Insurance Restoration Process in Boynton Beach, FL

Palm Beach County homeowners pay an average of $6,327 per year in insurance premiums — among the highest in Florida. When damage strikes your Boynton Beach home, filing a restoration claim shouldn't be harder than the damage itself. Palm Build navigates the entire insurance process — documentation, adjuster coordination, supplement negotiation, and scope approval — including Florida-specific deadlines, AOB reform compliance, Citizens Property Insurance protocols, and wind vs. flood classification — so you get the coverage you've been paying for.

Deerfield Beach — 20 Minutes from Boynton Beach Same day Response IICRC Certified

"The Adjuster Is Offering $4,200 on an $18,000 Claim."

Your Aberdeen Golf & Country Club home flooded three weeks ago. The restoration

company dried everything. Now you're staring at a partial denial letter from Citizens

Property Insurance — they're covering only $4,200 of your $18,000 claim. The adjuster

says the water intrusion through the CBS stucco wall was "gradual seepage," not sudden

and accidental. The mold remediation is "excluded under your sublimit." The barrel

tile replacement is "cosmetic, not structural."

You're paying $6,327 a year in premiums — among the

highest in Florida — and your carrier is denying two-thirds of a legitimate claim. Your

hurricane deductible alone is 2–5% of your dwelling value. You did everything right: you

called within 24 hours, you hired a restoration company, you filed on time. But the restoration

company didn't document the damage in the adjuster's language. No moisture mapping. No thermal

imaging. No Xactimate-formatted scope of loss. No cause-of-loss classification separating

wind from flood from sudden discharge.

This is the call Palm Build answers every week from Boynton Beach homeowners — from

Aberdeen estates to Hunters Run condos, from Canyon Isles villas to Leisureville ranch

homes. The difference between $4,200 and $18,000 isn't your policy. It's your

documentation.

What Boynton Beach Homeowners Are Paying for Insurance

Avg. Annual Premium

Palm Beach County average — among the highest in Florida

$6,327

Hurricane Deductible

Percentage of dwelling value, not a flat dollar amount

2–5%

Flood Risk Properties

Boynton Beach homes with substantial flood risk (FEMA + First Street)

42.2%

Don't Let Poor Documentation Cost You Thousands

Call now for a free insurance claim consultation. We'll review your policy and

document your damage properly from day one.

