Insurance Restoration Process in Clover, South Carolina

In a town of 7,234 residents where the median home is valued at $295,700, a single underdocumented insurance claim can mean the difference between a full restoration and thousands in out-of-pocket costs. Clover homeowners face coverage gaps most never discover until they file a claim — flood exclusions near the Catawba River corridor, mold sublimits that cap payouts far below actual remediation costs, and sewer backup exclusions that require a separate endorsement. Palm Build navigates the entire insurance process from emergency documentation through final scope approval, so Clover families recover every dollar they have been paying for.

Approx. 30 miles — Charlotte, NC 35-45 min Response IICRC Certified

Why Proper Documentation From Day One Determines Claim Success in Clover

Clover sits at the intersection of small-town living and big-city insurance complexity.

Most homeowners carry policies through Charlotte-area agents but are governed by South

Carolina insurance law. Navigating that gap — and documenting damage correctly from the

start — is where Palm Build delivers the most value.

Day-One Documentation Determines Everything

48 hrs

Critical documentation window

In Clover, most restoration claims are won or lost in the first 48 hours. The documentation you create before the adjuster arrives becomes the foundation of your entire claim. Photos taken on a phone camera don't meet the standard — insurers need timestamped DSLR images, moisture meter readings, and professional damage assessments. Palm Build arrives first and documents everything so your claim starts from a position of strength.

South Carolina Insurance Landscape

SC-specific

Policy endorsements apply

South Carolina's insurance market is tightening. After Hurricane Ian and successive storm seasons, carriers are reducing coverage limits, raising deductibles, and scrutinizing claims more aggressively. Clover homeowners — many insured through Charlotte-area agents — face policies with SC-specific endorsements that differ from North Carolina language. Understanding these state-line differences is essential for full claim approval.

Below-Average Premiums, Hidden Exclusions

$1,100-$1,300

Average annual premium

Clover homeowners pay approximately $1,100-$1,300 annually for standard HO-3 coverage — below the South Carolina state average. Lower premiums attract homeowners but often come with reduced mold sublimits ($5,000-$10,000), separate wind/hail deductibles (1-2% of dwelling value), and no flood coverage. When damage strikes, these gaps surface as thousands of dollars in out-of-pocket costs.

Delayed Claims Cost More

24-72 hrs

Mold growth timeline

Every day between damage and documentation weakens your claim. In Clover's humid climate, water damage leads to mold within 24-72 hours. If you wait to call your insurer until mold has spread, the carrier may classify it as secondary damage with sublimited coverage — or deny it as a maintenance issue. Palm Build's same-day response creates the documented timeline that connects all damage to the original covered event.

Palm Build documents every detail of property damage in Clover before the insurance

adjuster arrives — creating the evidence foundation that drives full claim approval.

