flood vs. Standard Claims

Standard Homeowners vs. Flood Insurance: Two Different Processes for York

York properties near Langham Branch and Bullock Creek may need both policy types — and

when a storm causes both rising water and wind-driven rain damage simultaneously, two

entirely separate claims processes run in parallel. Understanding the differences before

you file prevents costly mistakes that delay or reduce your payout.

Standard Homeowners Claim

HO-3 Policy — Covered Perils

Covered Events

Burst pipes, appliance failures, storm-driven rain through sudden breach, fire, wind damage, fallen trees

Filing Process

Call your carrier directly. Claim number assigned within 24 hours. Field adjuster scheduled within 3-7 business days for non-CAT events in York County.

Documentation

Pre-mitigation photos, moisture maps, thermal imaging, daily drying logs, Xactimate estimate in SC regional pricing. All submitted to your carrier adjuster.

Typical Timeline

3-7 days to adjuster visit, 7-21 days for scope agreement, 2-10 weeks for restoration. Total: 4-14 weeks for a standard York water damage claim.

Depreciation

Replacement Cost Value (RCV) policies pay Actual Cash Value (ACV) first, then release recoverable depreciation upon completion. Most York policies are RCV.

Deductible

Standard flat deductible of $1,000-$2,500 for most York homeowners. Applied once per claim event regardless of damage scope.

NFIP Flood Insurance Claim

Separate Policy — Rising Water Only

Covered Events

Rising water from Langham Branch, Bullock Creek, or Turkey Creek overflow. Surface water runoff. Storm surge. Mudflow. NOT covered by your standard homeowners policy.

Filing Process

File with your NFIP carrier (separate from homeowners). FEMA-trained adjuster assigned — different adjuster, different process, different documentation requirements than your standard claim.

Documentation

NFIP requires specific proof-of-loss forms, signed and sworn. Damage must be attributed specifically to rising water — not rain, not pipe failure. Palm Build separates flood-caused damage from other causes in our documentation.

Typical Timeline

NFIP proof-of-loss must be filed within 60 days of the flood event. Adjuster inspections may take longer during widespread flood events. Total resolution: 2-6 months for York flood claims.

Coverage Limits

NFIP max: $250,000 building / $100,000 contents. No recoverable depreciation — NFIP pays ACV only. Finished basements and below-grade improvements have significant limitations.

Deductible

NFIP deductibles range from $1,000-$10,000 depending on your selected plan. Separate from your homeowners deductible — both apply if you have both types of damage from one event.

Dual-Claim Events in York: When Both Policies Apply

When a severe storm causes both rising water from Langham Branch flooding and

wind-driven rain through damaged roofing, York homeowners may need to file two

separate claims with two separate carriers simultaneously. Palm Build documents damage

by cause — attributing each item to either the standard homeowners policy or the NFIP

flood policy — so neither carrier denies coverage by pointing to the other. This

cause-by-cause attribution is especially critical in York, where creek proximity and

storm intensity can create both flood and wind damage in a single event.

Documentation That Wins Claims

What Palm Build Documents on Every York Insurance Claim

Insurance claims are won or lost on documentation. Your adjuster makes coverage

decisions based on the evidence provided — and the format matters as much as the

content. Here's what Palm Build produces on every York restoration project.