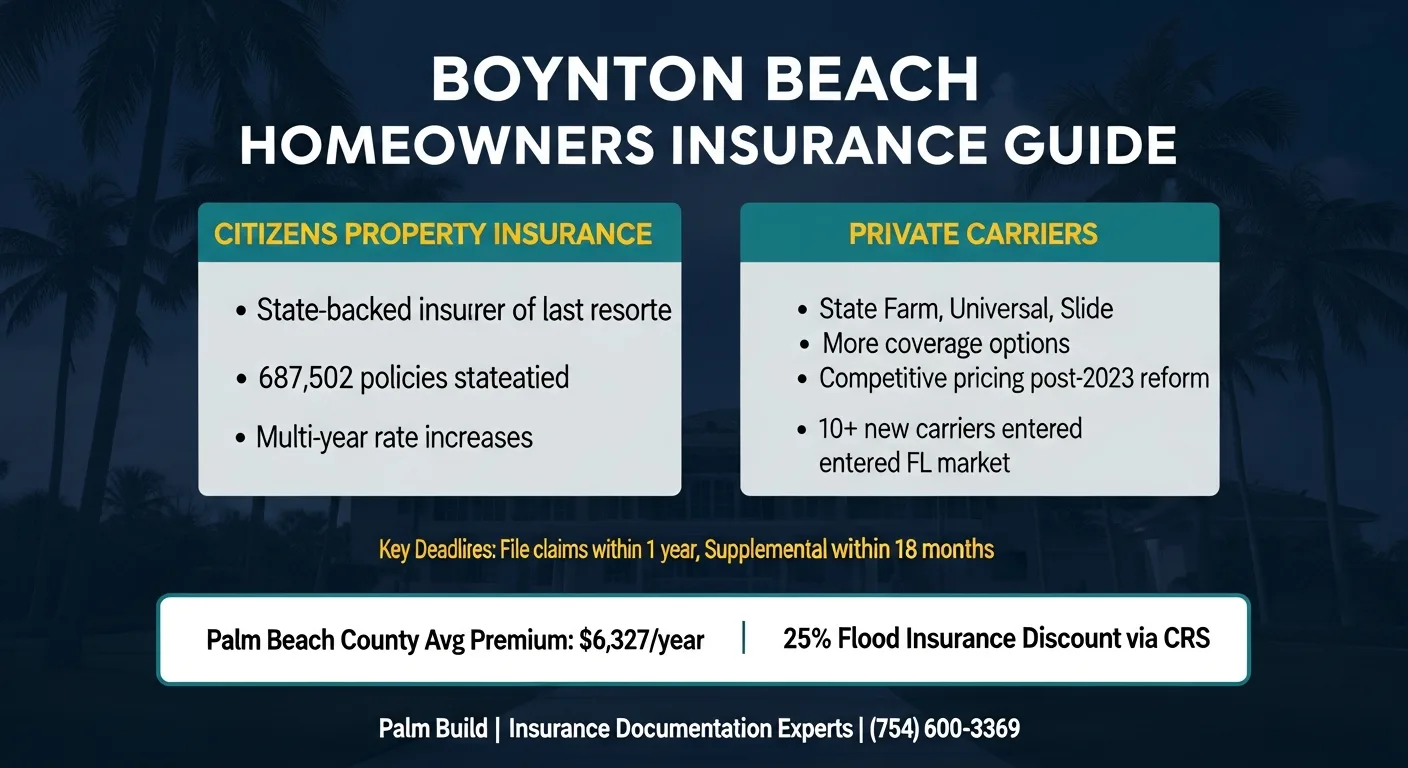

Boynton Beach homeowners face one of the most expensive and volatile insurance markets

in the country. With average annual premiums hitting $6,327 in Palm Beach County —

roughly three times the national average — every claim dollar matters. Citizens Property

Insurance Corporation dominates the market with 687,000 policies statewide, but the

post-2023 reform landscape has brought 10+ new private carriers competing for Florida

homeowners. Meanwhile, 42.2% of Boynton Beach properties carry substantial flood risk,

and the city's Community Rating System (CRS) participation earns residents up to 25% off

NFIP flood premiums. The market is changing fast — understanding it before you file a

claim determines whether you recover fully or absorb thousands in uncovered costs.

$6,327/yr

Avg. annual premium

Palm Beach County average — among the highest in Florida, 3x the national average

687K

Citizens policies statewide

Citizens Property Insurance is the dominant carrier for South Florida homeowners

10+ New Carriers

Since 2023 reform

SB 2A and tort reform attracted new private market entrants to compete with Citizens

Volatile Market

Carrier exits & entries

6+ carriers exited FL since 2020 while 10+ entered post-reform — constant market churn

42.2%

Flood-risk properties

Boynton Beach properties with substantial flood risk per FEMA and First Street Foundation

25% CRS Discount

NFIP flood savings

Boynton Beach CRS rating earns residents up to 25% discount on NFIP flood premiums

Know Your Carrier

Citizens vs. Private Carriers in Boynton Beach

Your claims experience depends heavily on whether you're insured through Citizens (the

state-backed insurer of last resort) or a private carrier. The post-2023 reform

landscape has reshaped both options — here's what Boynton Beach homeowners need to know.

Citizens Property Insurance

State-backed insurer of last resort

State-backed, not-for-profit — insurer of last resort when private carriers decline

687,000+ policies statewide, heavily concentrated in South Florida

Limited coverage options — no luxury endorsements, basic dwelling form

Multi-year rate increases mandated by legislature (up to 14% annually)

Depopulation programs actively moving policyholders to private carriers

Slower claims processing — fewer adjusters per claim volume

Private Carriers

State Farm, Universal, Slide, Tower Hill, others

10+ new carriers entered Florida since 2023 tort reform (SB 2A)

More coverage options — including hurricane deductible buydowns and mold endorsements

Competitive pricing post-reform: many undercutting Citizens by 10-20%

State Farm, Universal, Slide, Tower Hill, Frontline among largest in Palm Beach County

Faster claims processing — smaller portfolios, dedicated South Florida adjusters

Risk-based pricing — well-maintained homes with mitigation features get lower rates

AOB Prohibition (Jan 2023)

Senate Bill 2A eliminated Assignment of Benefits for new property insurance claims. You can no longer assign your policy benefits to a restoration company. You remain the policyholder, authorize all work, and your carrier pays you directly. Any contractor asking you to sign an AOB is operating outside the law.