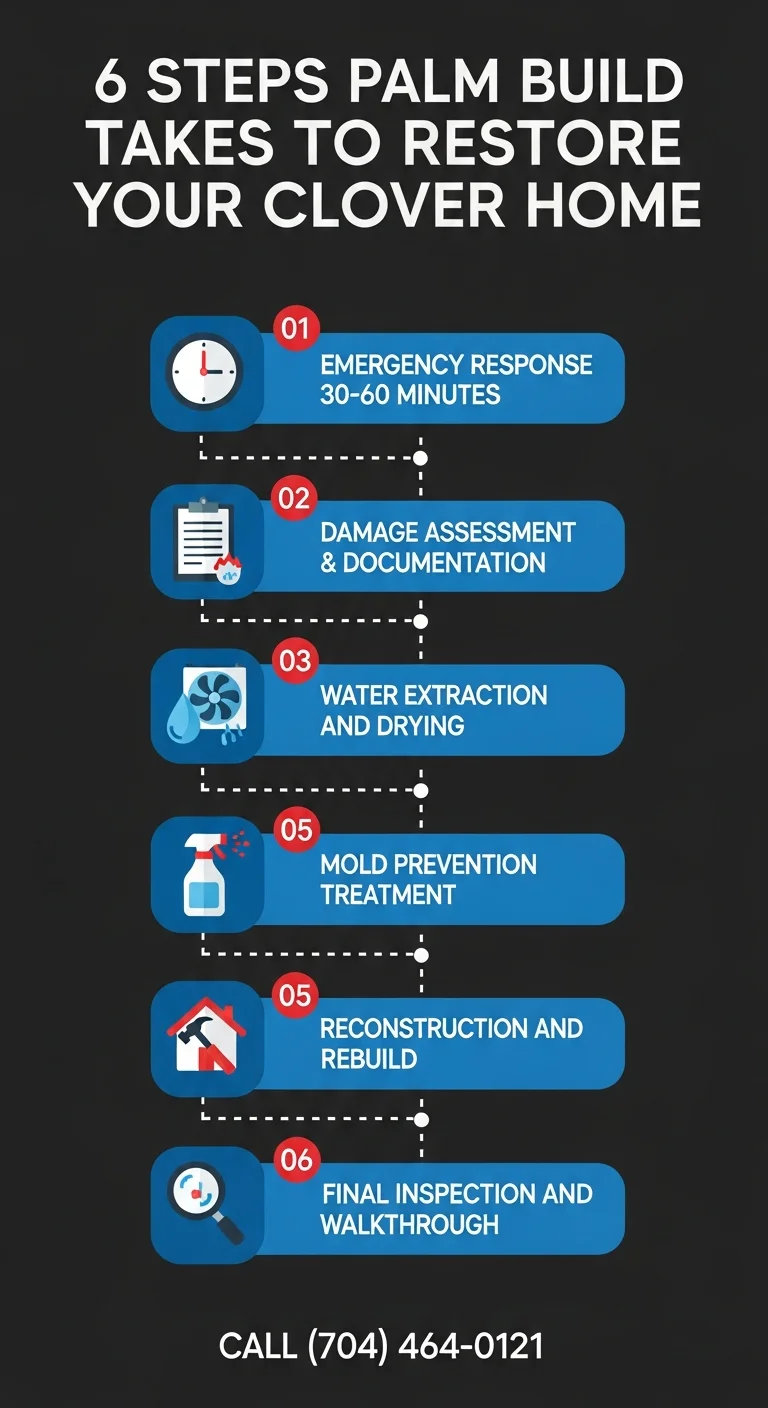

Claims Process

Step-by-Step Insurance Claims Support for Clover SC

Filing a restoration claim correctly from day one is the difference between full

coverage and a partial settlement that leaves you paying out of pocket. Here is exactly

how Palm Build supports your claim from first call through final payout.

01

Document the Damage

Before anything is moved, cleaned, or dried, Palm Build arrives to document every point of damage. We use DSLR photography with measurement references, thermal imaging to reveal hidden moisture, and pin-type moisture meters to map water migration. In Clover's older homes — especially those with crawl spaces — water travels far beyond what's visible. This initial documentation becomes the bedrock of your entire claim.

02

Contact Your Insurance Company

With professional documentation in hand, we help you file your claim. Our damage report, photo package, and preliminary scope-of-work estimate give your carrier everything they need to open the claim efficiently. For Clover homeowners with State Farm or Auto-Owners — the most common carriers — our reports are formatted specifically for their adjuster workflow.

03

Meet the Adjuster On-Site

We meet your insurance adjuster at your Clover property and walk them through every documented damage point. Our project managers speak the adjuster's language — Xactimate pricing, IICRC protocol references, and industry-standard scope terminology. Nothing gets missed because everything was captured before the adjuster arrived.

04

Review the Scope of Work

After the adjuster's inspection, we compare their approved scope against our documented damage assessment. If anything is missing — and in compound damage claims, items are almost always missed on the first pass — we prepare a detailed supplement with supporting evidence. Hidden damage behind walls, under floors, and in crawl spaces requires supplemental filing.

05

Approve and Begin Restoration

Once the scope is agreed upon, restoration begins immediately. Throughout the project, we maintain daily drying logs, progress photography, and updated moisture readings. Every piece of documentation feeds back into your claim file — supporting supplement filings for hidden damage discovered during the restoration process.

06

Final Walkthrough and Settlement

After restoration is complete, we conduct a final walkthrough with you. Your project file includes all documentation, photos, invoices, and inspection certificates. For RCV policies, we help you file for the recoverable depreciation holdback — money many Clover homeowners don't realize they're owed once work is finished.

Documentation Standards

What Palm Build Documents and Why It Matters in Clover

The quality of your damage documentation directly determines the size of your insurance

payout. Adjusters approve what they can see and verify. Our documentation package is

designed to capture every dollar your policy covers — using the tools and standards that

Clover-area carriers expect.

DSLR Photography

Professional-grade photos of every damage point with measurement references, timestamps, and GPS metadata. For storm claims in Clover, individual damage measurements documented against rulers. For water damage, progression photos showing before, during, and after treatment at every affected area.

Thermal Imaging

Infrared thermal cameras reveal moisture hidden behind walls, under floors, and above ceilings — damage invisible to the naked eye but captured in data the adjuster can verify. This is especially critical in Clover's older homes and crawl-space construction where water migrates unseen through subfloors and wall cavities.