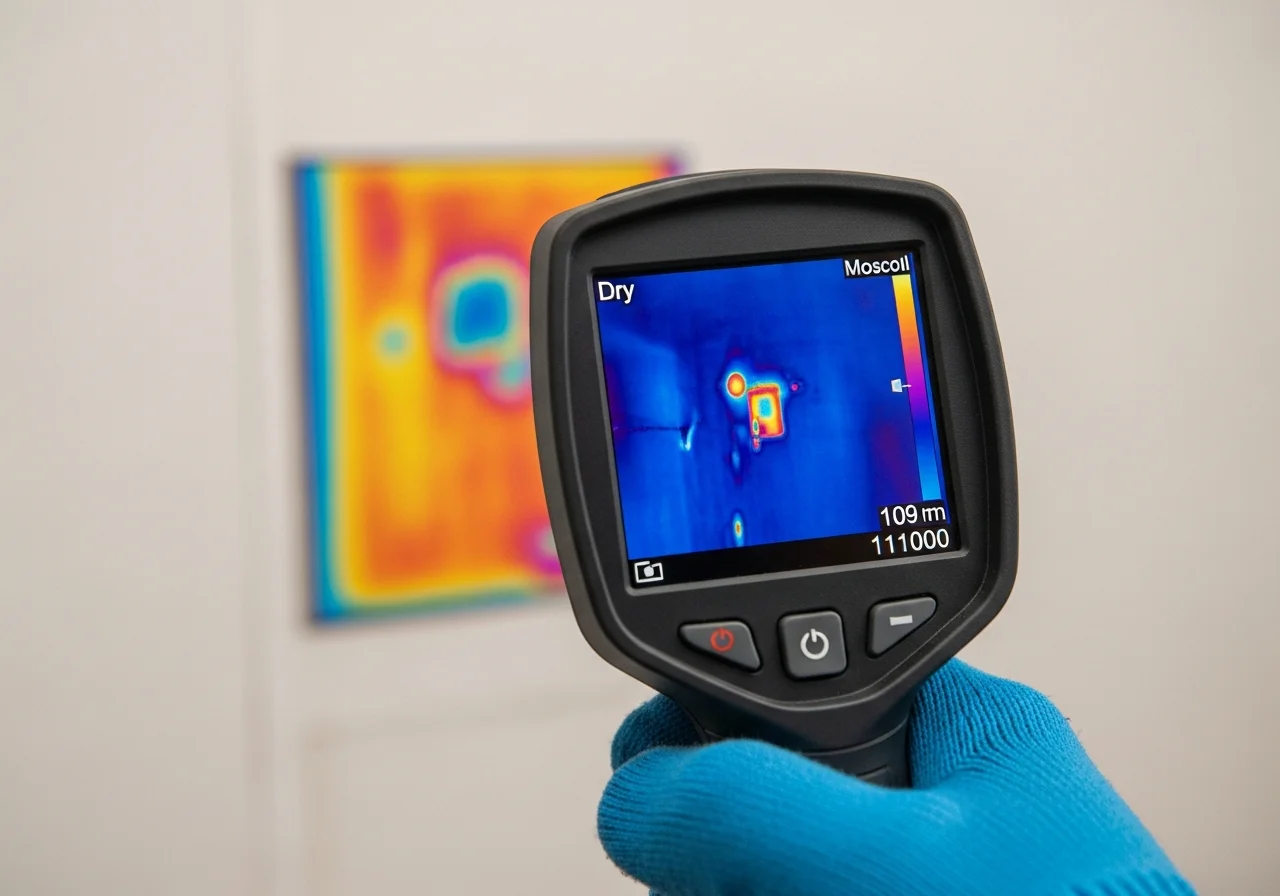

Thermal Imaging & Moisture Maps

Infrared thermal cameras reveal moisture trapped behind walls, under floors, and in ceiling cavities that isn't visible to the naked eye. In York's older homes with plaster walls and hardwood subfloors, hidden moisture can persist for weeks before visible damage appears. Our thermal imaging pinpoints every affected area so your adjuster sees the full scope on the first inspection — preventing under-scoped estimates that leave hidden damage unclaimed.

Calibrated Moisture Meter Readings

Pin-type and non-invasive moisture meters quantify the moisture content of every affected material — drywall, studs, subfloor, insulation — with calibrated readings your adjuster can verify independently. These readings prove scope of damage at initial inspection and verify when materials have reached dry standard during the drying process. For York claims, establishing exact moisture levels at time of loss prevents carriers from disputing the extent of water intrusion.

Daily Drying Records

Data-logged moisture readings taken every 24 hours throughout the structural drying process. These logs prove that professional drying was necessary, document progressive moisture reduction toward IICRC dry standard, and verify the timeline. For York mold claims, establishing that the drying process began within 24-48 hours of the loss event — and that conditions didn't support mold growth during covered drying — is often the difference between covered and denied.

Pre-Mitigation Photo & Video Logs

Complete photographic and video documentation of all damage before any cleanup begins. Wide shots establish room context, close-ups capture material damage, and video walkthroughs show water levels, smoke patterns, or structural displacement. Every image is timestamped and geotagged to your York property address. This baseline documentation is what your adjuster references for the entire claim — without it, disputes over pre-existing conditions become impossible to resolve.

Xactimate Scope-of-Work Estimates

Line-item estimates written in the same Xactimate software and SC regional pricing database your insurance carrier uses. Every damaged item is measured, described, and priced per current York County market rates. This format eliminates the translation delays that occur when contractors submit estimates in spreadsheets or competing software — and gives adjusters a document they can approve line-by-line without reformatting.