1-Year Filing / 18-Month Supplement Deadline

Florida Statute 627.70132 requires policyholders to report property damage within 1 year of the loss date (reduced from 2 years by SB 2A). Supplemental claims for hidden damage discovered during restoration must be filed within 18 months of the original loss date. Miss either deadline and your carrier owes you nothing — regardless of how legitimate the damage.

The Claims Process

How the Insurance Restoration Process Works in Boynton Beach

From the first phone call through final claim settlement, here's exactly what happens

during a Boynton Beach insurance restoration claim — including Florida-specific

deadlines, AOB reform impacts, and how Palm Build manages each step.

01

Document Damage & Make Two Calls

Day 1

Take photos and video of all visible damage before touching anything. Then make two calls: your insurance company to open a claim, and Palm Build for emergency response. Under Florida Statute 627.70132, you must report damage within 1 year of the loss date. Your policy also requires immediate mitigation to prevent further damage. We arrive in 30-45 minutes and begin emergency work and documentation simultaneously. Critical: under Florida's AOB reform (January 2023), you retain all policy benefits — Palm Build works for you as the policyholder, not through an assignment.

02

Adjuster Visit + Palm Build Xactimate Estimate

Days 2-3

Your carrier assigns a field adjuster. Under Florida Statute 627.70131, they must begin investigation within 14 days. Palm Build provides our complete documentation package — moisture mapping, thermal imaging, photography, and a full Xactimate-formatted scope of loss — to the adjuster during the inspection. We walk the property together, ensuring the adjuster sees every affected area in your Boynton Beach home, including moisture trapped behind CBS stucco walls and under slab-on-grade foundations where damage isn't visible.

03

Claim Decision

Week 1-2

The insurer must provide a coverage determination within 60 days under Florida law, though most straightforward claims receive initial decisions within 1-2 weeks. For Boynton Beach claims, we ensure the adjuster understands CBS construction specifics, barrel tile replacement costs, and Palm Beach County building code requirements. If the initial estimate matches our Xactimate scope, restoration proceeds immediately. If there's a shortfall, we move to supplemental documentation.

04

Supplemental Claims (If Needed)

Week 2-4

Approximately 65-75% of Boynton Beach restoration projects require at least one supplement for hidden damage discovered during work — moisture behind CBS walls, mold in sealed cavities, polybutylene pipe failures not visible until demolition. Palm Build documents supplemental damage within 48 hours of discovery with photos, moisture data, and updated Xactimate line items. Florida's 18-month supplemental claim deadline applies. Most Palm Build supplements resolve in one revision cycle because we submit in the adjuster's own format.

05

Restoration Work

Month 1-3

Once mitigation is complete and the scope is approved, reconstruction begins. We document progress at every milestone — demolition, rough-in, Palm Beach County inspections, specialty material installation, and finish work. For Boynton Beach projects requiring Florida Building Code hurricane hardening upgrades, we include engineering certifications and inspection records. This ongoing documentation supports any remaining supplements and provides your carrier with proof that the approved scope is being executed correctly.

06

Final Payment Settlement

Month 3-6

Final walkthrough confirms every scope item is complete. A completion certificate is provided to your carrier with final photos, inspection records, and a summary of all work. Your carrier releases final payment — for Florida policies, this includes the recoverable depreciation holdback released upon verified completion. NFIP flood claims require a separate 60-day proof of loss submission, which we prepare on your behalf. Your Boynton Beach home is fully restored, and your claim is properly closed.

Know Your Coverage

What's Covered by Peril Type in Boynton Beach

Florida homeowners policies have unique coverage gaps that Boynton Beach homeowners must

understand before filing — especially the percentage-based hurricane deductible, mold

sublimits, the flood exclusion for rising water, and the critical distinction between

wind damage and storm surge during hurricane events.

Wind Damage

HO-3 (Hurricane Deductible Applies)

Roof, barrel tile, stucco, window damage from wind

Rain entering through wind-created openings

Fallen tree removal and structural damage

Hurricane deductible: 2-5% of dwelling value (not a flat amount)

Storm surge classified as flood — requires separate flood policy

Burst Pipe / Sudden Water

HO-3 (Covered)

Burst supply line, hot water heater failure, appliance leak

Emergency extraction and structural drying

Resulting damage to walls, floors, and contents

Gradual leaks, seepage, or long-term moisture intrusion

The pipe itself (the source) — only the resulting damage is covered

Flood (Rising Water)