Moisture Mapping

Pin-type and non-invasive moisture meters create a comprehensive moisture map of your Clover property. Each wall section, floor area, and crawl-space zone is measured, recorded, and tracked daily during drying. This data proves the full extent of water damage and verifies when drying targets are met.

Daily Drying Logs

Every day during structural drying, we record moisture readings, equipment placement, temperature, and relative humidity. These logs prove that professional-grade equipment was deployed for the necessary duration — preventing adjusters from challenging the scope or timeline of drying services.

Xactimate Estimates

We prepare scope-of-work estimates using Xactimate — the same software used by insurance adjusters for State Farm, Auto-Owners, Allstate, Cincinnati, and Travelers. Speaking the same language eliminates translation errors and reduces disputes over line items, pricing, and scope.

Causation Timelines

For compound damage claims — where storm damage led to water intrusion led to mold — we construct documented timelines showing how each damage phase connects to the original covered event. In Clover's humid climate, this causation chain is the key to getting compound damage approved as a single claim.

Thermal imaging reveals hidden moisture damage in a Clover home — every reading is

recorded, mapped, and included in your insurance claim file.

Coverage Gaps

The 5 Insurance Gaps Every Clover Homeowner Should Know

Clover homeowners enjoy lower premiums than coastal South Carolina — but those savings

come with gaps that surface at the worst possible time. Understanding these coverage

limitations before you file helps Palm Build build a claims strategy that maximizes your

payout.

Flood Exclusion

Full cost out of pocket for flood events

Standard homeowners insurance does NOT cover flood damage from rising water. Most of Clover sits outside FEMA mandatory flood zones, so separate flood insurance is rare. But properties near Crowders Creek, the Catawba River corridor, and low-lying areas along Kings Mountain Highway do flood. When it happens, homeowners without NFIP coverage face the full restoration cost out of pocket.

Typically Covered

Burst pipe water damage

Appliance line failures

Sudden roof leaks from storms

Typically Not Covered

Rising floodwater

Storm surge

Creek overflow

Surface water runoff

Mold Sublimits

$5K-$10K cap vs. $8K-$35K+ actual cost

Standard York County policies cap mold coverage at $5,000-$10,000. Clover crawl-space mold remediation routinely costs $8,000-$35,000+. The sublimit is exhausted before the project is half complete. Connecting mold directly to a covered water damage event — with documented causation timelines — is essential for maximizing coverage beyond the sublimit.

Typically Covered

Mold from sudden pipe burst (up to sublimit)

Mold testing after covered water loss

Typically Not Covered

Mold from long-term humidity

Pre-existing mold

Mold exceeding sublimit without supplement

Sewer Backup Coverage

Zero coverage without endorsement

Sewer and drain backup is NOT covered under standard SC homeowners policies — it requires a separate endorsement. In Clover, aging municipal sewer lines and tree root intrusion cause backups that send contaminated water into finished basements and ground-floor living spaces. The endorsement typically costs $40-$75/year but provides $5,000-$25,000 in coverage.

Typically Covered

Sewer backup (with endorsement only)

Drain overflow from sudden blockage (with endorsement)

Typically Not Covered

Sewer backup without endorsement

Septic system failures

Gradual drain deterioration

Ordinance or Law Coverage

Code upgrades not covered without endorsement

When restoring damage to older Clover homes, current building codes may require upgrades beyond simple replacement — updated electrical, plumbing brought to code, or structural reinforcements. Standard policies only pay to restore to pre-loss condition. Without Ordinance or Law coverage, you pay the code-upgrade difference out of pocket. This is especially relevant for homes in Clover's historic downtown area.

Typically Covered

Restoring damaged area to pre-loss condition

Like-kind materials replacement

Typically Not Covered

Electrical upgrades required by current code

Plumbing code compliance

Structural reinforcement mandated by inspector

Gradual Damage Exclusion

Complete denial if classified as gradual

Insurance covers sudden and accidental events — not gradual deterioration. Slow pipe leaks, long-term crawl-space moisture, and seepage through foundation walls are excluded. In Clover's humid climate with aging plumbing infrastructure, the line between "sudden" and "gradual" is where claims get denied. Our documentation establishes clear causation timelines that prove sudden origin.

Typically Covered

Sudden pipe burst

Appliance failure

Storm-caused roof leak

Typically Not Covered

Slow leak over weeks/months

Long-term condensation

Foundation seepage

Wear and tear

Clover Insurance Carrier Guide

Insurance Carriers Serving Clover SC Homeowners

Knowing which carrier insures your Clover home — and understanding their specific claims

process — can save weeks of delays and thousands in settlement gaps. No competitor

publishes this level of carrier-specific guidance for Clover and York County.