Thermal imaging reveals moisture trapped behind walls — critical for proving full claim

scope to York adjusters

Calibrated moisture meter readings provide the quantified data adjusters need to approve

full restoration scope

Documentation in Action

Insurance Restoration: From Damage to Settlement in York SC

Every step of the York insurance restoration process is documented — from initial damage

assessment through final walkthrough — ensuring your carrier has the evidence needed to

approve the full scope of work.

Claims consultation: Reviewing damage documentation and policy coverage with York homeowners

Structural drying: Equipment placement and daily moisture logs verify the full scope of services

Before and after: Insurance-covered kitchen restoration from water damage in York

Final result: York living room restored to pre-loss condition through the insurance claims process

Common Questions

York SC Insurance Restoration FAQ

Answers to the questions York and York County homeowners ask most often about the

insurance claims and restoration process.

Does Palm Build work with South Carolina insurance carriers in York?

Yes. We work with every major carrier writing policies in York and York County — State Farm, Allstate, Nationwide, USAA, Travelers, SC Farm Bureau, and smaller regional carriers. Our estimates are written in Xactimate at current South Carolina regional pricing, matching the exact format and database your carrier's adjuster uses. This eliminates the back-and-forth that delays claims when restoration contractors submit estimates in incompatible formats.

Does my York homeowners policy cover flood damage?

Almost certainly not. Standard homeowners policies in York County exclude flood damage — meaning any water that enters your home from an external rising source, including Langham Branch overflow, Bullock Creek flooding, or overwhelmed storm drains. Separate flood insurance through the National Flood Insurance Program (NFIP) or a private flood policy is required. This distinction is critical after heavy rain: water from a burst pipe is typically covered under your standard policy, but water rising from a swollen creek or backed-up storm drain is flood damage requiring separate coverage. Palm Build documents the precise source and path of water intrusion to support the correct coverage determination.

What about mold coverage on my York SC policy?

Most standard homeowners policies in York include a mold sublimit of $5,000 to $15,000 — and South Carolina does not have specific mold coverage mandates requiring carriers to offer higher limits. If water damage goes undetected for 48-72 hours — common in York's humid summers — secondary mold growth can quickly exceed that sublimit. The critical strategy is documentation timing: if we can establish that the mold resulted directly from a covered water event and document the causal chain from day one, the remediation may be processed under the primary water damage claim rather than triggering the standalone mold sublimit.

Should I call my insurance company or Palm Build first?

Call Palm Build first — or at least simultaneously. Your policy requires you to mitigate further damage immediately, and documenting initial damage conditions before any cleanup begins is essential for your claim. We begin emergency mitigation and documentation while you open your claim with your carrier. Waiting for an adjuster before starting mitigation can result in secondary damage — especially mold in York's humid climate — that complicates your claim or triggers coverage exclusions for failure to mitigate.

What documentation does my insurance carrier need for a York SC claim?

Your carrier needs: initial damage photos and video before any cleanup, cause-of-loss determination, moisture mapping with calibrated meter readings, thermal imaging of hidden moisture, a detailed scope of work with Xactimate line-item pricing, daily drying logs showing progress toward drying goals, photos at each stage of mitigation and reconstruction, and final completion documentation. For flood-related claims, separate documentation tracks are required for your NFIP or private flood policy. Palm Build produces all of this as standard on every York project — our documentation packages are formatted specifically for how SC adjusters process claims.

How long does the insurance claims process take in York?

For a straightforward covered loss — a burst supply line or appliance failure — the process typically takes 1-3 weeks from initial filing to scope approval. Claims involving disputed coverage between flood and standard water damage, mold remediation that may exceed sublimits, or larger multi-room losses can take 4-10 weeks. Claims involving York County floodplain compliance requirements for substantial improvements may add additional time for permitting. Palm Build's organized documentation packages minimize back-and-forth with adjusters and keep timelines on the shorter end.

What if my insurance company denies part of my claim?

Partial denials are common in York, particularly for mold remediation (sublimited coverage), gradual or maintenance-related damage (excluded), flood damage filed under a standard policy (excluded — requires separate flood insurance), and code upgrade costs (requires ordinance-and-law endorsement). Palm Build helps you understand which items are covered vs. excluded, documents all covered items thoroughly to prevent incorrect denials, and files supplements with supporting evidence when legitimate claim items are initially denied. We do not perform public adjuster activity — our role is as your licensed restoration contractor providing complete, defensible documentation.

Insurance Claim in York?

Palm Build handles the entire insurance process — documentation, adjuster coordination, cause-of-loss determination, flood vs. standard claim separation, supplement filing — so you can focus on getting your home back. We work with every major carrier in the York County market.