NOT Covered by HO-3

Rising water from storms, canal overflow, or ground saturation

Storm surge during hurricane events — even if you have HO-3

Covered under NFIP or private flood policy (separate purchase required)

Boynton Beach CRS rating provides up to 25% NFIP premium discount

42.2% of Boynton Beach properties have substantial flood risk

Mold

Limited / Excluded

Standard HO-3 excludes mold or caps at $10K-$25K sublimit

Mold resulting from a covered sudden water event may bypass sublimit

Mold from humidity, condensation, or maintenance issues — excluded

Enhanced mold endorsement available from some carriers ($50K-$100K)

Sewer Backup

NOT Standard (Endorsement Needed)

Sewer and drain backup is NOT covered by standard HO-3 policies

Sewer backup endorsement available from most carriers ($5K-$25K limits)

Category 3 contaminated water — most expensive to remediate

Common in Boynton Beach during heavy rain events that overwhelm aging systems

Saltwater Surge

Flood Policy Only

Saltwater storm surge is classified as flood — excluded from HO-3

Covered only under NFIP or private flood insurance policy

Causes accelerated corrosion of electrical, plumbing, and HVAC systems

Remediation costs 2-3x freshwater due to contamination and corrosion

Documentation That Wins Claims

What Palm Build Documents on Every Boynton Beach Project

Insurance claims are won or lost on documentation. In Florida's contentious insurance

market where carriers scrutinize every line item, your adjuster makes coverage decisions

based on the evidence provided — and the format matters as much as the content. Here's

what Palm Build produces on every Boynton Beach restoration project and why it matters

for your claim.

Moisture Mapping Every Wall & Floor

Pin-type and non-invasive moisture meters measure every affected surface — walls, floors, ceilings, and behind cabinetry. In Boynton Beach's CBS slab-on-grade construction, moisture wicks 12-24 inches up block walls before it's visible. Our moisture maps prove the full extent of damage your adjuster can't see with the naked eye, justifying the complete scope of demolition and drying.

Thermal Imaging Scans

Infrared thermal cameras reveal temperature differentials caused by moisture trapped behind CBS stucco walls, under tile floors, and in ceiling cavities. This non-invasive technology shows your adjuster exactly where water has migrated — critical in Boynton Beach homes where CBS construction traps moisture behind impermeable surfaces for weeks. Thermal images become exhibit-quality evidence in contested claims.

Photo & Video of All Damage

Comprehensive photography and video documentation of every affected area before any cleanup begins. We photograph damage from multiple angles with reference scales, timestamps, and location tags. For Boynton Beach hurricane claims, we separate wind damage photos from water intrusion photos to support cause-of-loss classification — the single most important distinction in a multi-peril event.

Xactimate-Formatted Scope of Loss

Line-item estimates written in the same software your insurance carrier uses. Every damaged item is measured, described, and priced per Xactimate's localized cost database for the Boynton Beach FL market — including Palm Beach County labor rates, CBS-specific demolition and rebuild costs, and barrel tile replacement pricing that generic estimates consistently under-scope.

Daily Drying Logs with Readings

Data-logged moisture readings taken every 24 hours during the drying process. In Boynton Beach's subtropical climate where ambient humidity regularly exceeds 70%, proving that professional drying equipment was necessary — not natural evaporation — requires scientific documentation. Daily logs show progressive moisture reduction against IICRC dry standards, justifying equipment placement and drying duration to your adjuster.

Materials Inventory (Removed & Why)

Detailed inventory of every material removed during demolition — drywall, insulation, flooring, cabinetry, baseboards — with photographic evidence of why each item required removal. This prevents the common adjuster challenge of 'Why did you remove that?' Contamination levels, moisture readings, and visual evidence for each removed material are documented and submitted with your claim.

Air Quality Testing Results

Pre- and post-remediation air quality testing when mold is present or suspected. In Boynton Beach's climate where mold colonizes in 24-48 hours after water intrusion, air quality data proves the necessity of containment protocols and antimicrobial treatment. Post-remediation clearance testing provides your carrier with third-party verification that the remediation was successful and the home is safe for occupancy.

Common Pitfalls

Why Boynton Beach Insurance Claims Get Denied

These are the five most common reasons Boynton Beach restoration claims are partially or

fully denied — and exactly how Palm Build's documentation process prevents each one.