State Farm

Largest U.S. homeowners insurer — dominant presence in Clover and York County

Local agents: Multiple agents in Rock Hill and Fort Mill serving Clover residents; Charlotte-area agents also write Clover policies

Claims notes: State Farm uses field adjusters for most Clover claims. Their documentation workflow is standardized — our reports are formatted to match exactly. For water damage claims, State Farm requires detailed moisture readings and drying logs before approving structural drying scope. We provide these on day one.

Auto-Owners Insurance

Strong regional carrier across the Carolinas — well-represented in rural York County

Local agents: Independent agents in York County and the greater Charlotte metro area

Claims notes: Auto-Owners is known for competitive premiums in smaller SC communities like Clover. Their claims process relies heavily on independent adjusters. Detailed, organized documentation speeds their review. We format all reports with the line-item detail their adjusters expect.

Allstate

Significant market share in York County residential coverage

Local agents: Local agents in Rock Hill, Fort Mill, and the Lake Wylie corridor serving Clover homeowners

Claims notes: Allstate uses a mix of staff and independent adjusters. For compound damage claims — storm damage leading to water intrusion leading to mold — detailed timeline documentation is critical. We build causation timelines that connect every phase to the original covered event.

Cincinnati Insurance

Preferred carrier for higher-value homes in the Lake Wylie and Clover area

Local agents: Independent agents throughout York County and the Charlotte metro

Claims notes: Cincinnati Insurance is common among Clover homeowners with newer construction and higher dwelling values. Their policies tend to offer broader coverage terms but require thorough documentation for large claims. Our Xactimate-native estimates align with their scope review process.

Travelers

Major national carrier active in the SC market — common among Charlotte commuters in Clover

Local agents: Charlotte-based and Rock Hill agents writing SC policies for Clover residents

Claims notes: Many Clover homeowners who commute to Charlotte maintain Travelers policies through NC-based agents. These policies carry SC endorsements that may differ from NC standard language. We review policy language as part of our claims support to ensure SC-specific terms are addressed correctly.

Clover SC Average Annual Premiums by Coverage Level

Dwelling Coverage

Avg. Annual Premium

$100K - $199K

$895.00

$200K - $299K

$1,025.00

$300K - $399K

$1,215.00

$400K - $499K

$1,475.00

Source: SC Department of Insurance / PolicyGenius — York County, SC 2024 data

Documentation in Action

Insurance Documentation: From Damage to Settlement in Clover

On-site documentation: Capturing every damage point before the adjuster arrives

Thermal imaging: Revealing hidden moisture that supports the full claim scope

Water extraction: Every step documented with timestamps and moisture readings

Structural drying: Equipment placement and daily logs verify the scope of services

Why Palm Build

Why Clover Homeowners Choose Palm Build for Insurance Claims Navigation

The difference between a partial settlement and full coverage often comes down to

documentation quality and claims strategy. No competitor in Clover provides the

carrier-specific, neighborhood-level insurance guidance that defines our approach.

Xactimate-Native Documentation

We prepare every estimate in Xactimate — the same pricing software used by your insurance adjuster. When our estimate matches their format, there are fewer disputes, fewer delays, and faster approvals. For Clover claims with State Farm, Auto-Owners, or Travelers, this alignment is the difference between weeks and days.

We Work with Every Carrier Serving Clover

State Farm, Auto-Owners, Allstate, Cincinnati Insurance, Travelers — we know their claims processes, documentation requirements, and adjuster workflows. Whether your policy was written through a Rock Hill agent or a Charlotte office, we've navigated the process with every carrier active in Clover.

Supplement Filing Expertise

Hidden damage is rarely approved on the first adjuster visit. Our supplement process — filed with supporting moisture data, thermal images, lab results, and detailed scope documentation — captures the full extent of damage that initial estimates miss. In Clover's crawl-space homes, supplements often double the approved scope.

Clover-Specific Claims Knowledge

We understand compound damage from York County storms, wind/hail deductible traps, ACV vs. RCV on older roofs, flood exclusions near Crowders Creek, sewer backup endorsement gaps, and mold sublimits in crawl-space claims. No franchise offers this level of local claims intelligence for Clover homeowners.

Your Advocate, Not Your Insurer's

We work for you, not your insurance company. Our documentation is designed to maximize your legitimate claim — capturing every dollar your policy covers while maintaining the professional standards that adjusters respect. When there is a dispute, our evidence package speaks for itself.

