Step 1

Read the denial letter carefully

It must state the specific policy provision and reason for denial. Compare this to your actual policy language.

Claim Denial Guide

A claim denial is not the final word. Understanding why claims get denied and knowing your escalation options — from supplements to public adjusters to appraisal — puts you back in the driver's seat.

Key Steps

Step 1

It must state the specific policy provision and reason for denial. Compare this to your actual policy language.

Step 2

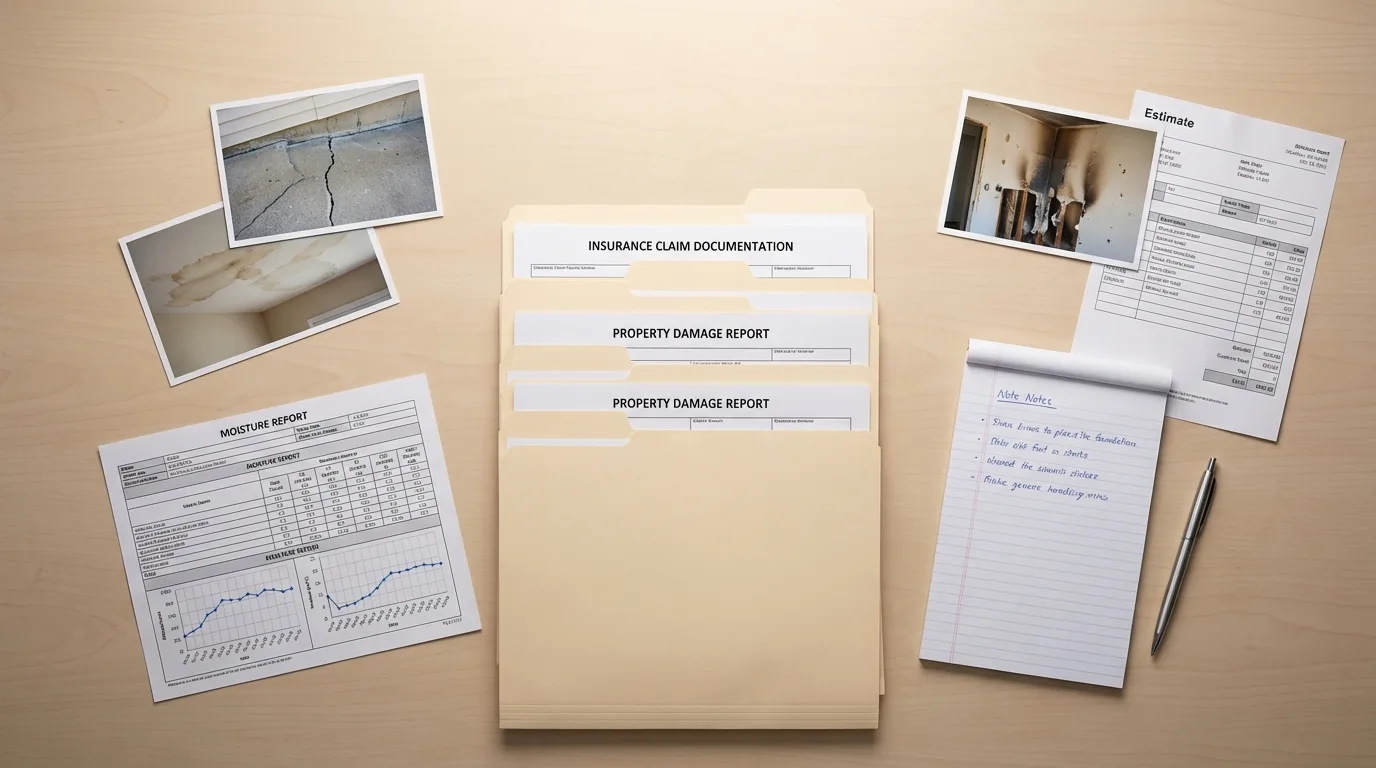

If denied for insufficient documentation, submit supplemental photos, moisture logs, plumber's reports, or contractor assessments.

Step 3

Send a formal written response citing policy language, attaching additional evidence, and requesting the claim be reopened.

Step 4

Supplement → Reconsideration → Public Adjuster → Appraisal Clause → State DOI Complaint → Attorney. Escalate in order.