"Pre-Existing Damage"

The most common denial in Boynton Beach — the insurer blames the age of CBS concrete block construction, claiming the stucco cracking, moisture intrusion, or structural shifting was pre-existing rather than caused by the reported event. For homes built in the 1960s-1980s (Leisureville, Chapel Hill, Lake Boynton Estates), carriers routinely argue that CBS wall deterioration is age-related, not event-related. Without timestamped moisture data proving the damage timeline, this denial sticks.

How Palm Build Prevents This

Palm Build documents moisture levels, thermal anomalies, and damage patterns immediately upon arrival — establishing a clear baseline tied to the reported loss date. Timestamped data with IICRC-standard readings creates an evidence trail that contradicts the pre-existing damage argument.

"Maintenance Issue"

Carriers attribute humidity-related damage, mold growth, and slow water intrusion to the homeowner's failure to maintain the property — especially in Boynton Beach's subtropical climate where ambient humidity averages 60-80% year-round. HVAC condensation, bathroom exhaust failures, and gradual plumbing leaks are all classified as maintenance rather than covered losses. Mold resulting from humidity is excluded; mold resulting from a covered sudden event may be covered.

How Palm Build Prevents This

Palm Build classifies every item of mold and moisture damage by its specific cause. When mold results from a covered sudden water event (burst pipe, appliance failure), we document the causal chain connecting the mold to the original covered loss — potentially bypassing both the maintenance exclusion and the mold sublimit.

"Flood Exclusion"

Rising water from storm events, canal overflow (common near LWDD canals), and ground saturation is classified as flood — excluded from standard HO-3 policies. Carriers exploit ambiguity during hurricane events by classifying wind-driven rain entering through a damaged building envelope as 'rising water' or 'storm surge,' shifting liability to a flood policy you may not have. With 42.2% of Boynton Beach properties at substantial flood risk, this exclusion affects nearly half the homes in the city.

How Palm Build Prevents This

Palm Build documents water entry points and flow patterns to distinguish between rising water (flood policy) and sudden/accidental discharge or wind-driven rain (homeowners policy). Photographic evidence of entry points, flow direction, and water line heights establishes cause-of-loss classification that withstands carrier challenge.

"Late Filing"

Florida's 1-year filing deadline (reduced from 2 years by SB 2A in 2023) means any damage reported more than 12 months after the loss date is automatically denied — regardless of how legitimate the claim. For Boynton Beach homes with slow water intrusion through CBS stucco walls where damage develops gradually behind impermeable finishes, the loss date can be ambiguous. The 18-month supplemental deadline adds additional urgency for hidden damage discovered during restoration.

How Palm Build Prevents This

Report any suspected damage immediately — even if minor. Palm Build helps establish the loss date with timestamped documentation tied to a specific identifiable event. We track all supplemental deadlines and submit within 48 hours of discovering hidden damage, well within the 18-month window.

"Insufficient Documentation"

Claims denied for lack of evidence — no moisture readings, no thermal imaging, no photos before cleanup began, no daily drying logs, no Xactimate-formatted scope. The restoration company did the work but didn't produce the documentation the adjuster needs to justify payment. This is the most preventable denial and the most common reason Boynton Beach homeowners receive partial payments instead of full coverage.

How Palm Build Prevents This

This is exactly why Palm Build exists. We document before we touch anything — moisture mapping, thermal imaging, comprehensive photography, Xactimate scope, daily drying logs, air quality testing, and materials inventory. Every document is formatted for the adjuster, not for the homeowner. The documentation is the claim.

We Work With Every Carrier

Top 10 Insurance Carriers in Palm Beach County

Palm Build works with every carrier writing homeowners policies in the Boynton Beach

market. Our Xactimate-based documentation integrates with any carrier's claims workflow.

Click any carrier for tips on working with their claims team.

RankCarrierFL Policies

The Palm Build Difference

Why Boynton Beach Homeowners Choose Palm Build for Insurance Claims

The difference between a $4,200 partial payment and an $18,000 full claim recovery isn't

your policy — it's your documentation. Here's why Boynton Beach homeowners trust Palm

Build to handle their insurance restoration claims.

Xactimate-Certified Estimators

Every estimate, supplement, and change order is written in the same software and pricing database your carrier uses. No format translation, no re-entry errors, no weeks of back-and-forth. In Florida's post-SB 2A environment where carriers scrutinize every line item, Xactimate-native estimating is the single most effective tool for accelerating claim approval. Our estimators use localized Boynton Beach FL pricing — including Palm Beach County labor rates and CBS-specific material costs.