Every step of the restoration process in Clover is documented, photographed, and

formatted for your insurance carrier — supporting full claim approval from start to

finish.

Common Questions

Clover Insurance Restoration FAQ

Does Palm Build work with my insurance company in Clover?

Yes — we work with every major carrier writing policies in the Clover and York County market, including State Farm, Auto-Owners, Allstate, Cincinnati Financial, and Travelers. Our estimates use the same Xactimate software and pricing database that your carrier's adjuster uses, which reduces format disputes and accelerates scope approval.

Should I call my insurance company or Palm Build first after damage in Clover?

Call Palm Build first — or at least simultaneously at (704) 464-0121. Your policy requires you to mitigate further damage immediately, and documenting the initial damage condition before cleanup begins is the most important evidence for your claim. We begin emergency mitigation and documentation while you open your claim. In Clover's humid climate, waiting 48 hours for an adjuster can allow mold colonization that triggers your sublimit or results in a secondary damage denial.

Is flood damage covered by my Clover homeowners insurance?

No. Standard homeowners policies exclude all flood damage — water entering your home from rising water, surface runoff, or overflowing creeks. Clover homes near the Catawba River corridor or Crowders Creek are at highest risk, but even homes in FEMA Zone X can experience excluded surface water intrusion. Separate NFIP or private flood coverage is required. Palm Build documents the precise source and path of water intrusion to support the correct coverage determination.

Does my Clover policy cover mold in my crawl space?

It depends on the cause. Most SC policies cap mold at $5,000-$10,000 sublimits and only cover mold resulting from a covered sudden water event. Crawl space mold from long-term humidity is excluded as gradual damage. South Carolina does not have statewide mold licensing standards, making contractor documentation quality critical. Palm Build's IICRC-certified processes connect mold to the covered loss when a sudden triggering event exists, establishing the timeline to prevent reclassification as gradual damage.

What is the difference between FEMA Zone AE and Zone X for my Clover property?

Zone AE is a Special Flood Hazard Area — 1% annual flood chance. Properties in Zone AE near the Catawba River or Crowders Creek face York County floodplain requirements including the substantial improvement rule: restoration costs exceeding 50% of market value trigger full flood compliance for the entire structure. Zone X is minimal risk — most Clover neighborhoods. Flood insurance is not required but recommended, as 20-25% of NFIP claims come from Zone X properties.

What about sewer and drain backup — is that covered?

Not under your standard policy. Sewer and drain backup is excluded unless you purchased a separate endorsement — typically $40-$100 per year with coverage caps of $5,000-$25,000. This is a significant gap for older Clover neighborhoods with aging infrastructure. The annual endorsement cost is minimal compared to the $8,000-$20,000 cost of a backup cleanup and restoration.

How much does Palm Build charge for insurance coordination?

Nothing additional. Insurance coordination, documentation, adjuster meetings, supplement filing, and scope negotiation are included as part of your restoration scope. Our fees are paid by your insurance carrier as part of the approved claim. You are responsible only for your policy deductible.

What if my insurance company denies or underpays part of my Clover claim?

Partial denials are common in Clover, particularly for mold exceeding sublimits, crawl space damage disputed as gradual, code upgrade costs without ordinance-or-law coverage, and hidden damage missed during the initial walkthrough. Palm Build files supplements with photographic evidence, moisture data, and Xactimate line items when legitimate items are denied. Complete evidence packages leave adjusters little room to dispute legitimate scope.

How long does the insurance claims process take for a Clover restoration?

Straightforward covered losses like a burst pipe typically take 1-3 weeks from filing to scope approval. Complex claims involving flood zone complications, sudden vs. gradual disputes, mold exceeding sublimits, or York County floodplain requirements can take 4-10 weeks. Palm Build's thorough initial documentation reduces the back-and-forth that extends most timelines.

What documentation does my insurance company need for a Clover claim?

Your carrier needs: pre-cleanup damage photos and video, cause-of-loss determination, thermal imaging scans, calibrated moisture readings, Xactimate scope with SC regional pricing, daily drying logs, stage-by-stage photos, FEMA flood zone verification if water intrusion is involved, and final completion documentation. Palm Build produces all of this as standard on every Clover project at no additional cost.

Need Help With a Restoration Insurance Claim in Clover?

Palm Build handles the entire insurance process — documentation, adjuster coordination, Xactimate estimates, supplement negotiation, flood zone verification — so you can focus on getting your home back. We work with every major carrier in the York County market and respond to Clover in 35-45 minutes.