Most denials can be challenged — many are overturned with additional documentation

The denial letter must cite the specific policy exclusion or reason

Public adjusters are most valuable for denied or significantly underpaid claims

Florida homeowners can request state-sponsored mediation for hurricane claims

A qualified restoration contractor's documentation often reverses denial decisions

In-Depth Guide

A claim denial feels final, but in most cases it is simply the beginning of a negotiation. Insurance companies deny claims for specific, documented reasons — and each reason has a corresponding counter-strategy. The most important first step is reading the denial letter carefully and identifying the exact policy provision cited. A denial for "insufficient documentation" requires a completely different response than a denial for "pre-existing damage" or "policy exclusion."

The escalation path for denied claims follows a predictable sequence: supplemental documentation, formal reconsideration request, public adjuster involvement, appraisal clause invocation, state Department of Insurance complaint, and finally legal action. Most denials are resolved at the first or second step with proper documentation. The key insight is that insurance companies respond to evidence — professional moisture readings, engineering reports, and detailed Xactimate estimates carry significantly more weight than homeowner photographs alone.

State regulatory agencies are a powerful and underused tool for denied claims. Florida's Department of Financial Services offers free mediation for hurricane claim disputes and investigates consumer complaints. North Carolina's Department of Insurance is known for being particularly responsive to consumer complaints and can apply pressure that accelerates resolution. Filing a state complaint does not prevent you from pursuing other remedies simultaneously — it adds another channel of pressure on the insurer to resolve the dispute fairly.

Visual Reference

Real-world examples of the documentation, coordination, and processes involved in insurance claims.

Read the denial reason carefully. Most denials can be challenged with the right evidence.

A qualified contractor's documentation often provides the evidence needed to overturn a denial.

A well-organized appeal package with clear evidence, policy citations, and expert reports is the most effective tool for overturning a denial.

The denial letter must cite a specific policy exclusion. Comparing that citation to your actual policy language often reveals the path to a successful appeal.

Step-by-Step

Understanding each step gives you leverage and helps prevent common problems.

Is it a coverage exclusion, insufficient evidence, late reporting, or cause-of-loss dispute? Each has a different response strategy.

Expert reports (plumber, engineer), additional photos, moisture data, contractor assessments — build the strongest case possible.

Written letter citing policy language, attaching evidence, and requesting reconsideration. Keep copies of everything.

Public adjuster for complex disputes. Appraisal clause for scope/cost disagreements. Attorney for clear bad faith. State DOI complaint as additional leverage.

South Florida

FL homeowners can request mediation through DFS for hurricane claim disputes. The AOB ban means you retain control of your claim — and the responsibility to pursue it.

Charlotte / NC

NC DOI is responsive to consumer complaints and can pressure insurers to review denied claims. The insurance market is less contentious than FL.

Coastal SC

SC DOI offers consumer complaint resolution. Wind/hail claims through the SC Wind and Hail Pool have their own appeal process.

Common Questions

The most frequent denial reasons are: insufficient documentation, pre-existing or gradual damage, maintenance-related issues, policy exclusions (like flood on a homeowners policy), late reporting, and cause-of-loss disputes. Each reason has a specific counter-strategy — the key is matching your response to the stated denial reason.

Appeal deadlines vary by state and policy. Florida requires insurers to respond to appeals within specific timeframes. Most policies have a window of 60-180 days for formal appeals, but some provisions like the appraisal clause have different deadlines. Check your policy and state regulations — acting quickly preserves your options.

Start with a public adjuster for claims denied due to scope or documentation issues — they charge 10-15% of the settlement and specialize in building the evidence package. An attorney is more appropriate for bad faith denials, coverage disputes, or when the insurer is unresponsive to legitimate appeals. The escalation path is: supplement → PA → appraisal → attorney.

Yes. A qualified restoration contractor provides professional documentation — moisture maps, Xactimate estimates, engineering assessments — that directly addresses the most common denial reasons. Their technical evidence often fills the gaps that caused the denial in the first place.

The appraisal clause is a policy provision that allows either party to request an independent appraisal when they disagree on the value of a loss. Each side hires an appraiser, and a neutral umpire resolves disputes. It is most effective for disagreements about repair scope or cost — not for coverage disputes, which require legal resolution.

Continue Reading

Our team has helped homeowners overturn denials with professional documentation, moisture mapping, and contractor assessments. We know what evidence adjusters need to reopen claims.