30-45 Minute Response Time

From our Deerfield Beach operations center, we reach Boynton Beach homes in 30-45 minutes — Aberdeen, Hunters Run, Canyon Isles, Leisureville, Chapel Hill, and every neighborhood in between. Emergency mitigation begins immediately while documentation runs in parallel. The faster we arrive, the less damage develops, and the stronger your claim documentation becomes.

Document Before Touching Anything

Pre-mitigation documentation is the foundation of every successful claim. We photograph, moisture-map, and thermally image every affected area before any cleanup begins. This establishes the baseline condition your adjuster will reference for the entire claim. In Boynton Beach's CBS homes where water damage hides behind stucco and impermeable finishes, this initial documentation proves the full extent of damage before it's altered by remediation work.

Know Florida Insurance Law

We know the deadlines, the exclusions, and the post-2023 reform rules that affect every Boynton Beach claim. 1-year filing deadline. 18-month supplement window. AOB prohibition. Hurricane deductible calculations. Mold sublimits. Flood exclusions. Citizens depopulation rules. Our documentation is designed around these legal requirements — not around generic restoration industry standards.

Work With All Carriers

Citizens, State Farm, Universal, Slide, Tower Hill, Frontline, American Integrity, Progressive, USAA, Florida Peninsula — we've processed claims with every major carrier in the Palm Beach County market. We know each carrier's claims workflow, adjuster preferences, and documentation requirements. This carrier-specific knowledge means faster approvals and fewer revision cycles.

Help With Supplemental Claims

65-75% of Boynton Beach restoration projects require at least one supplement for hidden damage discovered during work. We document supplemental damage within 48 hours of discovery — with photos, moisture data, and updated Xactimate line items — and submit directly to your adjuster. Most Palm Build supplements resolve in one revision cycle because we submit in the format the adjuster already uses.

Common Questions

Boynton Beach Insurance Restoration FAQ

What are the Florida-specific deadlines for filing an insurance claim in Boynton Beach?

Under Florida Statute 627.70132 (as amended by SB 2A in 2023), you must report property damage to your insurer within 1 year of the date of loss. Supplemental claims — for additional damage discovered during restoration — must be filed within 18 months. Your insurer must begin investigation within 14 days of receiving your claim and provide a coverage determination within 60 days. For NFIP flood claims, a sworn proof of loss must be submitted within 60 days. These deadlines are strictly enforced — missing them can result in claim denial regardless of the damage's legitimacy. Palm Build tracks every deadline on your behalf from the moment we begin work.

What does Florida's AOB prohibition mean for Boynton Beach homeowners?

Senate Bill 2A (effective January 1, 2023) eliminated Assignment of Benefits (AOB) for new property insurance claims in Florida. Previously, homeowners could assign their insurance benefits directly to a restoration contractor, who would then bill and negotiate with the carrier. Under the new law, you retain control of your claim — you remain the policyholder, you authorize the work, and your carrier pays you. This means you should never sign documents that attempt to assign your insurance benefits to any contractor. Palm Build operates fully within this post-reform framework: we document, restore, and coordinate with your adjuster, but you direct the claim and receive the insurance proceeds.

What is the difference between Citizens Property Insurance and private carriers in Boynton Beach?

Citizens Property Insurance Corporation is Florida's state-backed insurer of last resort, created for homeowners who cannot find coverage in the private market. With 687,502 policies statewide, Citizens has become one of the largest property insurers in Florida — not by design, but because six major private carriers exited the state between 2020 and 2023. Citizens has tightened underwriting requirements across Palm Beach County, including mandatory inspections, roof age restrictions (typically 15 years or newer), and depopulation efforts that move policyholders to private carriers. Private carriers active in the Boynton Beach market include State Farm (400,384 FL policies), Universal (251,927), Slide (236,627), Tower Hill (233,392), Frontline (188,785), American Integrity (167,738), Progressive/ASI (157,591), USAA (154,020), and Florida Peninsula (114,437). Palm Build works with every carrier — Citizens and private alike — and formats documentation to each carrier's claims workflow.

How is my hurricane deductible calculated in Boynton Beach?

Florida homeowners policies have a separate hurricane/wind deductible calculated as a percentage of your dwelling coverage — typically 2% to 5%. For a Boynton Beach home at the median value of $317,000, a 2% hurricane deductible is $6,350 and a 5% deductible is $15,875 — significantly higher than a standard $1,000 or $2,500 flat deductible for non-hurricane perils. This percentage-based deductible applies only to wind and hurricane claims; other covered perils (burst pipes, fire, appliance failures) use your standard flat deductible. Choosing a higher hurricane deductible lowers your annual premium but increases your out-of-pocket exposure during hurricane season. Palm Build helps you understand your specific deductible structure before restoration begins so there are no surprises.

Does my Boynton Beach homeowners policy cover mold damage?

Most Florida HO-3 policies either exclude mold entirely or sublimit coverage to $10,000-$25,000 — far below the cost of a significant mold remediation project. However, when mold results directly from a covered water event (burst pipe, appliance failure, wind-driven rain intrusion), the mold remediation may be covered under the original water damage claim rather than the mold sublimit. The key is documentation: Palm Build connects mold colonization directly to the covered water event through timestamped moisture readings, thermal imaging showing moisture migration paths, and microbial assessment reports. This cause-and-effect documentation is critical for bypassing mold sublimits and getting full remediation coverage. A separate mold endorsement can be added to most policies for broader coverage — ask your agent about availability and cost.

What is the difference between flood damage and water damage coverage in Boynton Beach?

This distinction determines whether your claim is approved or denied — and it catches Boynton Beach homeowners off guard every hurricane season. Standard HO-3 homeowners insurance covers sudden and accidental water damage from internal sources: burst pipes, appliance failures, roof leaks from wind damage. It does not cover flood damage — defined as rising water from external sources including LWDD canal overflow, storm surge, and surface water accumulation during heavy rainfall. Flood damage requires a separate NFIP or private flood policy. With 42.2% of Boynton Beach properties at measurable flood risk and 50 LWDD canals threading through the city, separate flood coverage is essential — not optional. Boynton Beach NFIP policyholders benefit from a 25% Community Rating System (CRS) discount, one of the best rates in Palm Beach County. During hurricane events, both wind damage (homeowners policy) and flood damage (flood policy) can occur simultaneously, requiring separate claims to separate carriers — Palm Build documents and separates both damage types from the first inspection.

How does Palm Build document damage for insurance claims in Boynton Beach?

Every Boynton Beach restoration project includes comprehensive insurance documentation from the moment we arrive. Our standard documentation package includes: initial damage photos and video captured before any cleanup begins, FLIR thermal imaging identifying moisture behind walls and under slab edges, Tramex and Delmhorst moisture mapping with psychrometric data at every reading point, daily drying logs showing moisture reduction progress, a detailed Xactimate scope of work using the same software and pricing database your adjuster uses, cause-of-loss determination connecting damage to a specific covered event, photos at each stage of mitigation and reconstruction, and final completion documentation with clearance readings. This documentation is formatted for your specific carrier's claims workflow — whether that's Citizens, State Farm, Universal, or any other insurer active in Palm Beach County. Xactimate-native estimates eliminate the manual re-entry and cross-referencing that causes weeks of adjuster delay.

What should I do if my Boynton Beach insurance claim is denied?

Claim denials in Florida fall into several categories, each with different remedies. Coverage denials (the peril is excluded from your policy) are the hardest to overturn — common examples include flood damage on a policy without flood coverage, or gradual damage excluded under all HO-3 policies. Scope denials (the carrier agrees damage is covered but disputes the extent or cost) are the most common and most reversible — Palm Build files supplements with additional documentation, line-item justification, and supporting evidence. Deadline denials (you missed Florida's 1-year filing window or 18-month supplemental window) are nearly impossible to overturn. If your claim is denied, do not accept the denial without understanding the specific reason. Palm Build reviews denial letters, identifies whether the denial is legitimate or based on incomplete information, and files supplements with cause-specific evidence when covered items are incorrectly denied. For complex disputes, we can refer you to licensed public adjusters or insurance attorneys who specialize in Florida property claims.

Trusted Vendors

Trusted local pros in Boynton Beach

Outside our restoration scope, these are the vetted, licensed contractors we trust

alongside our work. Personally evaluated, reference-checked, and recommended by Palm

Build.

Insurance Claim in Boynton Beach? Palm Build Navigates It With You.

Palm Build handles the entire insurance process — documentation, adjuster coordination, supplement negotiation, Florida-specific deadline compliance — so you can focus on getting your home back. We work with every carrier in the Boynton Beach market including Citizens, State Farm, Universal, and all Palm Beach County insurers.